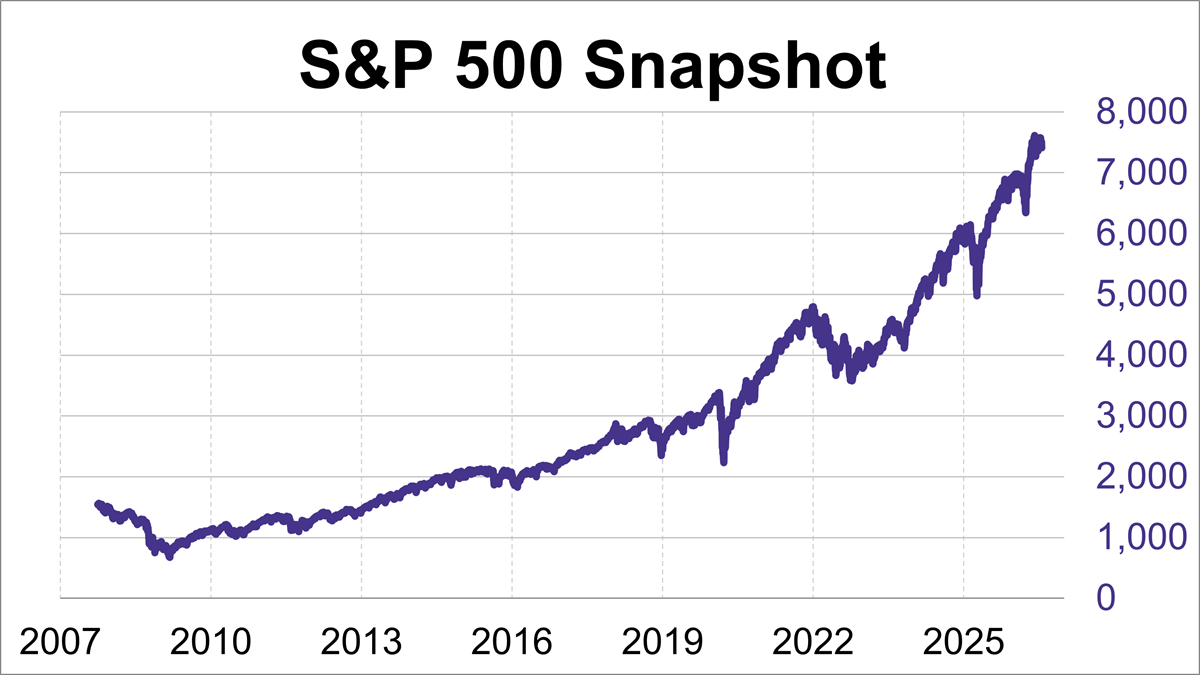

The S&P 500 ended its choppy week in the red, ultimately finishing with a loss of 0.6%.

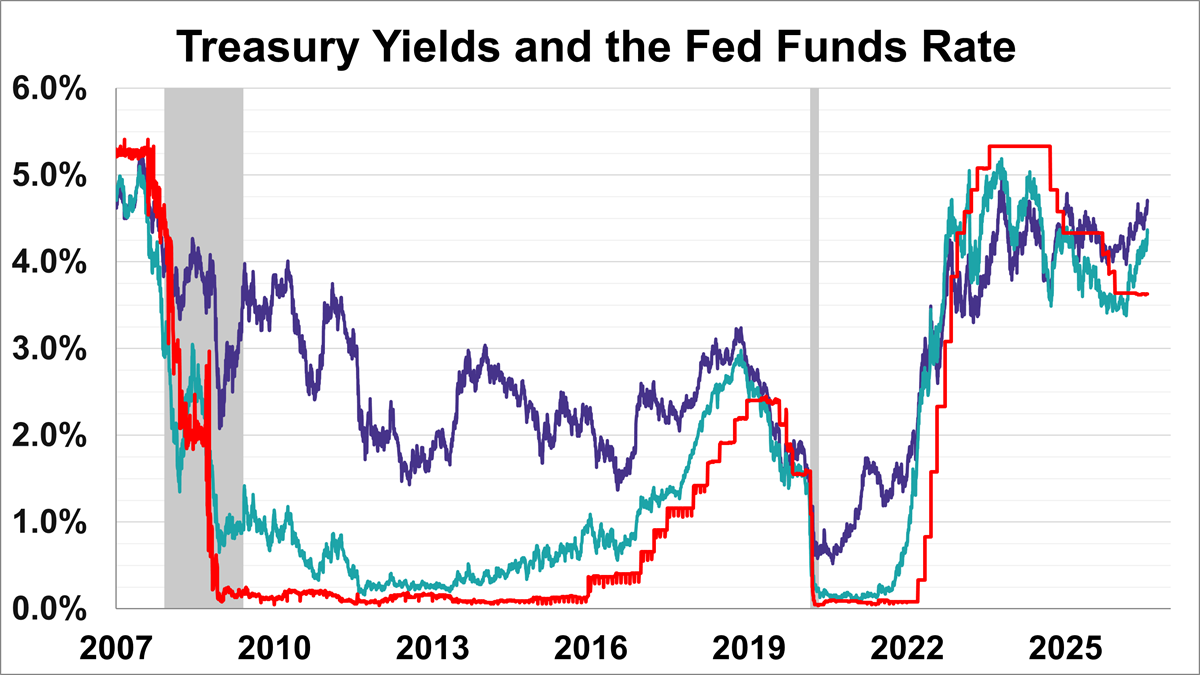

The yield on the 10-year note finished July 24, 2026 at 4.69% while the 2-year note ended at 4.33%.

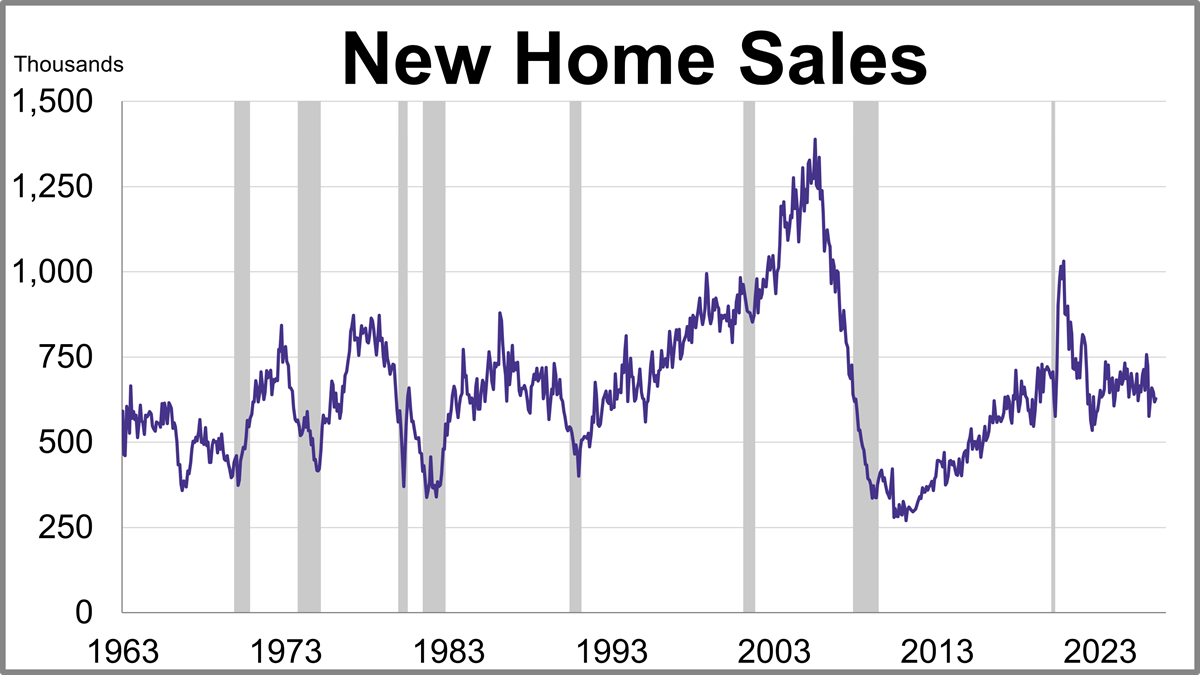

New home sales unexpectedly rose in June while the median price fell to its lowest level in almost a year.

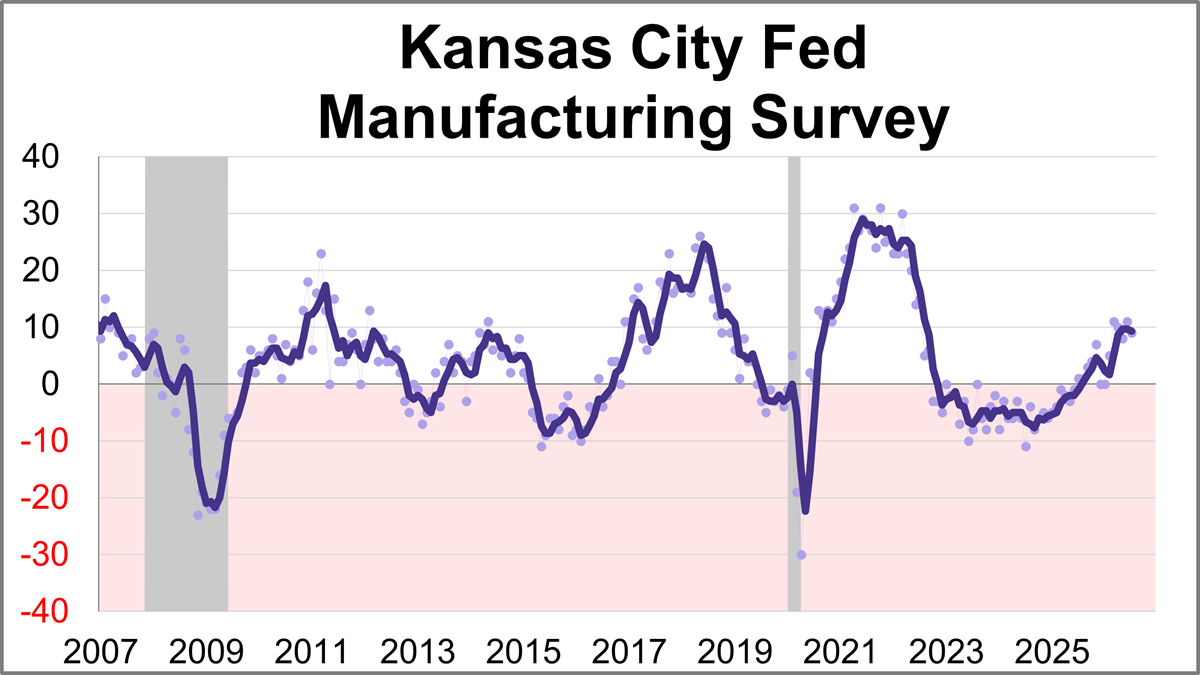

The Kansas City Fed Manufacturing Survey revealed regional activity remained steady in June. The composite index came in at 9 this month, down slightly from 11 in June but still indicating continued expansion.

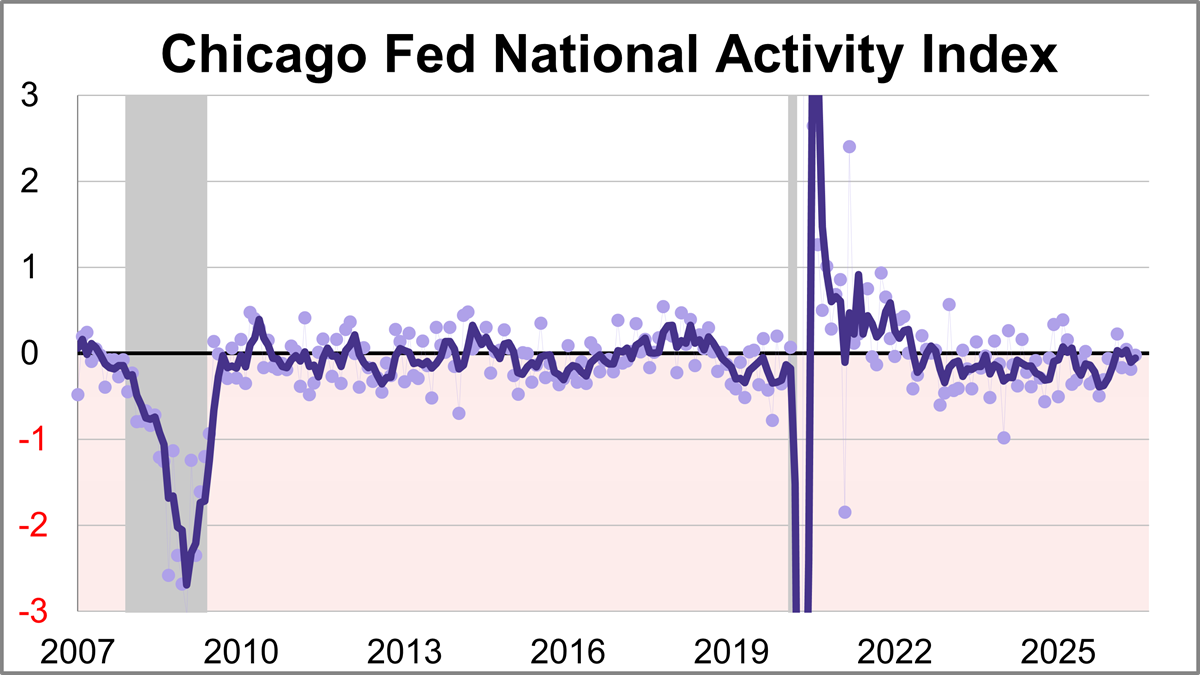

The Chicago Fed National Activity Index (CFNAI) rose to -0.02 in June from -0.19 in May. One of the four broad categories of indicators used to construct the index decreased from May, and two categories made negative contributions.

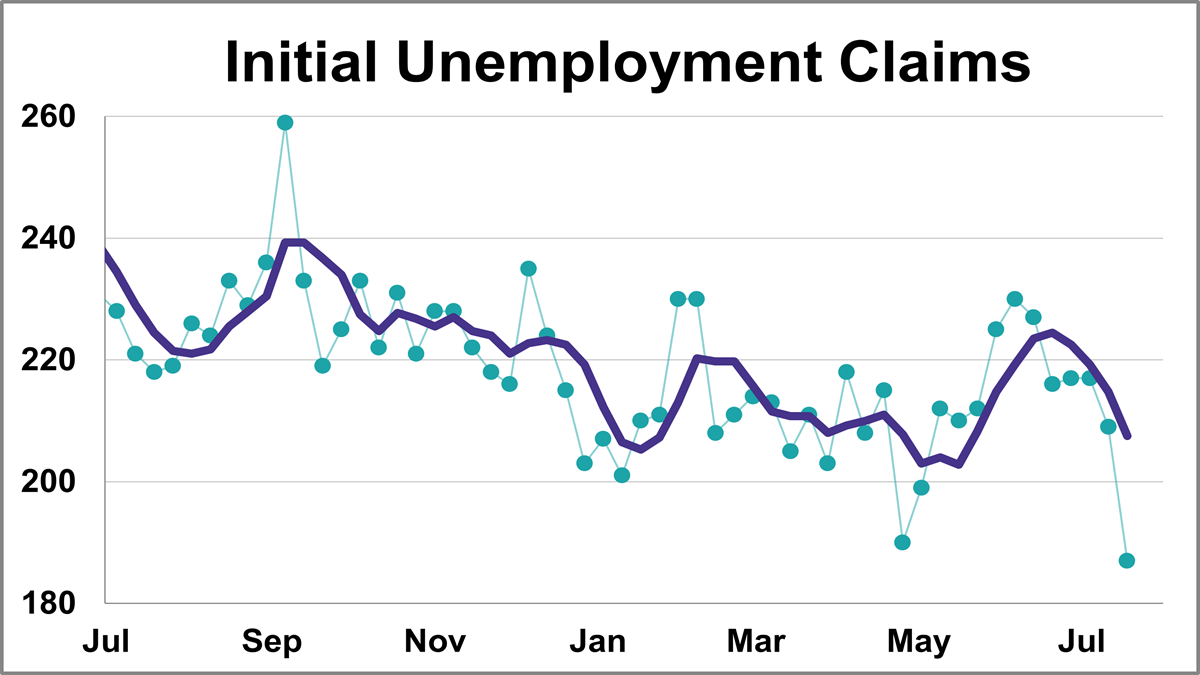

In the week ending July 18th, initial jobless claims were at a seasonally adjusted level of 187,000, the lowest level since 1969. This represents a decrease of 22,000 from the previous week's figure and was significantly lower than the forecast of 211,000.

