Parking your fixed-income assets in cash may seem like a safe choice in today’s volatile investing environment, but it’s actually a risky proposition. Here are three reasons why sitting on the sidelines can be a dangerous game.

For this edition of Bull vs. Bear, James Comtois, and Elle Caruso discussed the pros and cons of using single-stock ETFs to express opinions on stock earnings.

Despite economic uncertainty, we see compelling value in high-quality, liquid assets that we view as more resilient in the face of a potential recession.

Here are GMO’s updated forecasts for performance of various asset classes over the next seven years.

Markets are still facing uncertainties regarding the impact of the Federal Reserve’s aggressive rate hikes and quantitative tightening, a potential economic slowdown, and the likelihood of other unforeseen consequences of financial disintermediation.

It’s hard to open up a newspaper these days and not see a scary story about the debt ceiling debate. The Biden Administration is saying that a “default” is approaching if an agreement isn’t reached soon.

The view by many is that sustainable investing is concessionary in that financial results are forgone in order to achieve sustainable outcomes. Our historical analysis shows that this assertion isn’t true and that unique ESG data can be predictors of company results.

The Northern Trust Economics team shares its outlook for U.S. growth, employment, interest rates, and inflation.

The Federal Reserve’s latest 0.25% interest-rate hike has likely capped one of its most aggressive policy-tightening cycles in 40 years. And the cumulative 5% policy rate increase in just over a year is now starting to have an effect on rate-sensitive sectors and inflation.

Working with a skilled OCIO provider can help you position your portfolio to benefit from investment opportunities and avoid uncompensated risks.

The CBOE Volatility Index (VIX) is down about 26% for the year, but investors shouldn’t assume there won’t be market fluctuations ahead, especially with quantitative traders increasing their activity as of late.

The current economic and investing environment remains one of the most challenging and difficult to navigate in recent times. We have stubborn inflation, economic resilience, geopolitical tensions, tight labour markets, rising interest rates, higher for longer monetary policy, QT, bank failures, overwhelming bearishness and now, issues surrounding the debt ceiling.

Rising rates in today's fixed-income markets have led to more attractive bond prices and higher yields, alleviating some of the challenges facing income investors.

The paradox that this marriage potential created at the college was that the odds are good, but the goods are odd. This is the statement that can be made for common stock investing today.

Muni investors have more reasons for optimism than concern as California tackles a projected $31.5 billion budget deficit.

What's on the menu? Heading into a profits recession, there are many things to consider when building a portfolio. Here's a sneak peek at what we are serving up.

The future of money is uncertain, and speculation about what comes next is all over the place. The Federal Reserve note "dollar" is the world's reserve currency, but its seat on that throne is no longer secure.

If 2022 was the zenith of the post financial crisis bull market, the intervening year and a quarter is a relatively short period from which to conclude that a turn in the secular tide has taken place. That said, several indicators have already begun to signal a change in trend.

When an exchange traded fund (ETF) is associated with high or low beta, what exactly does that entail? It all boils down to risk and how much an investor is willing to accept, which is different for everybody.

Profit margins have remained elevated in the U.S. for a decade, and in a new white paper, GMO’s James Montier examines why that has been the case, ultimately finding the culprit in fiscal deficits.

Rising interest costs have sparked speculation about whether companies with loan-only capital structures might be vulnerable. Investment Director Cheryl Stober puts rising interest costs, debt service capacity and capital structures into context.

Analysis shows an extraordinary range of outcomes since the S&P 500's inception in 1928.

Doug Drabik discusses fixed-income market conditions and offers insight for bond investors.

Many investment strategists are forecasting that the U.S. economy could experience a recession in the next year or two.

As the US economy begins to feel the weight of the Federal Reserve’s rate hikes, investors have grown leery of US high-yield corporate bonds. On the surface, that makes sense. Historically, credit conditions soured when growth slowed.

Macroeconomic and geopolitical hurdles are slowing the full recovery of tourism.

