Financial Solutions Group

Commentary

Visions of Sugar Plums and Soft Landings

Rising real interest rates invariably trigger recessions. The residual impact of pandemic related

behaviors delayed the impact in this cycle.

Commentary

Bear Market – Interrupted

On Thursday, October 21 stock plunged following a sharp rise in consumer prices.

Commentary

US Growth Has Peaked Inflation Will Persist

by Team of Financial Solutions Group,

Long before supply chain issues and soaring consumer prices made the headlines, I warned readers that massive monetary expansion made persistent inflation inevitable.

Commentary

The 70% Solution

by Team of Financial Solutions Group,

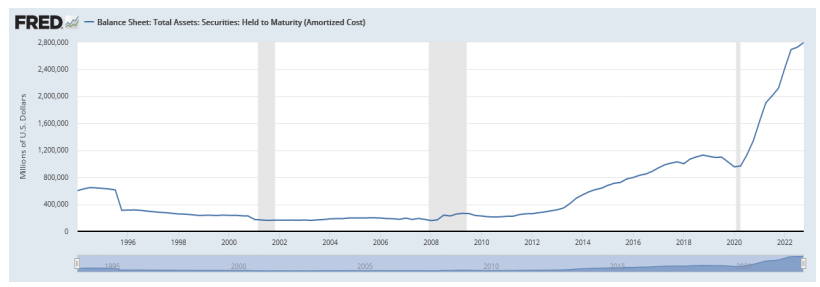

Inflation remained in check following the global financial crisis for over a decade despite a massive expansion of the Fed’s balance sheet.

Commentary

Where Have All The Workers Gone?

by Team of Financial Solutions Group,

In our last issue we suggested that the "Inflation Genie" was out of the bottle.

Commentary

January 2016 Flash Update

Stock market performance during the first week of the year has historically been a good indicator of market direction for the year ahead. Strong starts have historically indicated a better than normal outcome. Conversely, weak beginnings are generally ominous (excluding years when the Fed cuts short term rates).

Commentary

Corporate Earnings and Inflation

A few months ago our 2015 forecast emphasized several points we began making late last year. Taken together, those points differed dramatically from the prevailing wisdom of the time. As we begin May, they are falling into place.

Commentary

2015 Annual Forecast

It’s already February, but for many readers this is the first communication of 2015 so, Happy New Year! It’s been a great 6 weeks so far and we’re looking forward to many more to come. Let’s get into it…

Commentary

March Flash Update

At the end of February, the market as measured by the S&P 500 moved slightly above the year-end levels. Subsequently, a brief calming of the tensions surrounding the events in the Ukraine (time will tell) generated a relief rally that extended a bit further resulting in new record highs exactly 5 years after the financial crisis lows of March 2009.

Commentary

February Flash Update

It's too early to mean much, but so far out 2014 forecast is falling nicely into place. The market highs on Dec 31st have held, bonds are outperforming stocks, gold is outperforming both stocks and bonds, while gold mining shares are soaring! The anticipated volatility in emerging markets and Japan as well as the wild card of the Chinese economy continue to unfold, while bad weather has postponed the evidence of strong 2014 US growth.

Commentary

The Fed, Inflation, and the Perfect Storm in Gold Miners

Neither hopes of job creation nor fears of inflation (based on the massive expansion of the monetary base since late 2008) have thus far materialized. Total credit creation (i.e. money supply) during most of the last five years either shrank or barely grew despite massive growth in the monetary base. Nominal GDP (growth plus inflation) grows in response to total expansion of credit (both from the Fed and the banking system), not just the monetary base.

Commentary

Bursting of the Bond Bubble

Our April newsletter focused on the extreme overvaluation in the bond market. I argued that money market funds (or cash) were likely to outperform bonds and bond funds over the next decade. In May I applied the same logic to US stock prices and the inherent fallacy in the prevailing TINA (there is no alternative to stocks) hypothesis. Although stocks are likely to outperform bonds over the next decade, both asset classes remain seriously overvalued. In a world of overvalued assets, zero return looks much better than large potential losses even when that means foregoing transitory

Commentary

2013 US Financial Markets: Part 2 - The TINA Hypothesis

Contrary to the Bernanke Illusion (money market funds are a zero return investment), history indicates that money market funds are likely to provide investors with returns approximating inflation over the next decade. As I pointed out in our last letter, the markets are pricing in inflation levels significantly higher than the prospective total returns of 10 year TBonds. The small additional return achieved by corporate bonds or US stocks (at current prices) is unlikely to compensate a buy and hold investor with sufficient gains to justify the interim risks.