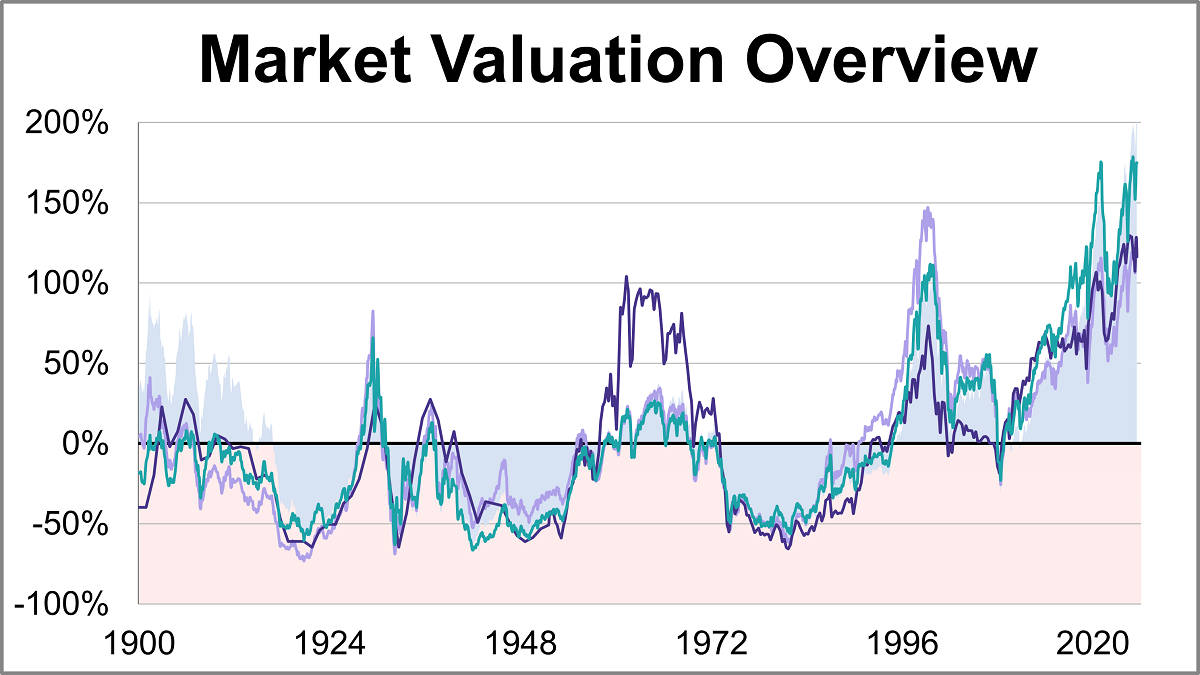

Here is a summary of the four market valuation indicators we update on a monthly basis.

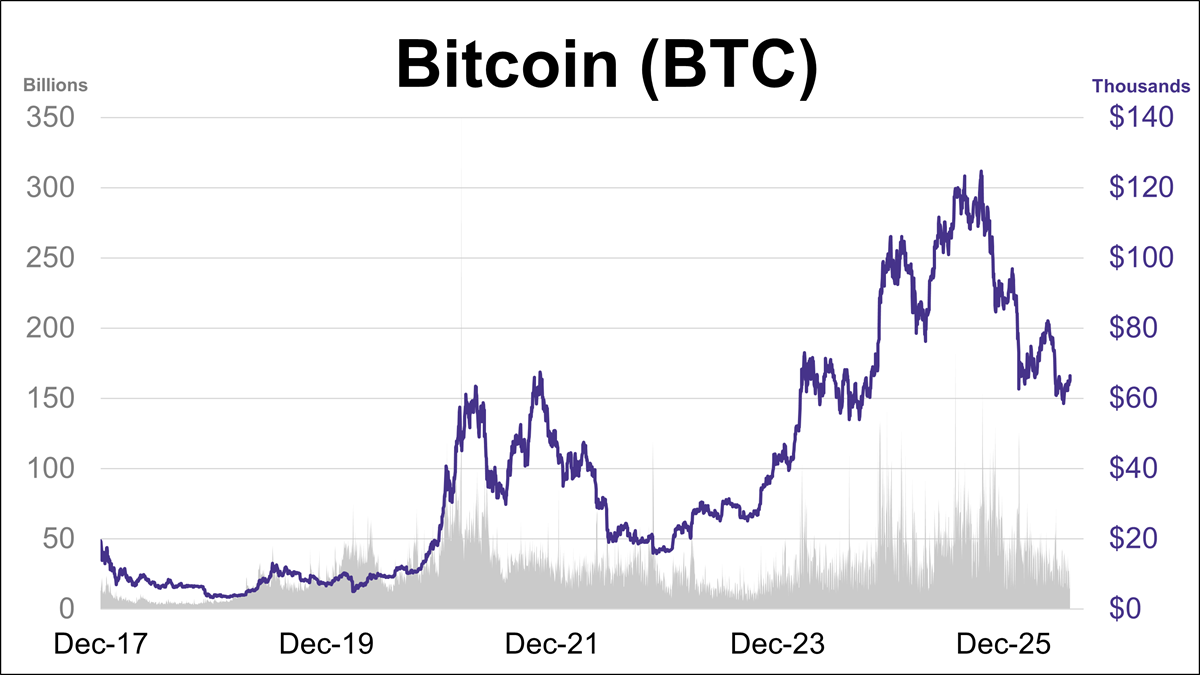

Bitcoin's closing price continued to edge higher this week, rising nearly 5% to its highest level in seven weeks. However, BTC is currently down approximately 24% year-to-date and sits about 47% below its October 2025 record high.

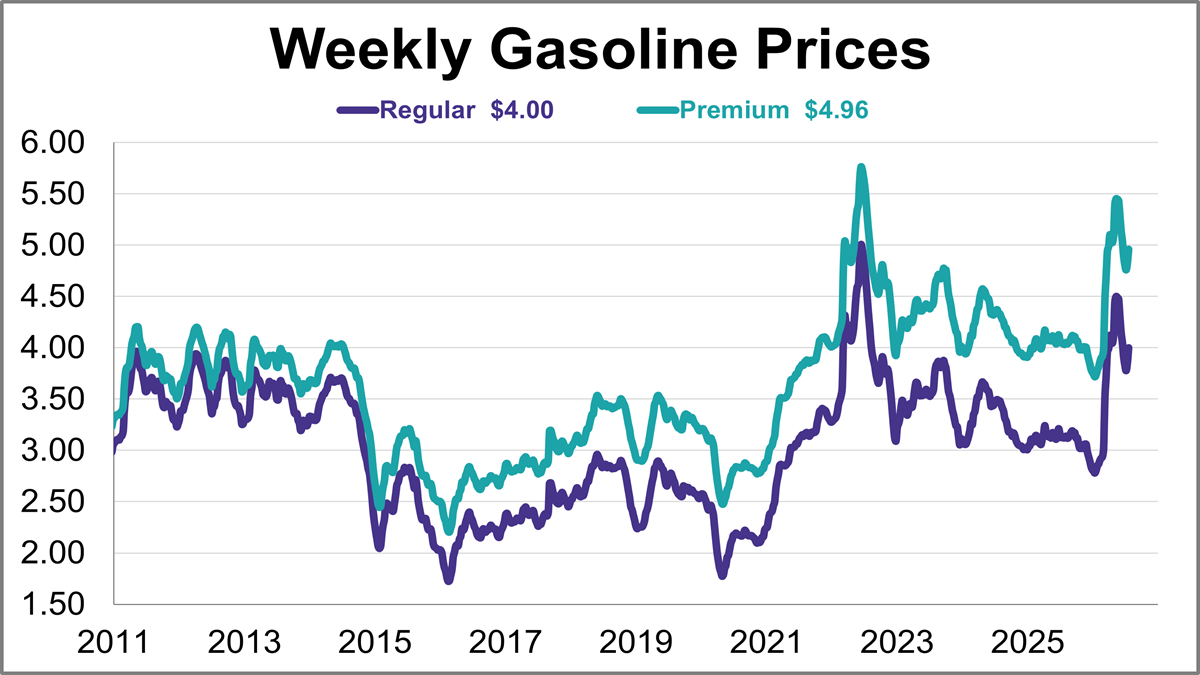

Gasoline prices rose for a second straight week, jumping back above $4.00 for the first time in over a month.

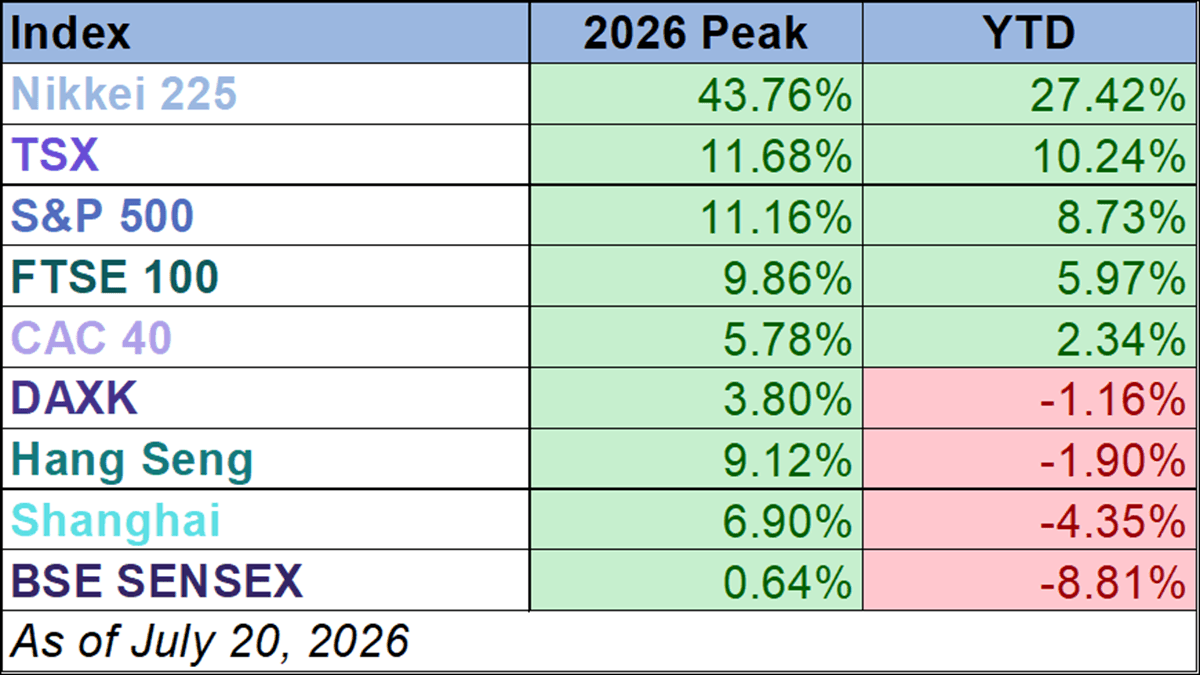

Five of the nine indexes on our world markets watch list posted year-to-date gains through July 20, 2026.

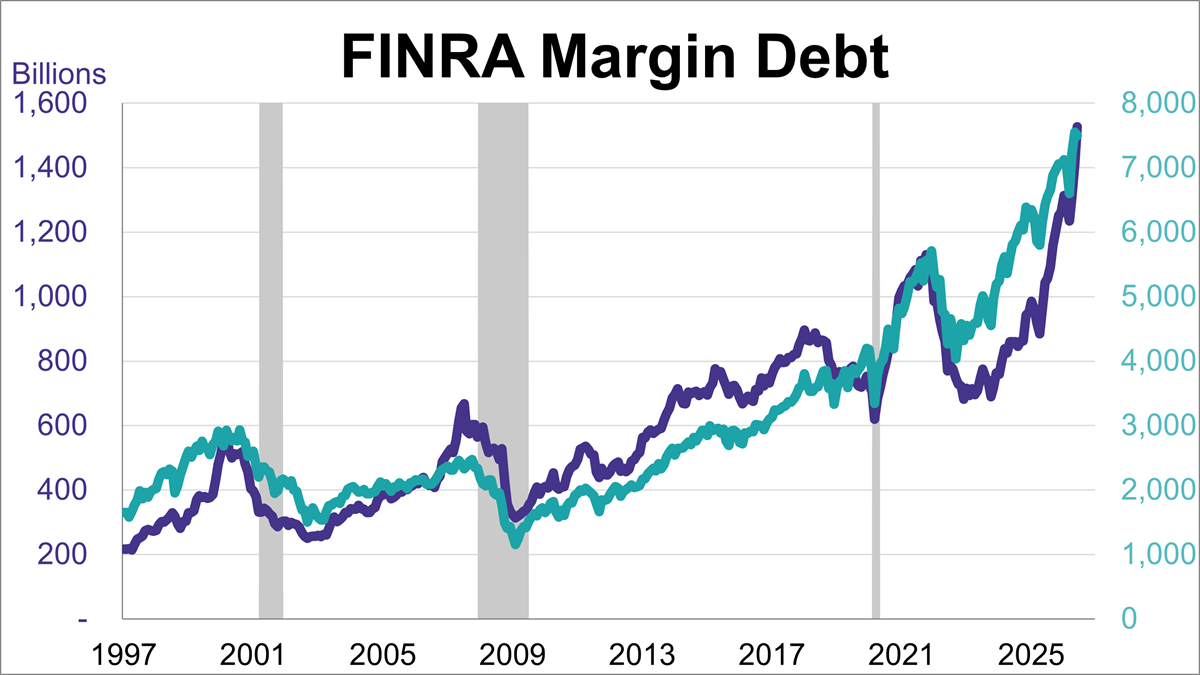

Margin debt rose for a third straight month in June, reaching a new record high of $1.53 trillion. This marked a 7.9% increase from May and a 51.5% rise compared to the previous year.

A handful of key economic data points dropped last week, painting a picture of an economy that is successfully downshifting from its recent inflation peaks even as consumers keep their footing.

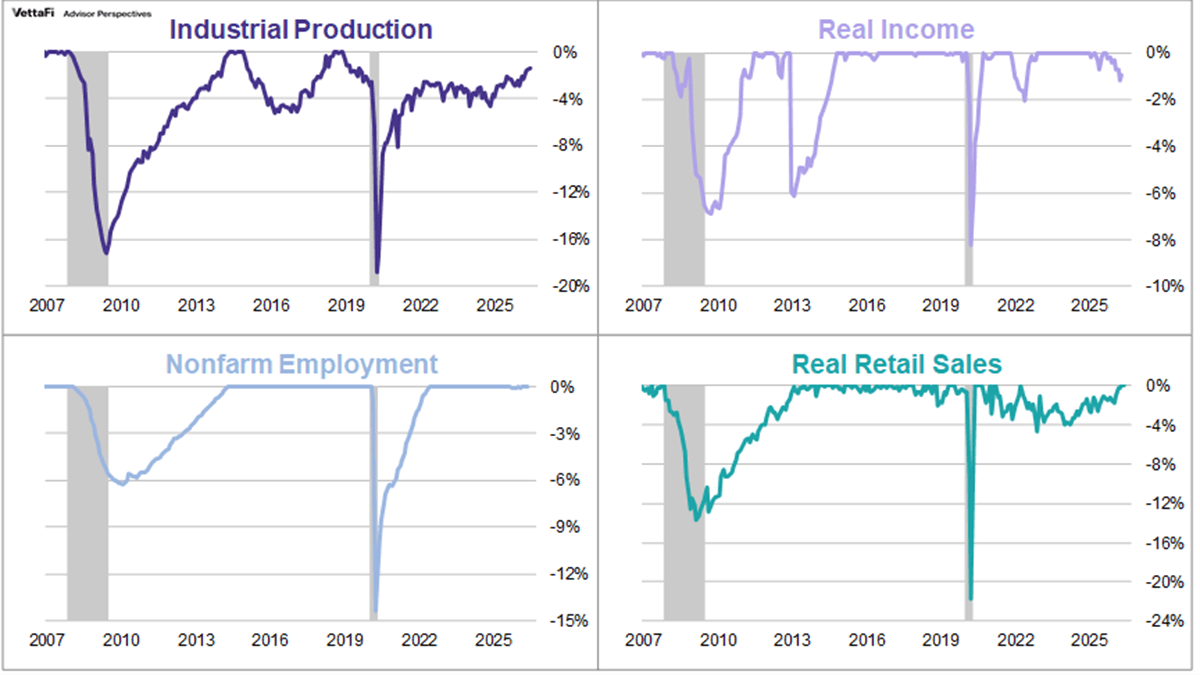

Official recession calls are the responsibility of the NBER Business Cycle Dating Committee, which is understandably vague about the specific indicators on which they base their decisions. There is, however, a general belief that there are four big indicators that the committee weighs heavily in their cycle identification process.