What if I told you that future returns could approach zero? Such seems hard to believe, considering young investors piling back into the markets since the beginning of the year

One of my mentors once told me that "Hope is not a strategy" and since we can't predict the markets, I have decided to focus this blog on using Direct Indexing to attract new high net-worth clients.

The COT (Commitment Of Traders) data, which is exceptionally important, is the sole source of the actual holdings of the three critical commodity-trading groups, namely: Commercial Traders, Non-Commercial Traders and Small Traders.

Although affordability remains an obstacle, recent data offer reasons to be more constructive as broader conditions still appear supportive of home prices.

Economic moats, also called business moats, are competitive advantages that help a company maintain long-term profits and market share over competitors.

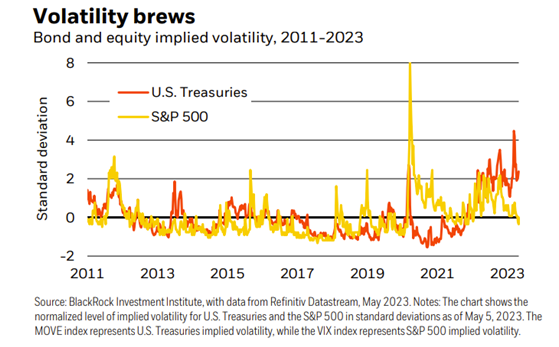

We think the U.S. debt limit showdown will spark renewed volatility in markets. That risk reinforces why we stay invested and cautious by going up in quality.

What follows a technical default? We hope we will not need to find out.

As the credit market grows more stringent, investors should consider high-quality, longer-term bonds. Here are some fixed-income strategies.

The economy co-exists and interacts with broader society, including government. Public policies—and the political processes that determine them—can change the economy in deep and lasting ways. We may not like them, but we can’t ignore them.

Review the latest Weekly Headings by CIO Larry Adam. Tighter lending standards still pose a risk. The debt ceiling issue will get resolved. The earnings outlook is improving.

This week’s inflation numbers were mostly positive and benign for the U.S. economy as well as for the Federal Reserve (Fed) and confirms our view that, at least for now, the Fed is done increasing interest rates for this monetary tightening cycle.

Political brinkmanship in Washington adds to concerns about the economy.

Review the latest portfolio strategy commentary from Mike Gibbs.

It would appear that the decline in European natural gas prices has contributed to an increase in Eurozone GDP estimates for the year. Once prices crossed below $50, GDP estimates began to rise, and now the consensus expects .6% GDP growth from the Eurozone this year.

There is a disconnect between the Fed’s message regarding taking a pause in hiking interest rates this year and the market’s expectations of rate cuts.

The Banking emergency arising with mid-sized, regional banks is a direct consequence of policy decisions. Examine the causes of bank failures in 2023 and the potential for larger contagion.

A wage-price spiral isn't imminent in Europe, but inflation may take a while to descend.

Tom Hauser, Co-Head of Corporate Credit, discusses his current views on opportunity in leveraged credit. Economist Paul Dozier updates on the latest economic data.

Portfolio manager John Paul Lech explores the defining changes of the last three years. Here he explains how he is navigating the new era of rising interest rates and financial tightening.

Saving for college can be daunting. Many parents don’t know how prepared they will be for college costs in the future. Parents face the question of how much to save and which funding vehicles to use.

China reported year-over-year inflation last night at just 0.1%, 0.2% lower than expectations. Clearly, China’s reopening is not creating price pressures, which brings the strength of the reopening into question.

The longer-term risks of sticky inflation, monetary policy changes, and slowing economic growth continue to challenge the markets. Within this uncertain backdrop, Franklin Income Investors’ Ed Perks shares his latest outlook and the investment opportunities he sees across fixed income and equities.

The central bank likely won't have enough reason to hike rates again this cycle. In fact, we wouldn't be surprised to see one or two rate cuts later this year.

We are presented with this decision in finance a lot. There is a small probability of something bad happening and a large probability that everything will be fine. What do you do to insure yourself against something bad happening? Because there is no such thing as a free lunch.