The sooner the mass of retail private credit managers realize they are zombies and give up the ghost, the sooner we can burn the whole thing to the ground and conjure a better model from the ashes. But there is no time like a crisis to have conversations about how to make the structure work better for everyone in the future!

Breakeven real rates can inform us how much of a total return portfolio’s realized risk premium would be required merely to catch up to the benefits of delayed claiming, arguably an inefficient use of the equity risk premium.

Advisors who run or plan to run ETF-based portfolios need to have a formalized trading methodology. For those who haven’t yet developed one, this article is intended to help accelerate progress and avoid some risks that may not be obvious to anyone who is primarily experienced with trading mutual funds.

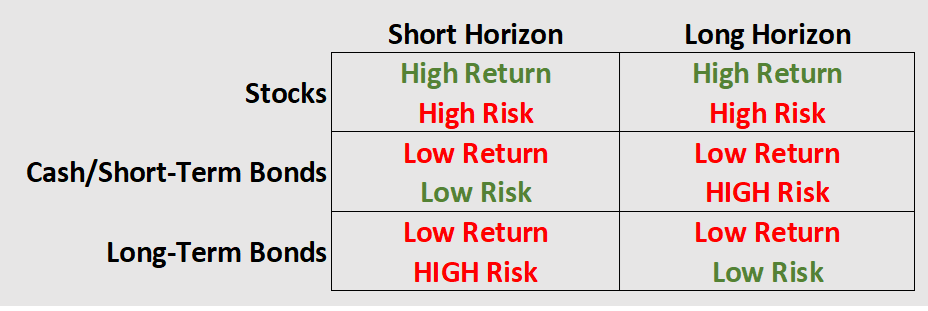

A portfolio of longish-term bonds held to a shortish-term horizon did appear to benefit from a drop and suffer harm from a jump in interest rates. This article’s purpose is to sharpen that observation and remove the ambiguity.

“Everyone knows” falling interest rates are good and rising interest rates are bad for bond investors. But “everyone” is generally wrong.

If a dividend is not a gain, then what is it? Here is my irony-drenched-but-accurate definition

I’ve identified long-term care as the greatest unsolved challenge in the field of goals-based retirement investing. This doesn’t make me Sherlock Holmes. Anyone who has requested a quote for LTCI knows we’ve got a problem.

Cathie Wood, CEO/CIO of Ark Investment Management, (in)famously predicted that her firm’s strategies could see a 40 percent annualized return over the subsequent five years. That prediction rounded the halfway pole and is now headed home, so this seems like a good time to check in on how it is faring

Last July, I issued an open letter to the annuity industry requesting the introduction of a product to meet the needs of independent advisors who adhere to a safety-first, goals-based investing philosophy. That call has been answered.

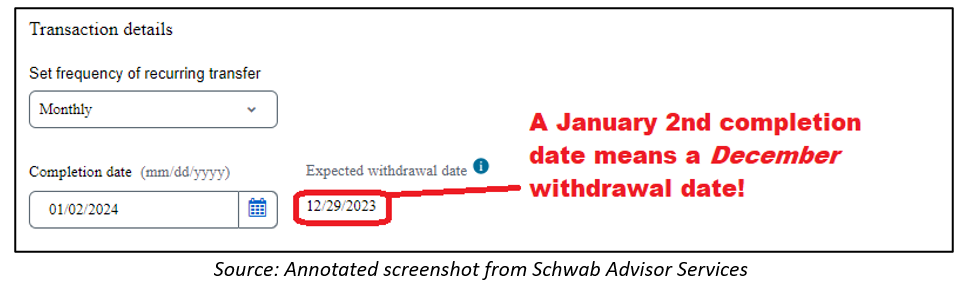

Advisors who set up recurring withdrawals at TD need to beware. With the transition to Schwab, those scheduled January withdrawals will take effect in December instead.

I previously discussed a method of applying long-run, risk-return insights to a goals-based approach to retirement investing. This article considers how to extend the process into the pre-retirement years.

While a goals-based approach divides a retiree’s liabilities (future spending goals/needs) and assets into separate pieces with separate mandates, it can be useful to see how they all stack together.

In investing, you can have a safe present or future value, but not both!

Common aphorisms and assumed truths about stock returns often imply the disappearance of risk over long horizons. Is that accurate?

The aim of this series is to move beyond the simplistic example of goals that exist at a single point in the future to consider retirement, the most common purpose for long-term investing for an individual.

We’ve known for a long time that CPI-adjusted lifetime guarantees are the ultimate bedrock for a secure retirement.

Nearly a year ago, I – provisionally and with qualifications – declared I-Bonds to be the fabled “free lunch” due to the remarkable 9.62% rate they were paying. That rate came down – a lot – so should you still buy them?