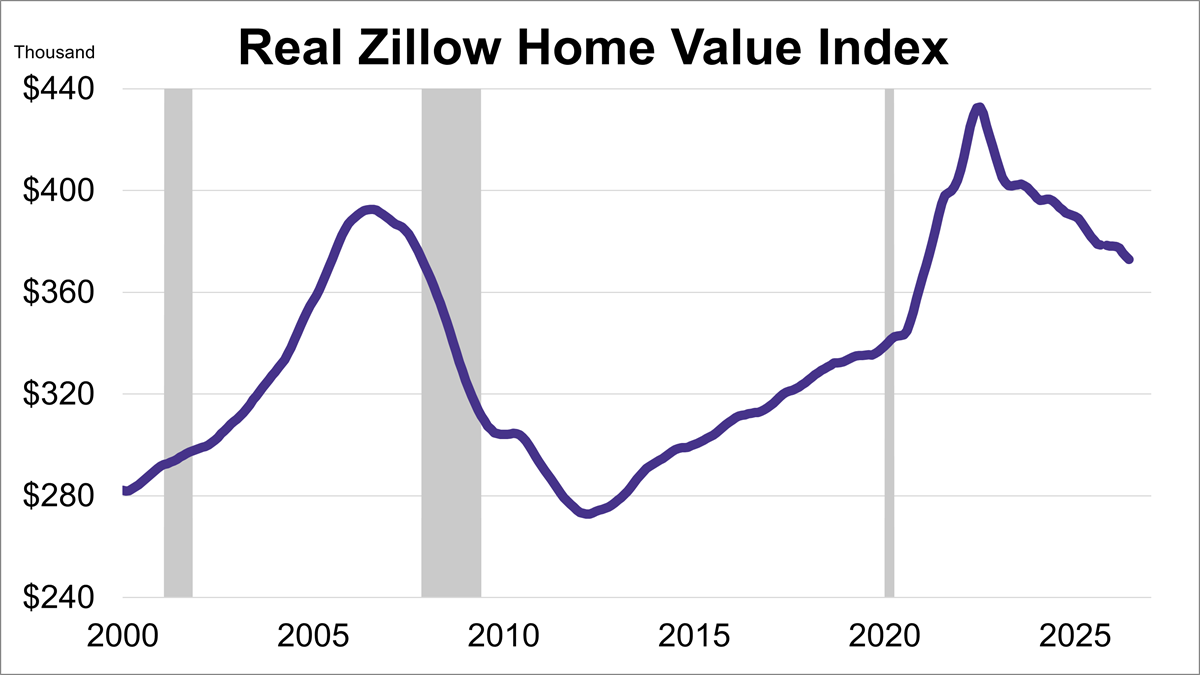

Home values fell for a second straight month in June, according to the Zillow Home Value Index. Additionally, after adjusting for inflation, real home values dropped even more sharply, hitting their lowest level in over five years.

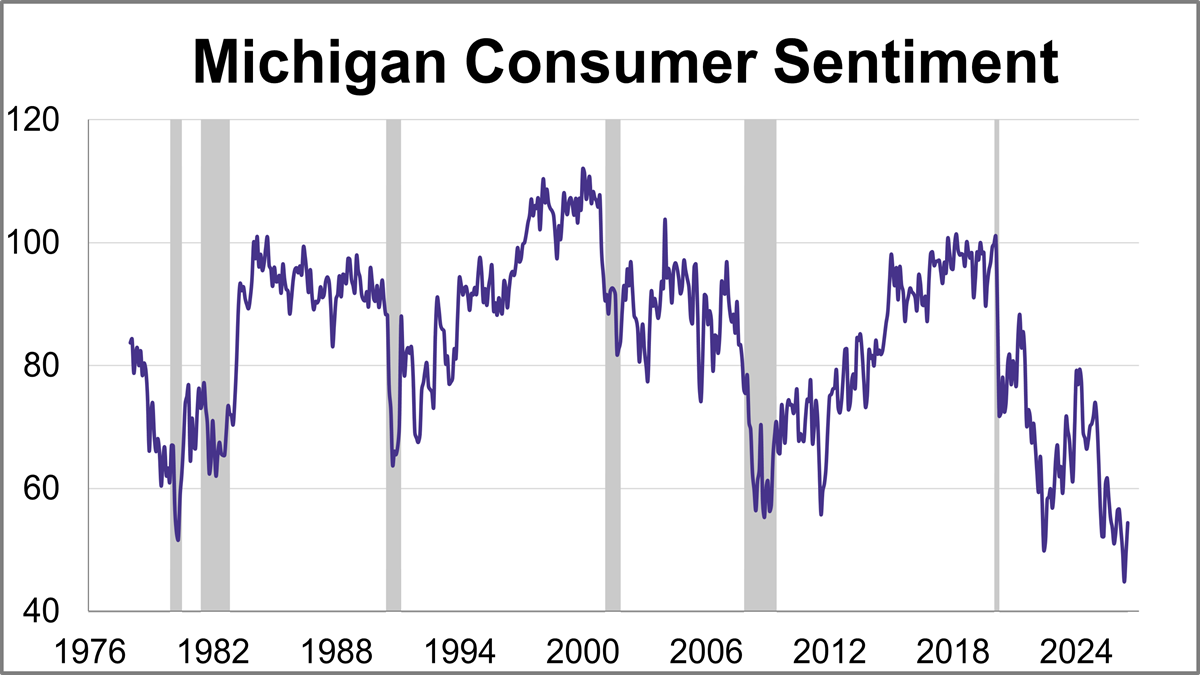

Consumer sentiment reached its highest level since February, driven by easing gas prices. The preliminary July reading for the University of Michigan Consumer Sentiment Index came in at 54.4. This marks a 9.9% (4.9 points) increase from June and beat the expected reading of 51.0.

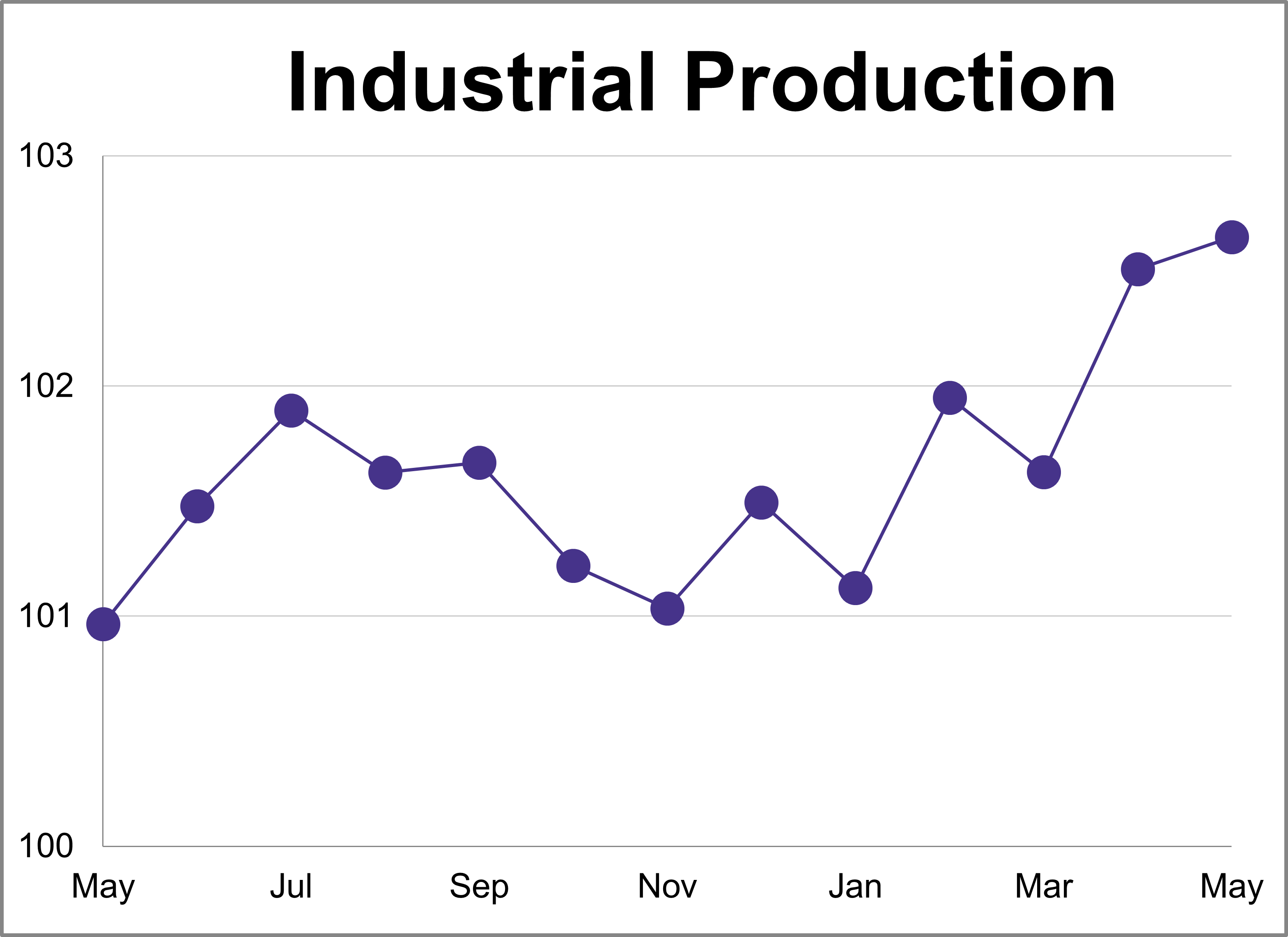

Industrial production rose less than expected in June, increasing 0.1% after May's 0.1% growth. This was lower than the expected 0.2% growth and marks a 1.1% increase compared to one year ago.

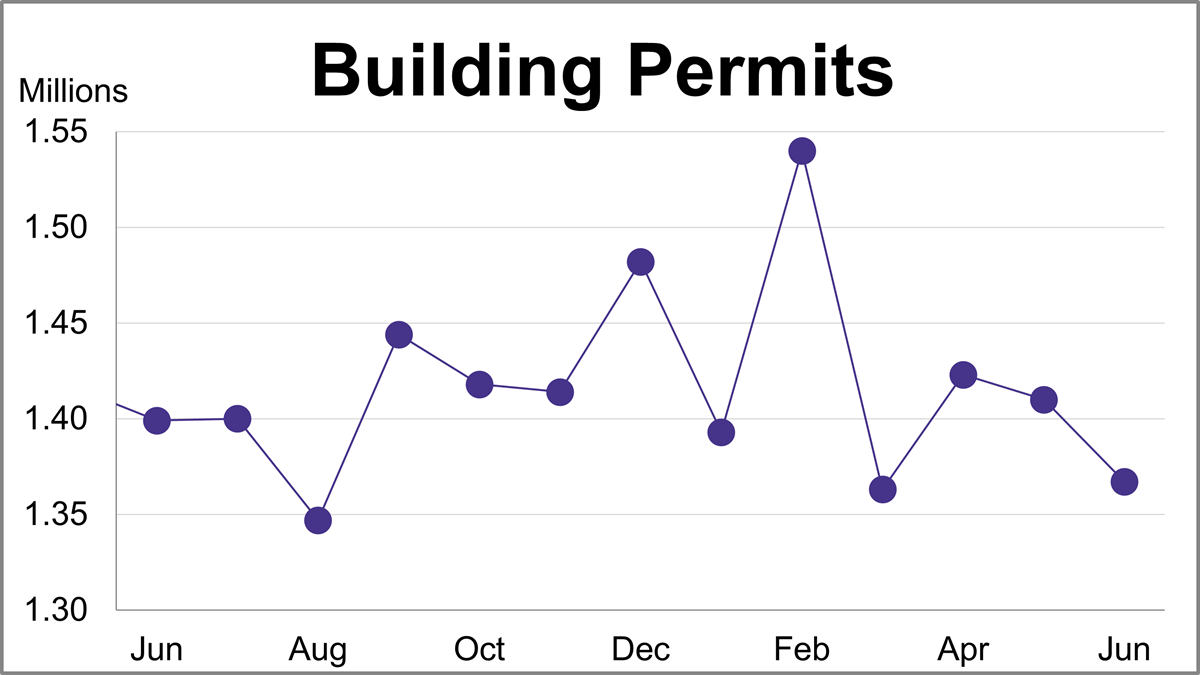

Building permits fell 3.0% in June to a seasonally adjusted annual rate of 1.367 million. The latest reading missed the forecast of 1.400 million.

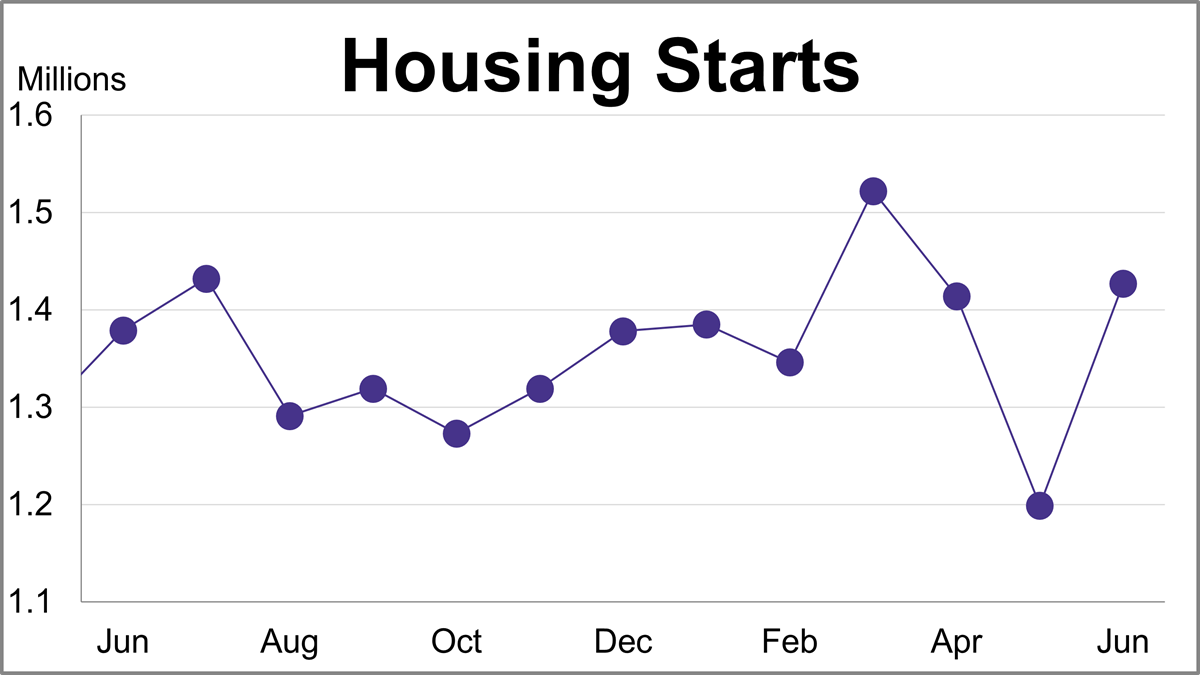

Housing starts jumped 19.0% in June to a seasonally adjusted annual rate of 1.427 million, beating forecasts driven by a massive surge in multi-family units.

Discover the top 10 most-read charts from the first half of 2026, covering historic market valuations, record margin debt, recession indicators, and global index performance.

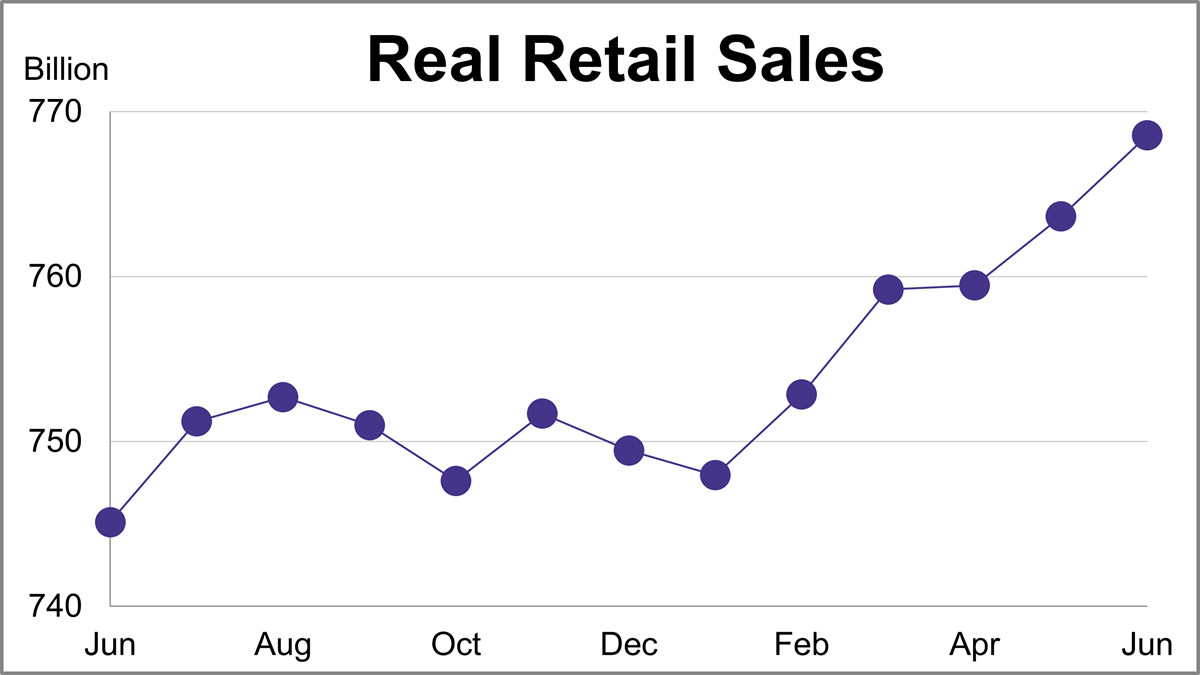

Nominal retail sales were up 0.22% month-over-month and up 6.72% year-over-year in May. However, after adjusting for inflation, real retail sales were up 0.64% month-over-month and up 3.15% year-over-year.

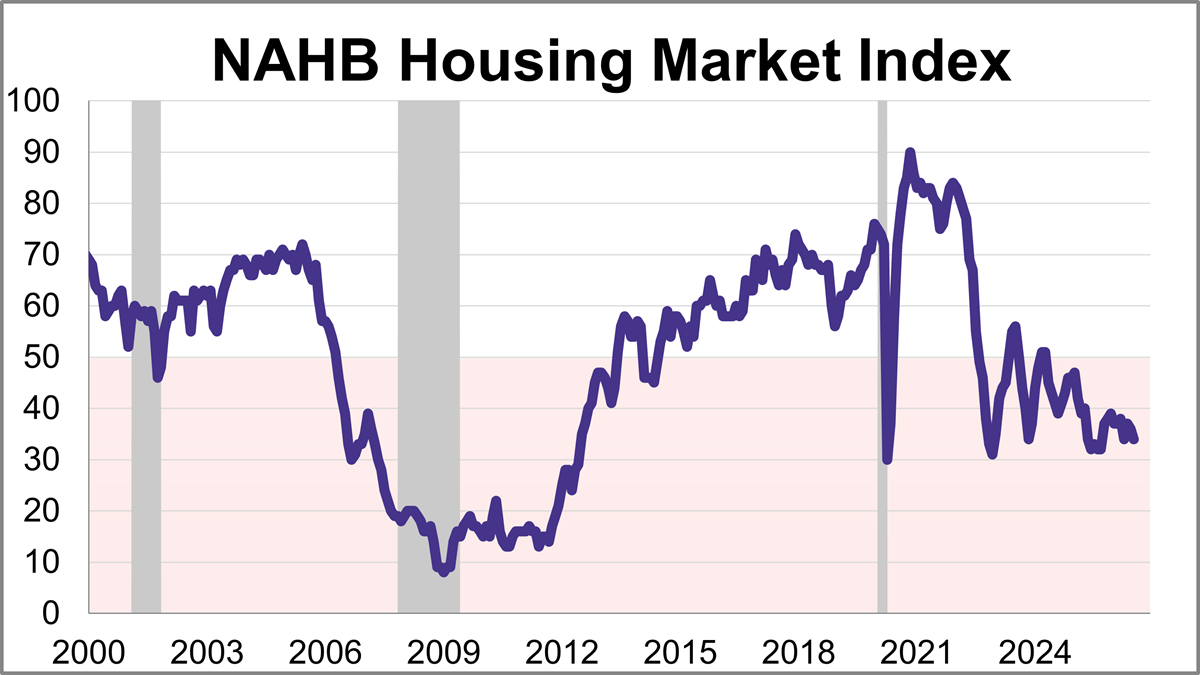

Builder confidence edged lower in July as ongoing affordability challenges continue to affect the housing market. The National Association of Home Builders (NAHB) Housing Market Index (HMI) fell 2 points from June to 34 this month, marking the 27th consecutive negative reading.

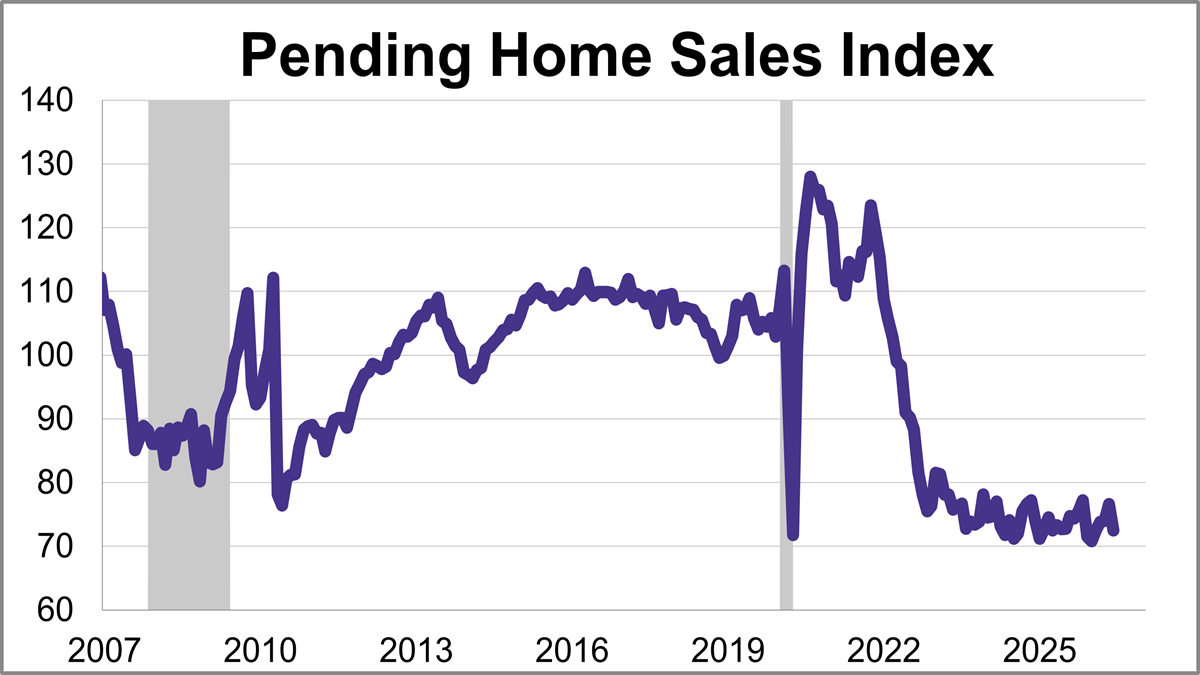

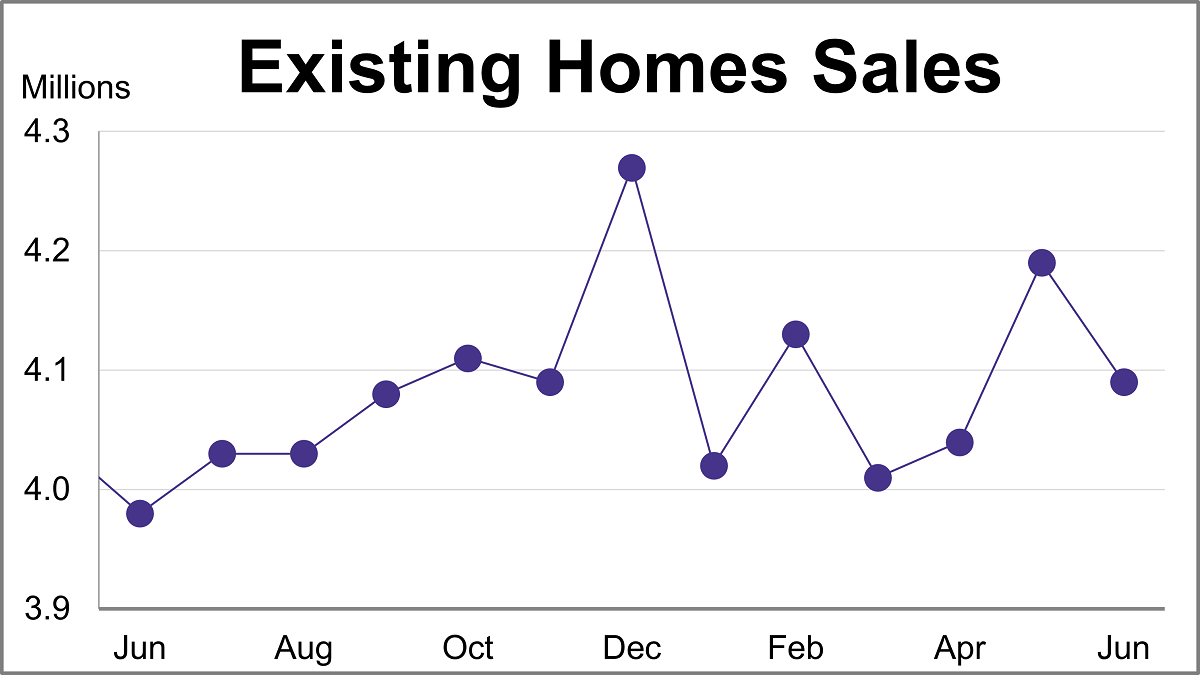

The National Association of Realtors® (NAR) pending home sales index sank 5.4% in June to 72.5, the lowest level since January.

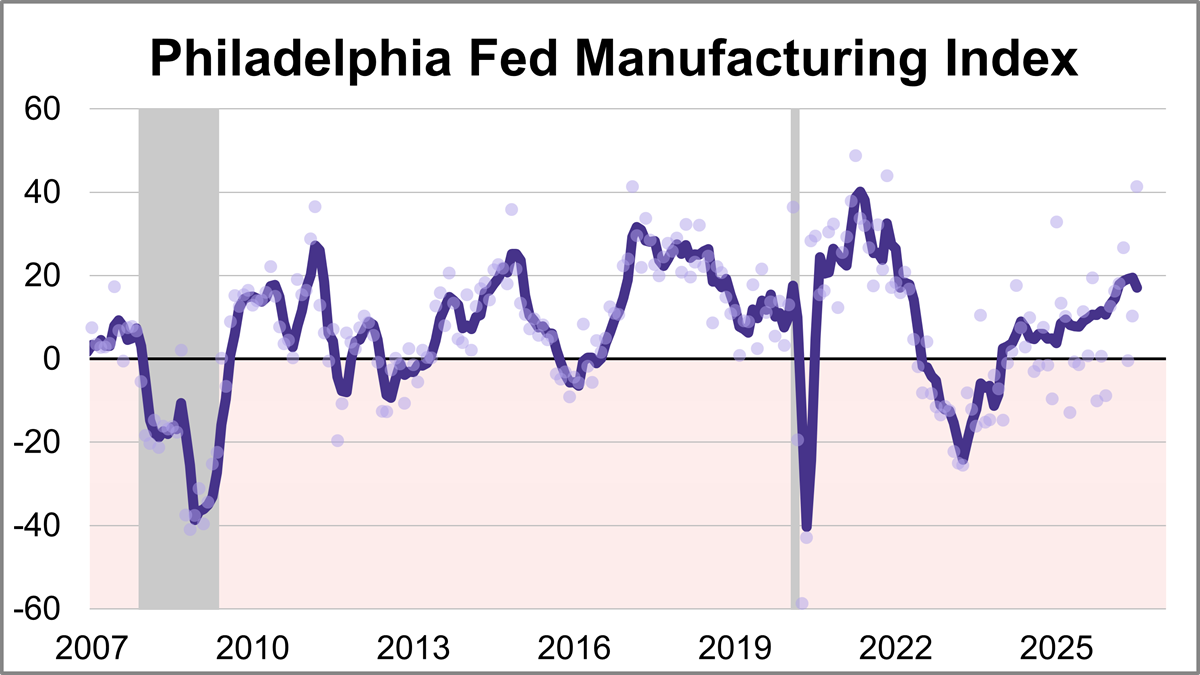

The Philadelphia Fed manufacturing index showed activity expanded significantly in July, with the index jumping 31.1 points to 41.4. This marks the highest level for the index since November 2021 and was more than triple the forecast of 12.7.

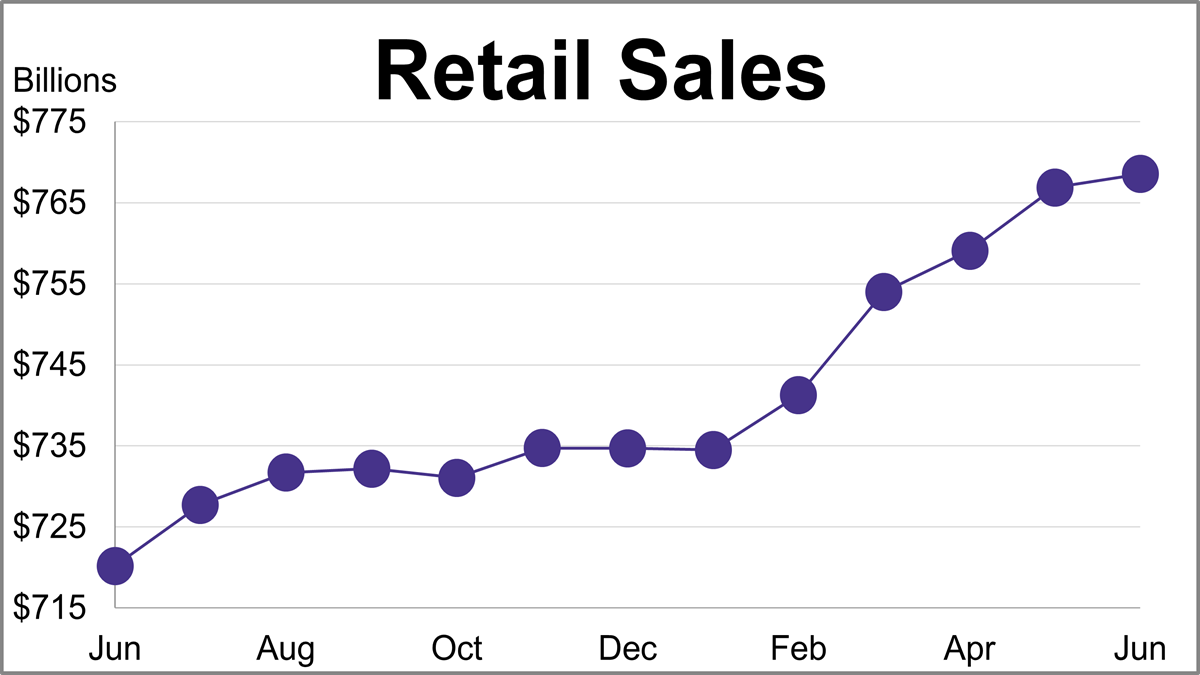

U.S. headline retail sales increased for a fifth straight month, rising 0.2% to $768.6B in June, while core retail sales fell unexpectedly by 0.2%.

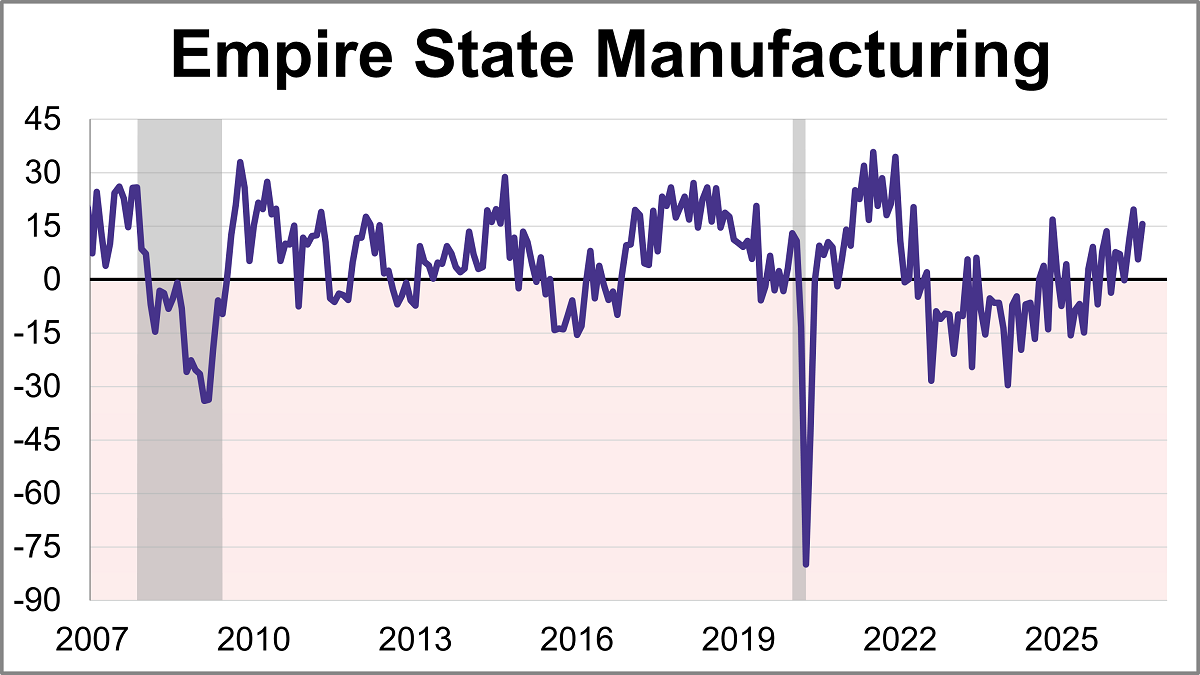

Manufacturing activity grew significantly in New York State, according to the Empire State Manufacturing July survey. The diffusion index for General Business Conditions remained in positive territory for a fourth straight month, jumping 9.9 points to 15.6 and coming in above the 9.3 forecast.

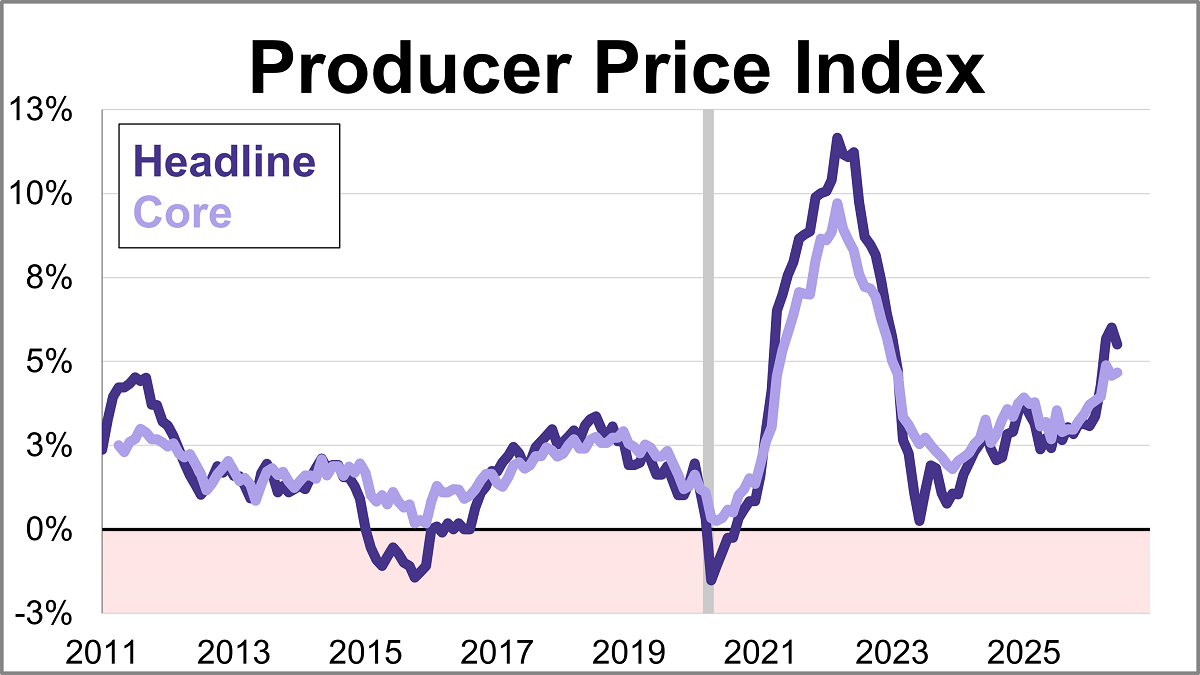

The Producer Price Index (PPI) experienced its largest decline in over a year in June, with wholesale inflation dropping 0.3%.

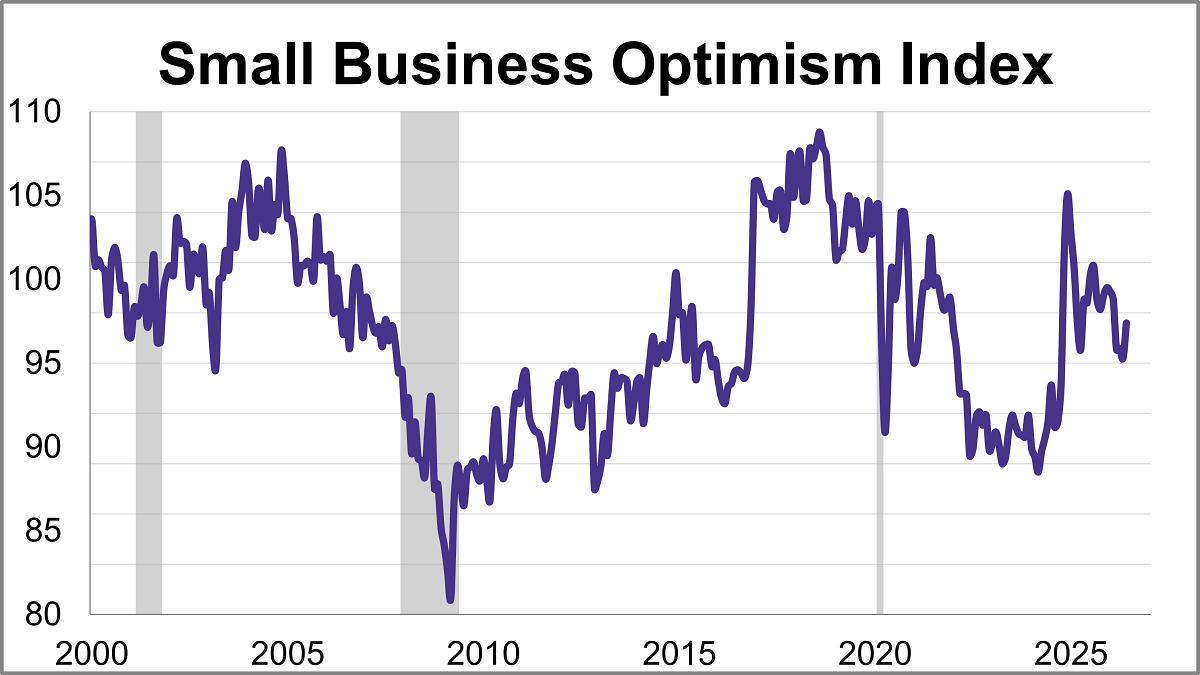

The NFIB Small Business Optimism Index rose 2.1 points to 97.4, reaching its highest level since February. However, the index remains below its historical average for a fourth straight month.

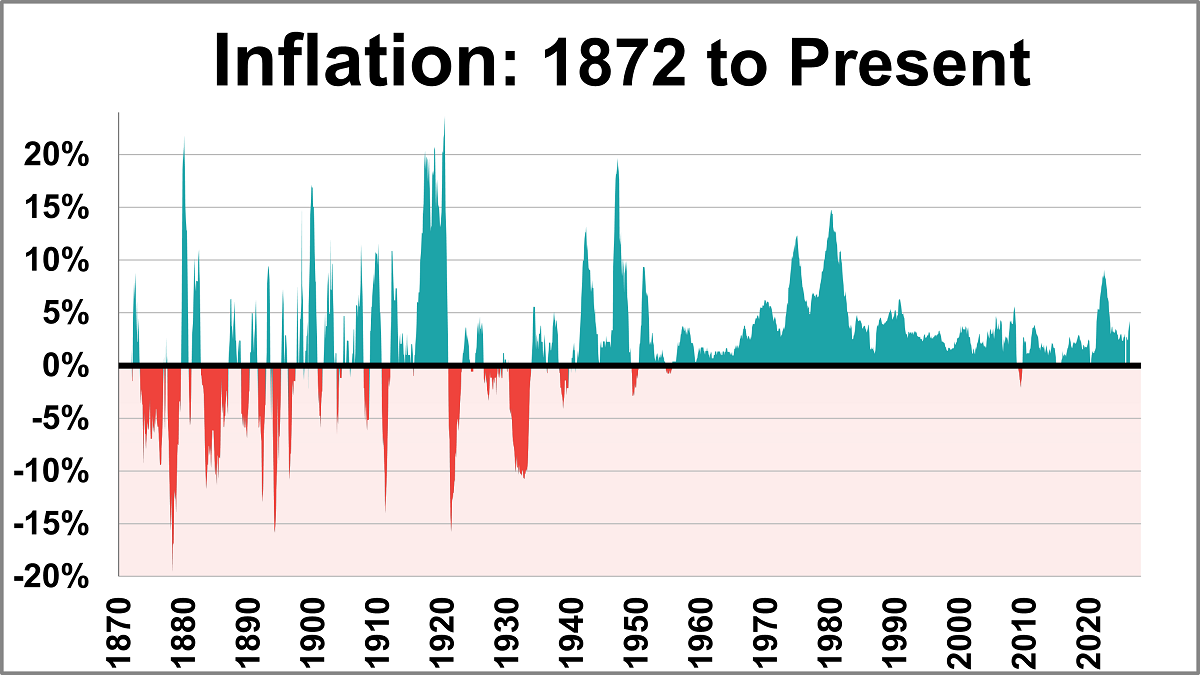

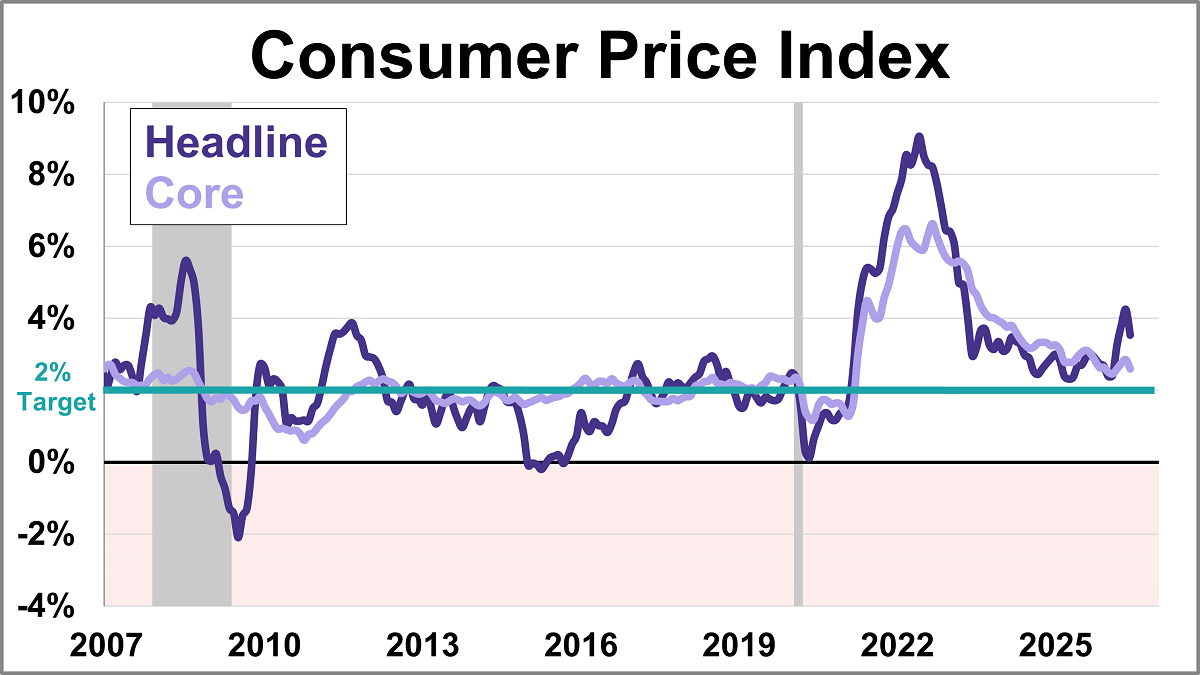

The June release of the Consumer Price Index for Urban Consumers (CPI-U) places the year-over-year inflation rate at 3.53%. This pushes inflation back below the post-WWII average of 3.72% for the first time since March. Meanwhile, this marks the fourth consecutive month that the current rate is above the 10-year moving average, which currently sits at 3.29%.

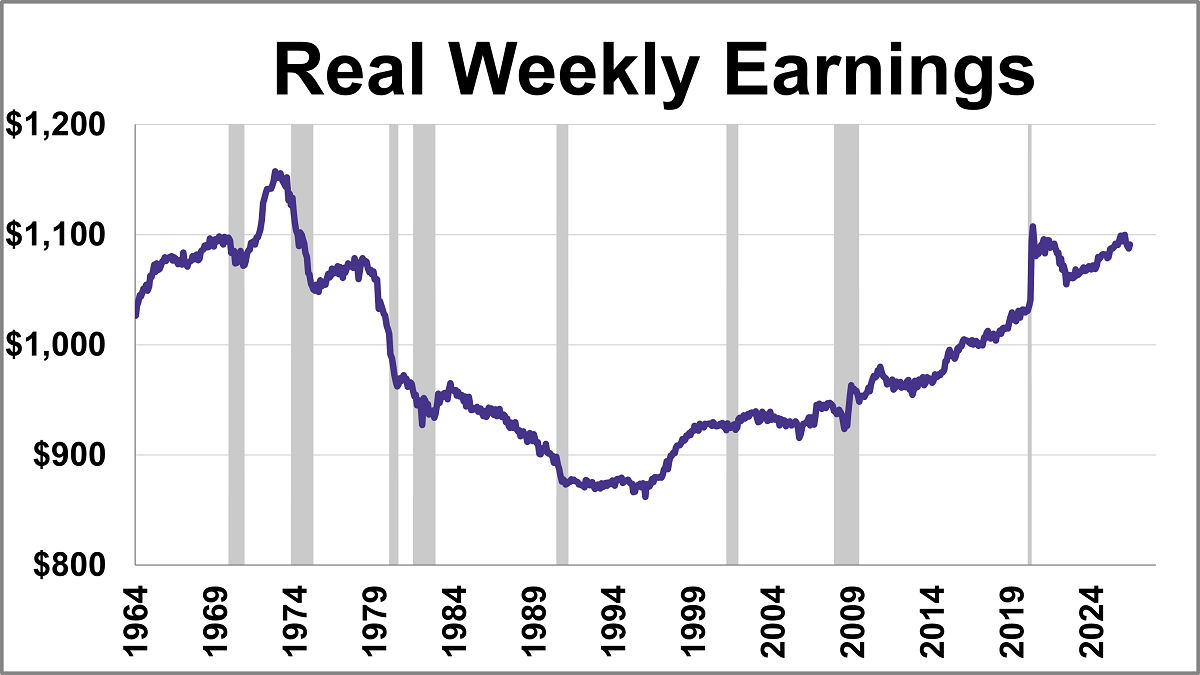

This series has been updated to include the June release of the consumer price index as the deflator and the monthly employment update. The latest hypothetical real (inflation-adjusted) annual earnings are at $54,560, down 5.7% from over 50 years ago.

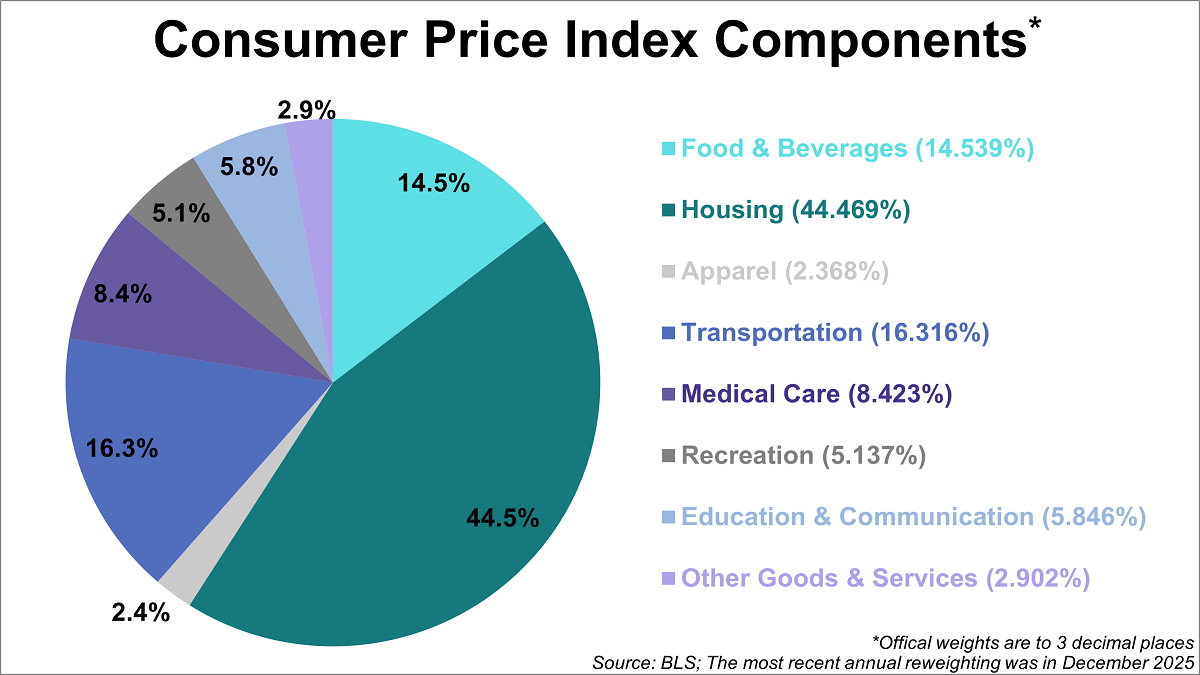

Inflation affects everything from grocery bills to rent, making the Consumer Price Index (CPI) one of the most closely watched economic indicators. The Bureau of Labor Statistics (BLS) tracks this by categorizing spending into eight categories, each weighted by its relative importance.

Inflation cooled for the first time in five months, coming in at 3.5% year-over-year in June. The headline figure for the Consumer Price Index (CPI) was lower than the 3.8% forecast.

Valid until the market close on July 31, 2026

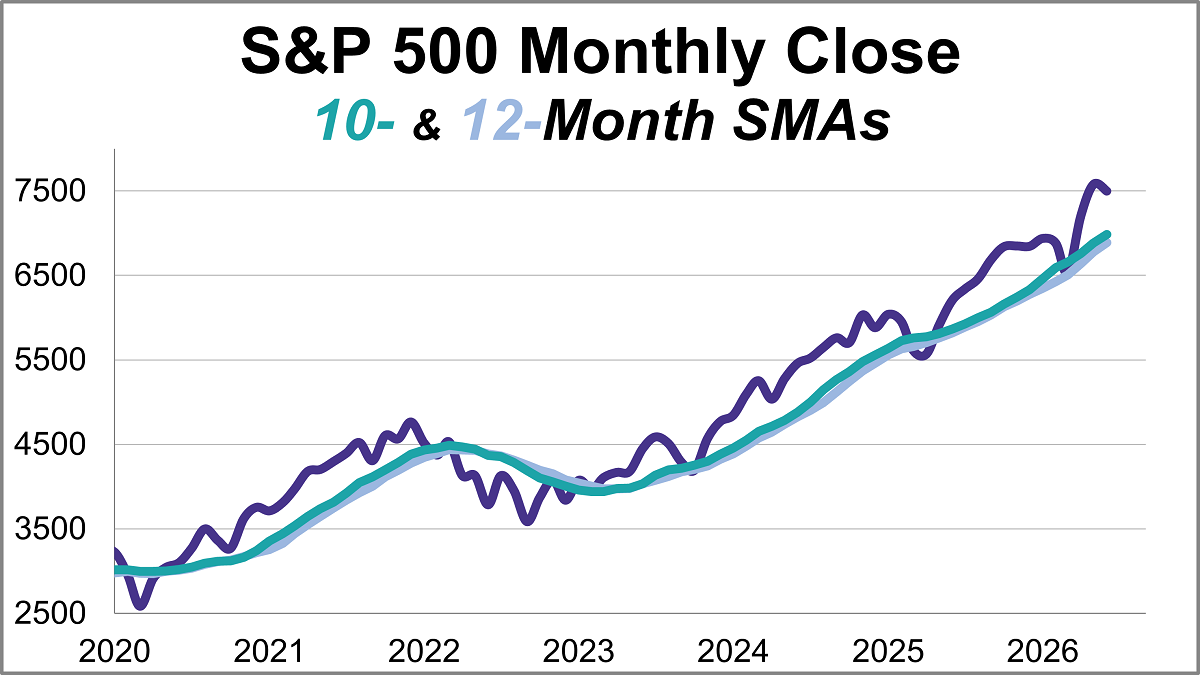

This article provides an update on the monthly moving averages we track for the S&P 500 and the Ivy Portfolio after the close of the last business day of the month.

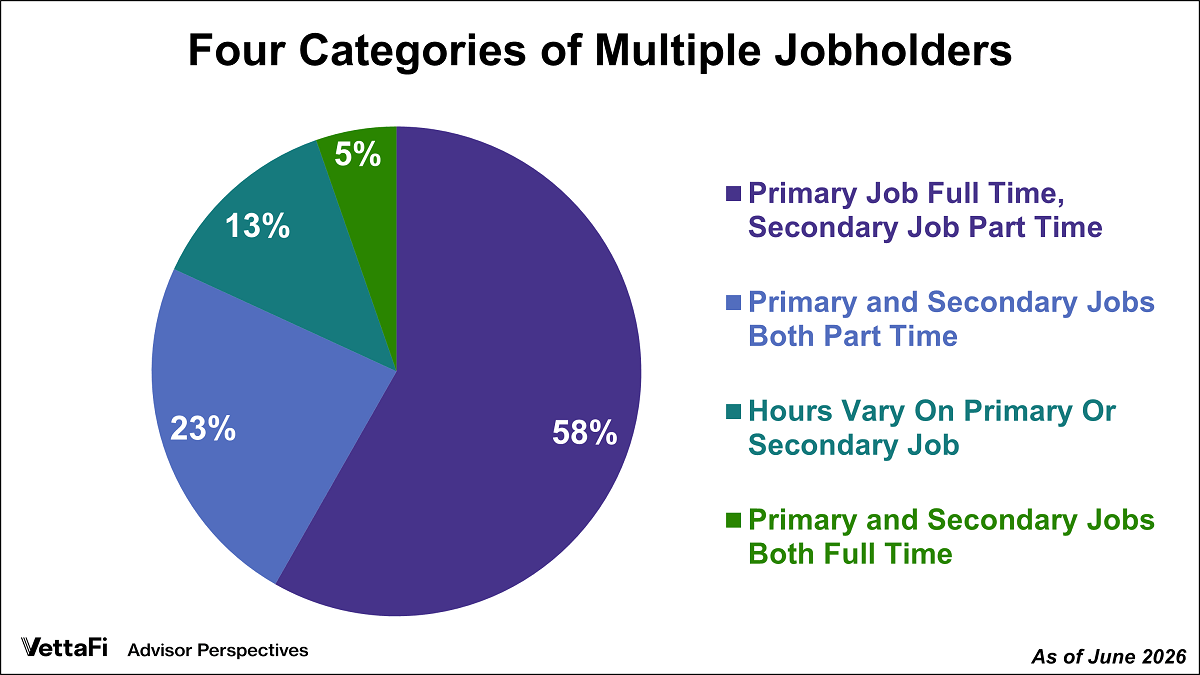

Multiple jobholders accounted for 5.2% of civilian employment in June.

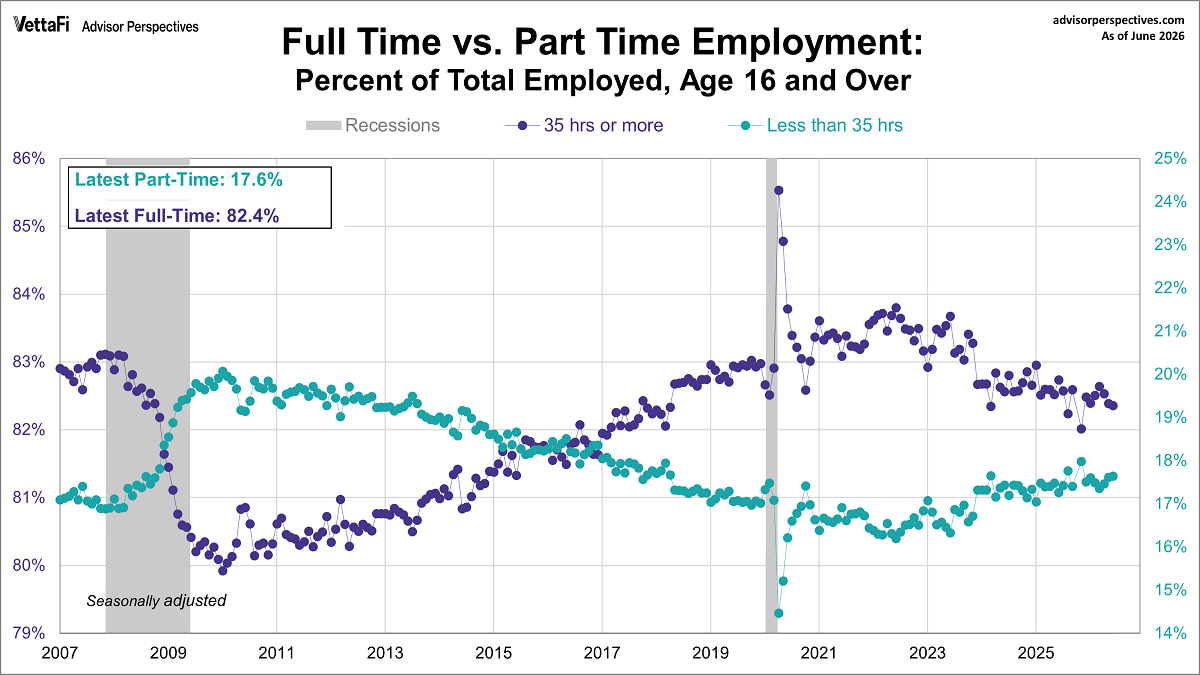

June's employment report showed that 17.6% of total employed workers were part time and 82.4% of total employed workers were full-time.

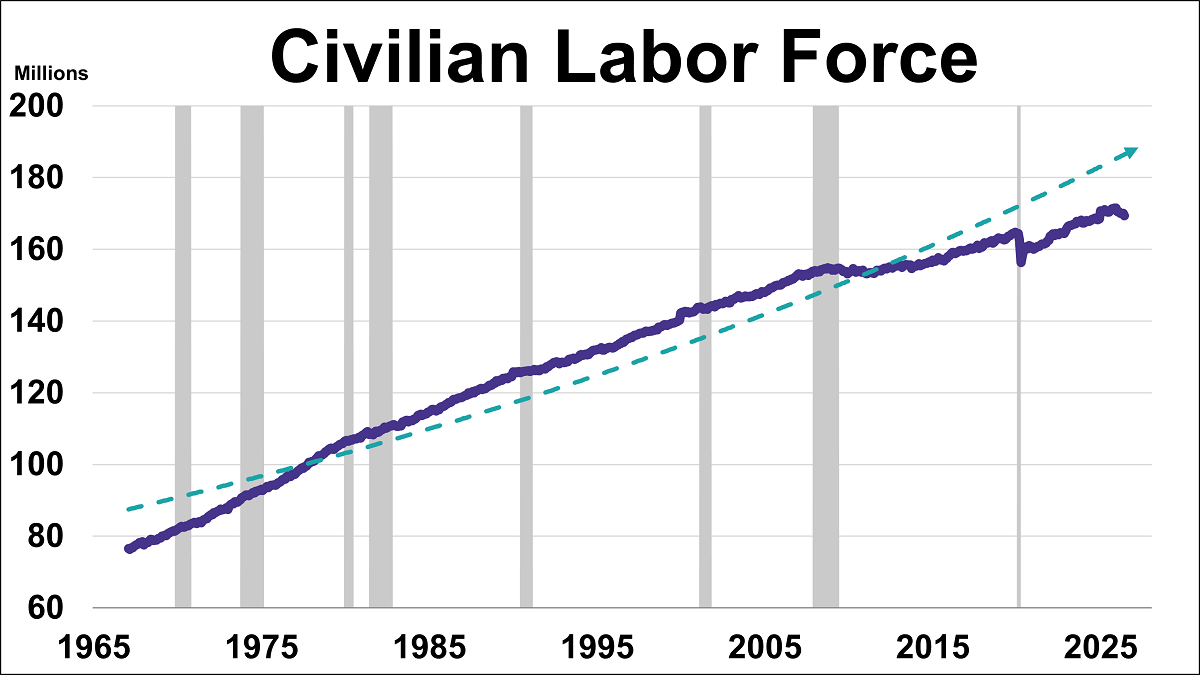

What does the ratio of unemployment claims to the civilian labor force tell us about where we are in the business cycle and recession risk?

Existing home sales unexpectedly fell 2.4% in June as the median home price surged to a record high of $440,600.

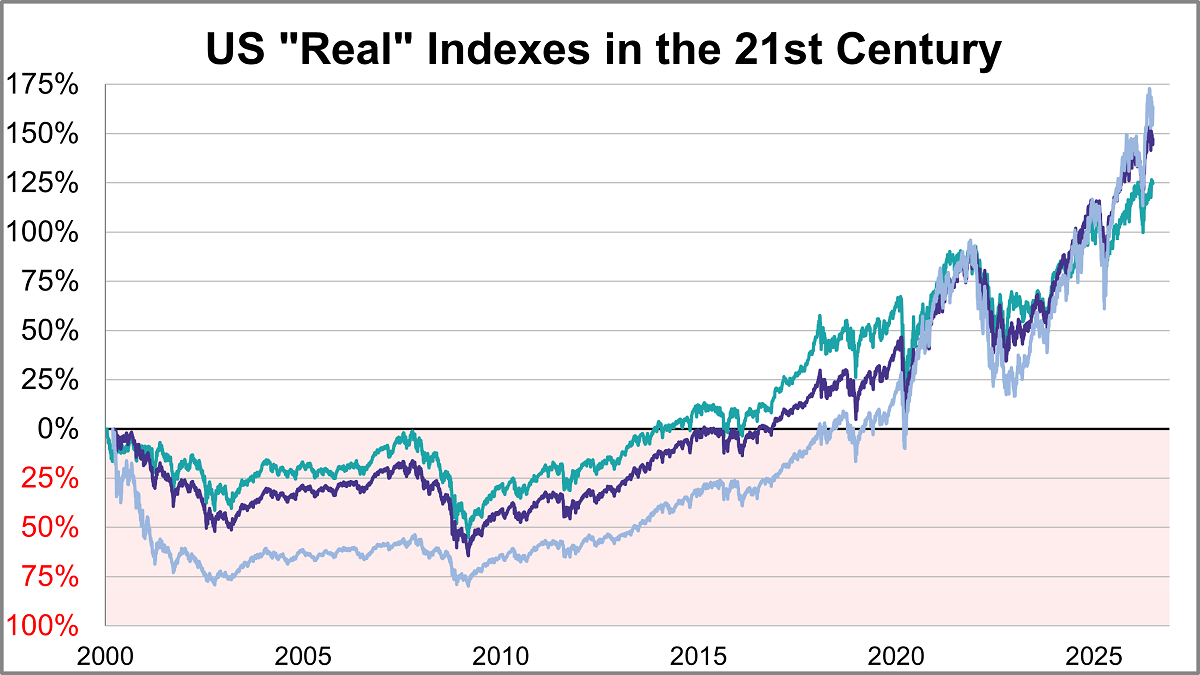

Here is a look at real (inflation-adjusted) charts of the S&P 500, Dow 30, and Nasdaq composite since their 2000 highs. We've updated this through the June 2026 close.

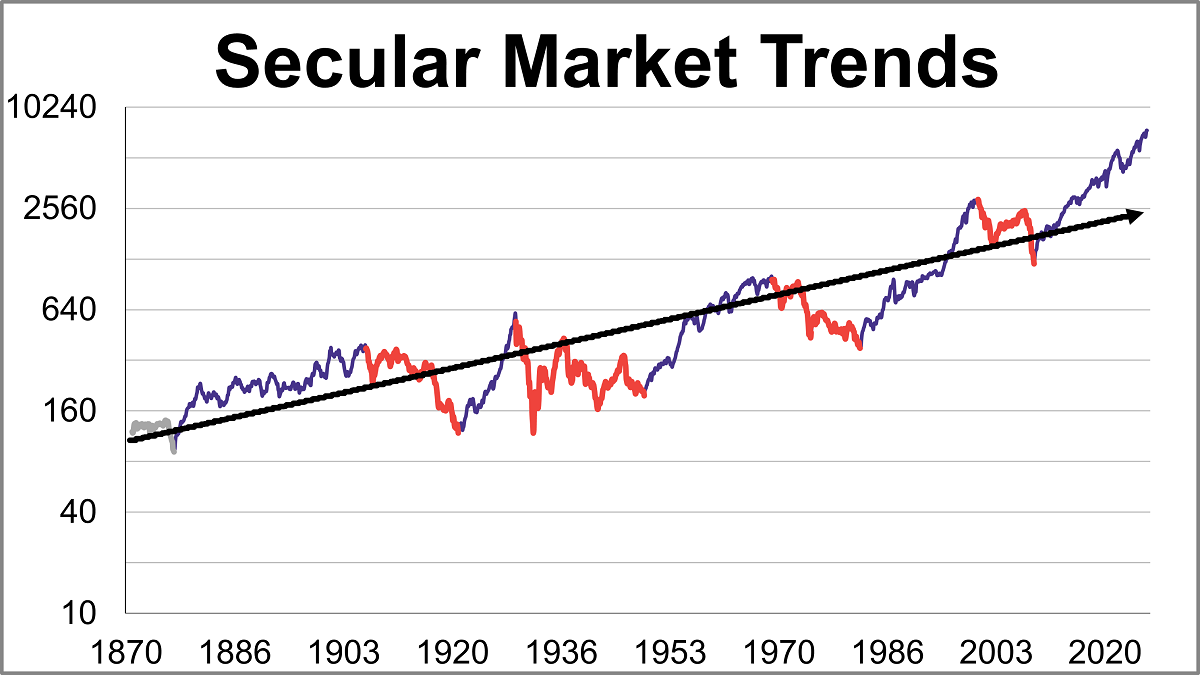

The S&P 500 real monthly averages of daily closes reached a its all-time high in May 2026. Let's examine the past to broaden our understanding of the range of historical bull and bear market trends in market performance.

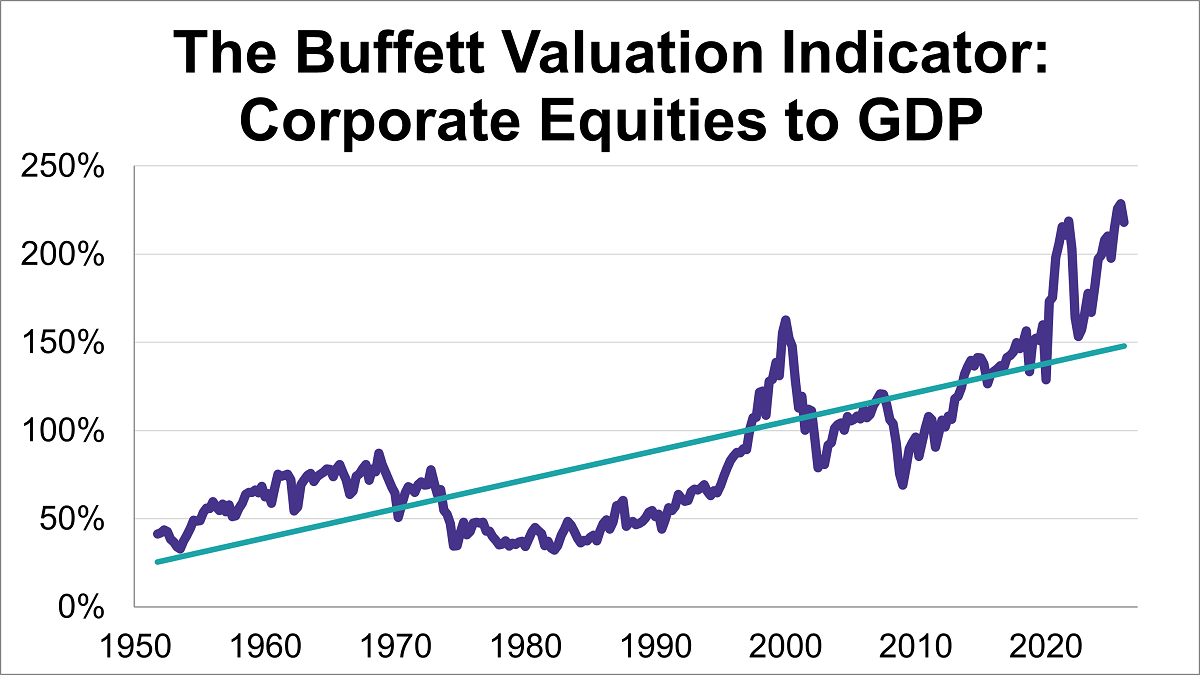

Following the Q1 GDP third estimate, the 'Buffett Indicator'—the ratio of corporate equities to GDP—now stands at 218.1%. This marks the fourth-highest reading in history.

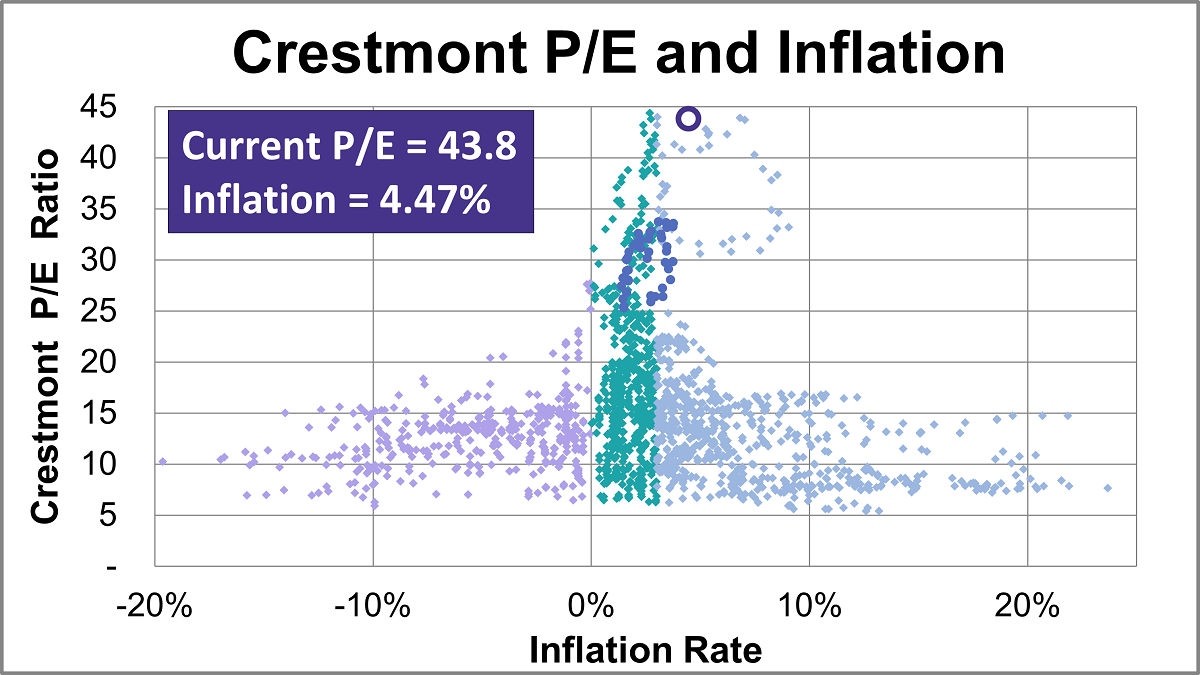

Based on June's S&P 500 average of daily closes, the Crestmont P/E of 43.8 is 185% above its arithmetic mean, 212% above its geometric mean, and is in the 100th percentile of this 14-plus-decade series.

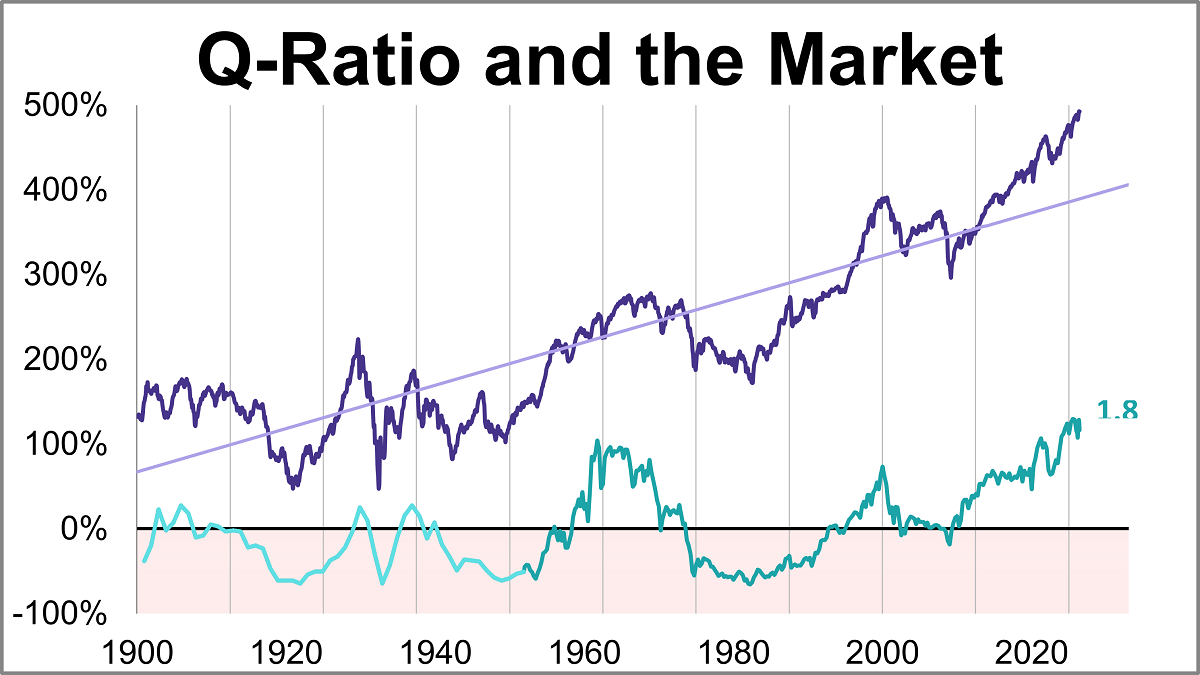

The Q Ratio is the total price of the market divided by the replacement cost of all its companies. As of June 2026, the latest Q-ratio is at 1.83.

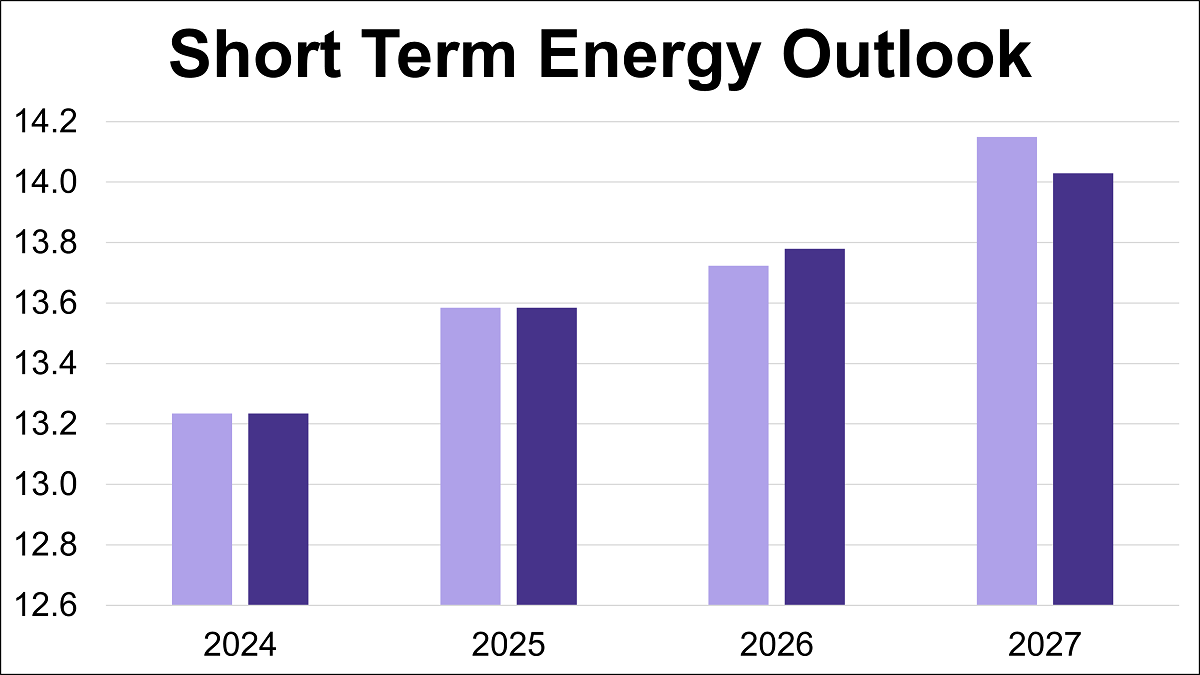

The U.S. Energy Information Administration (EIA) has released its latest Short-Term Energy Outlook (STEO), providing forecasts for energy markets. This article presents the annual production outlooks for crude oil, natural gas, and natural gas liquids (NGLs), comparing the July 2026 projections against the previous month's estimates.

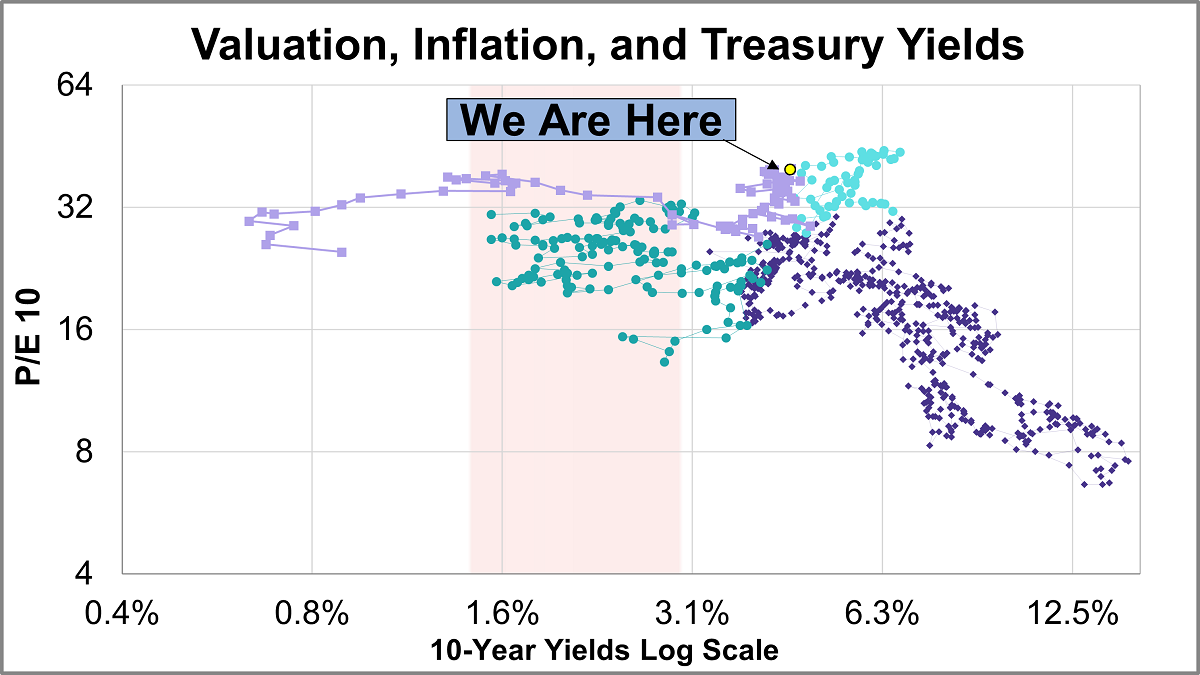

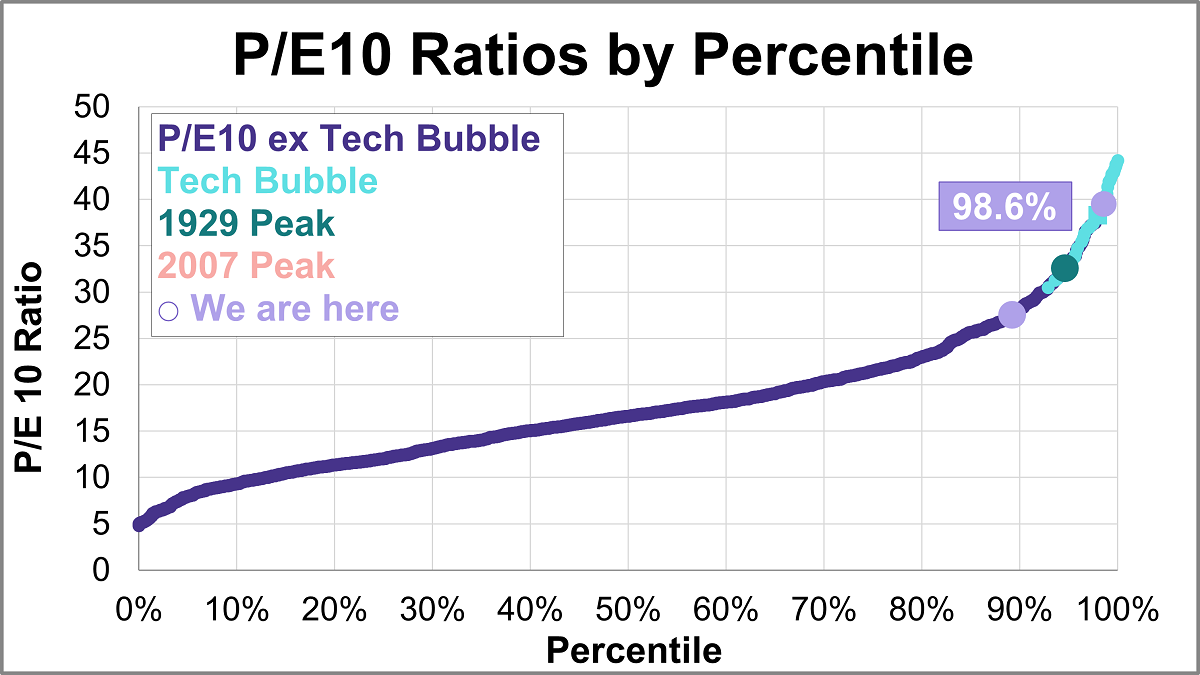

Our monthly market valuation updates have long had the same conclusion: US stock indexes are significantly overvalued, which suggests cautious expectations for investment returns. This analysis focuses on the P/E10 ratio, key indicator of market valuation, and its correlation with inflation and the 10-year Treasury yield.

Here is the latest update of a popular market valuation method, Price-to-Earnings (P/E) ratio, using the most recent Standard & Poor's "as reported" earnings and earnings estimates, and the index monthly average of daily closes for the past month. The latest trailing twelve months (TTM) P/E ratio is 25.3 and the latest P/E10 ratio is 39.5.

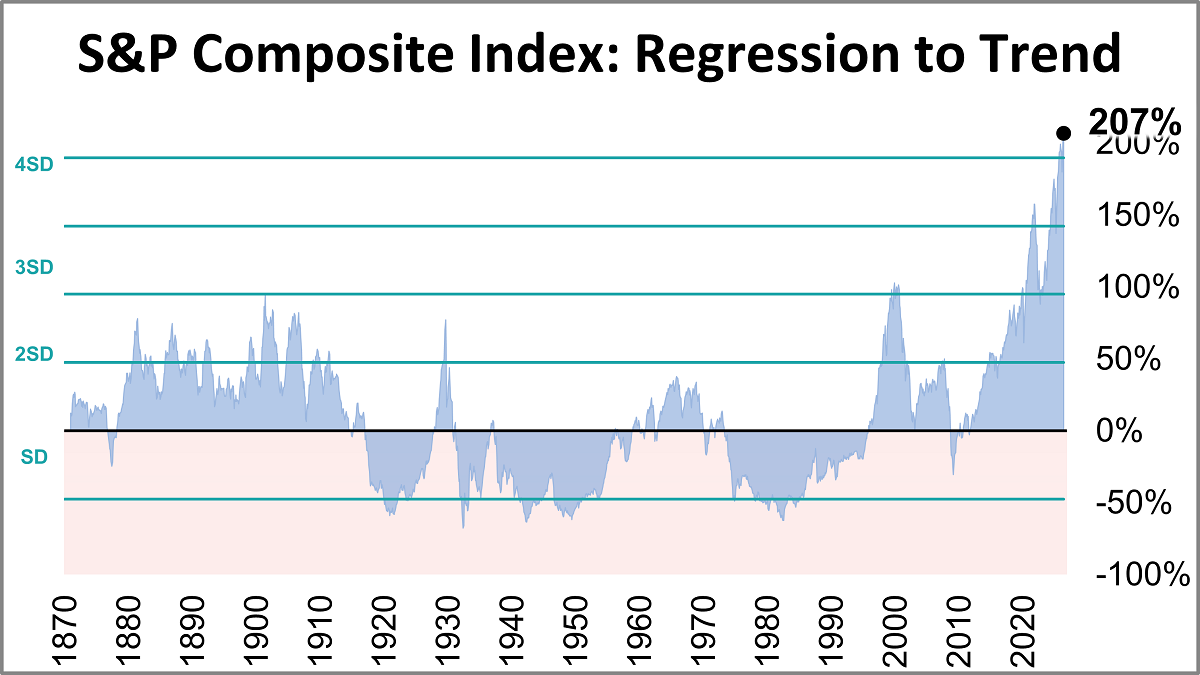

The inflation-adjusted S&P Composite Index was 207% above its long-term trend at the end of June.

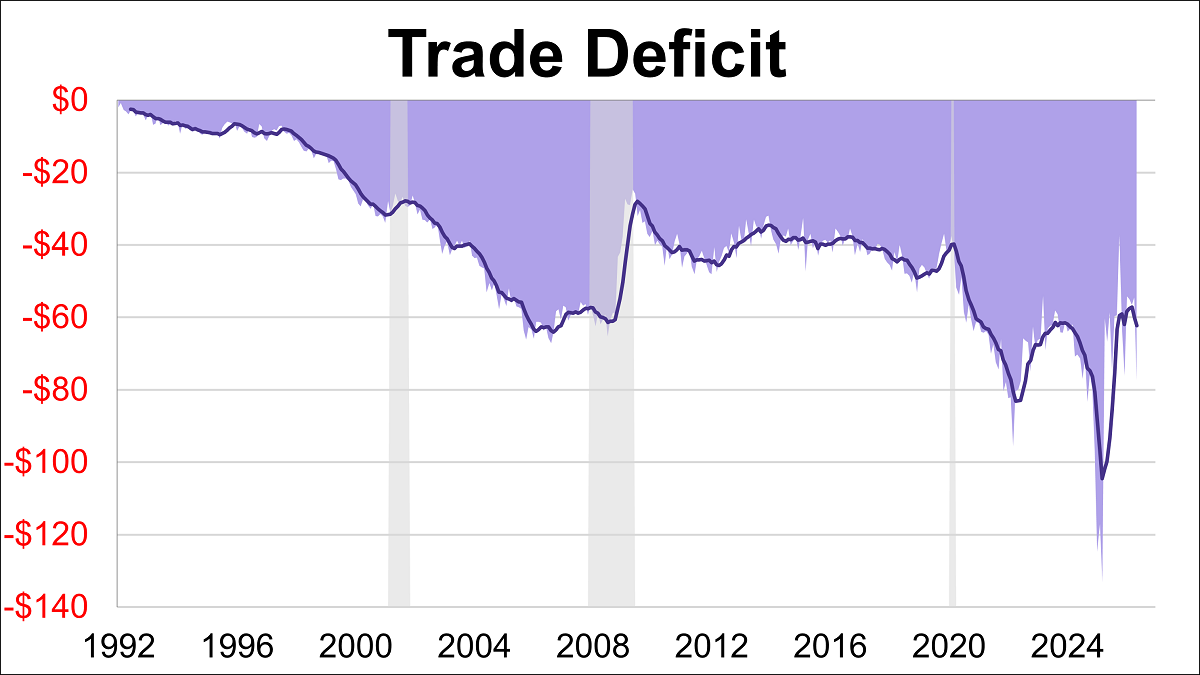

The U.S. trade deficit expanded over 40% in May to $77.59B, its widest gap since March 2025. The latest reading missed the forecast of -$78.30B.

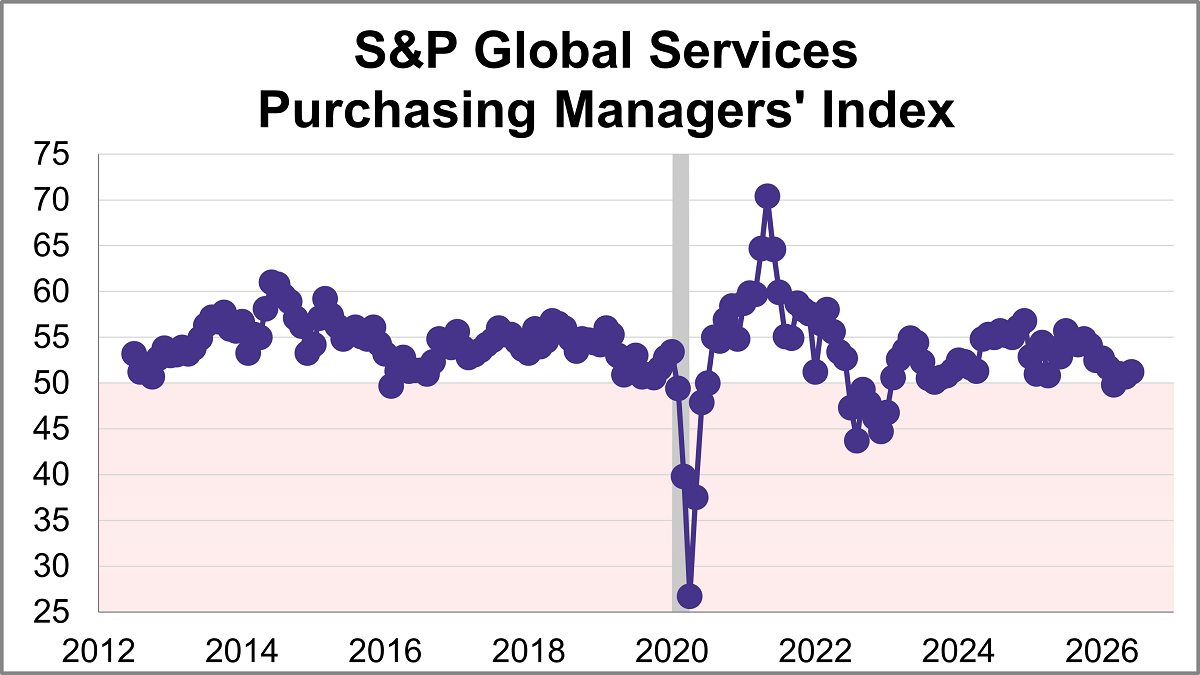

The June U.S. Services Purchasing Managers' Index (PMI) from S&P Global rose 0.5 points to 51.2, indicating a modest rise in service sector activity. The latest reading was just below the forecast of 51.3 and marked the strongest expansion in four months.

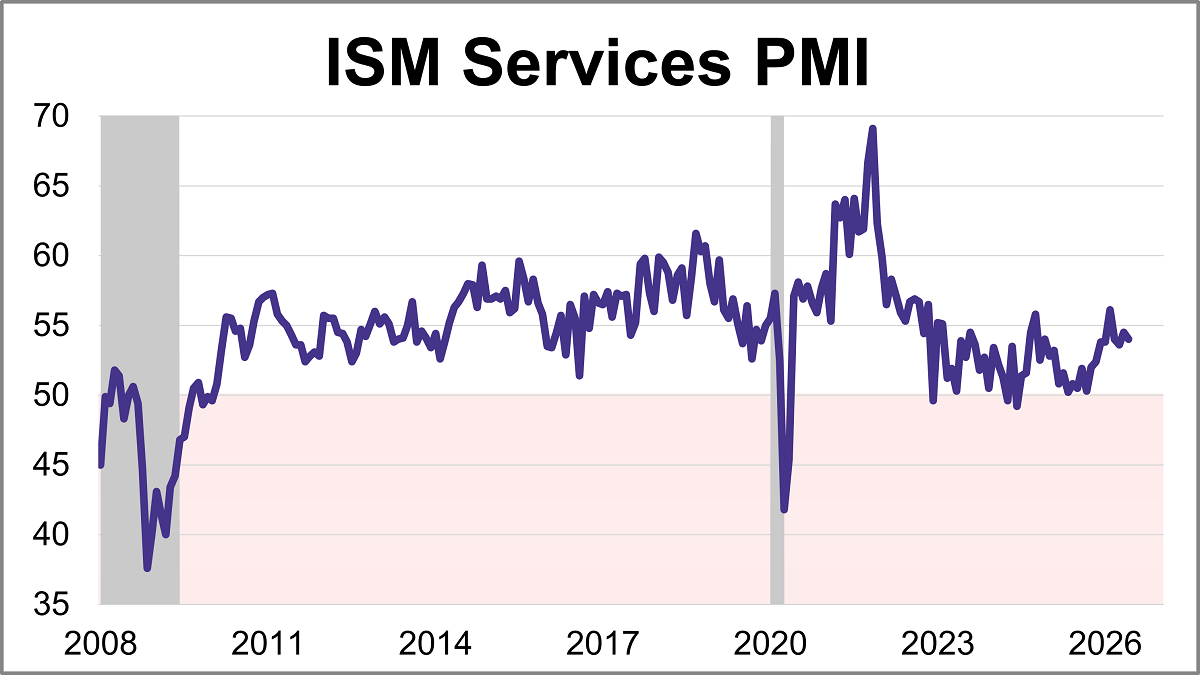

The Institute for Supply Management (ISM) released its June Services Purchasing Managers' Index (PMI), with the headline composite index at 54.0. This was slightly lower than the forecast of 54.2 but keeps the index in expansion territory for a 24th consecutive month.

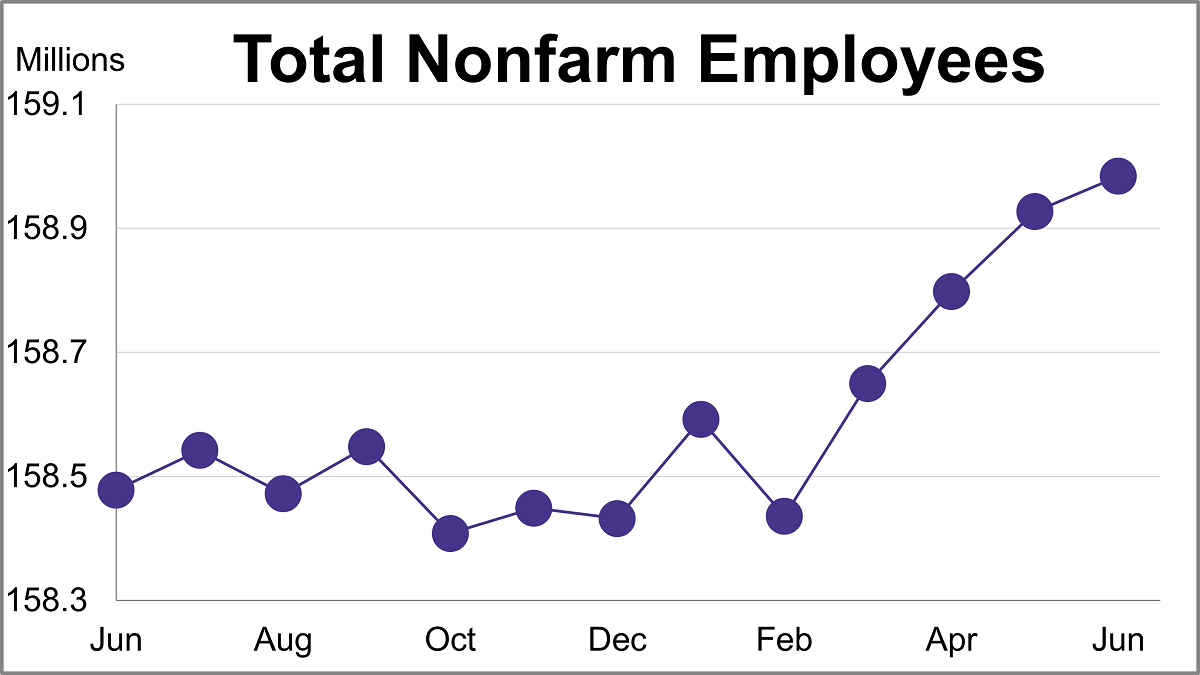

There is a general belief that there are four big indicators that the NBER Business Cycle Dating Committee weighs heavily in their cycle identification process. This commentary focuses on one of these indicators: nonfarm employment. In June, total nonfarm payrolls increased by 57,000 while the unemployment rate ticked down to 4.2%.