India is making bold moves in ‘new energy’ and decarbonization and our recent trip reinforced our reasons to remain bullish.

Recruiting talent is a basic ingredient for business success. Companies that are more inclusive in their recruiting will discover better-qualified employees, which can bolster competitive advantages and help deliver better outcomes for investors.

Going into the Fed meeting today it seemed like the consensus was toward a skip, pause, or possibly a full-on stop in raising interest rates going forward. Indeed, there are reasons to be optimistic about inflation coming down despite currently sticky “core numbers.”

The Federal Reserve paused in June but raised its estimates for the policy rate later this year. We expect a July increase but remain skeptical about subsequent hikes.

The meaning of "wealth" goes far beyond having a lot of money. It's more about what money can do for you.

For the first time since beginning the current tightening cycle in March 2022, the Fed opted against raising the federal funds rate at the June 14, 2023, FOMC meeting. The decision officially ends a run of 10 consecutive interest rate hikes by the central bank.

State and local tax revenues sank in April, yet we believe most governments have strong fiscal positions, with ample reserves and budget flexibility to manage the decline.

Using our AI engine, we prompted a description of the Atlanta Fed’s Flexible CPI. What we got was a pretty decent explanation.

Macroeconomic uncertainty has sparked questions over the durability of the traditional 60/40 portfolio—highlighting why investors may want to add alternative investments to the mix.

It’s been a challenging year for many managed futures strategies but they continue to offer long-term potential for portfolios. The benefits of trend-following strategies are numerous and worth consideration for inclusion in any alternative sleeve.

Chief Economist Eugenio J. Alemán discusses current economic conditions.

The Federal Reserve will meet this week and announce its decisions on Wednesday.

Interest-rate volatility on shorter-duration assets is running near historical highs, even as rate changes begin to level off.

The Euro Stoxx 50 Index is up about 13% year-to-date. Not a bad return for a region whose largest economy is in recession, and whose second largest is facing one of the worst inflation fights in decades.

In this article, we explore three of those important economic releases from the past week: the S&P Global Services PMI, the ISM Services PMI, and the trade balance.

Municipal bonds posted negative total returns in May amid continuing heightened volatility. Interest rates rose throughout most of the month as banking concerns abated, economic data exceeded expectations, comments from the Federal Reserve turned more hawkish, and the debt ceiling negotiations remained contentious to the very end.

Corporate bonds that fund environmental, social and governance (ESG) initiatives continue to capture investor hearts and minds. But ESG-labeled bonds come in different stripes, so investors need to discern among the good, the bad and the occasional ugly ones merely posing as ESG bonds.

Advisors parking cash in short-term T-Bills yielding are missing out on potential capital appreciation. The current fixed income market provides an opportunity not seen since the financial crisis to earn total return from longer-dated, high-duration bonds.

In this article, we will compare the three largest U.S. real estate ETFs by market capitalization: Vanguard Real Estate ETF (VNQ), Schwab US REIT ETF (SCHH), and Real Estate Select Sector SPDR Fund (XLRE).

With their ability to act as an inflation hedge, diversified, and return enhancer, commodities should be considered an important portfolio allocation over the long term.

A broadening out in market performance would help bolster a more sustainable stock rally, but that hinges on increasing clarity for monetary policy, recession risk, and bank stress.

Healthcare companies are beginning to explore how artificial intelligence (AI) might unlock efficiencies for patients and medical systems. But to transform science fiction into reality, AI applications in the sector must prove that they can improve business profitability to deliver returns for investors.

Investor activism in Japanese companies has been the subject of a fair amount of recent conjecture. Specifically, foreign investors have been concerned about the relative prevalence of minority interest, the ghosts of fading Keiretsus on Japanese companies’ financial statements.

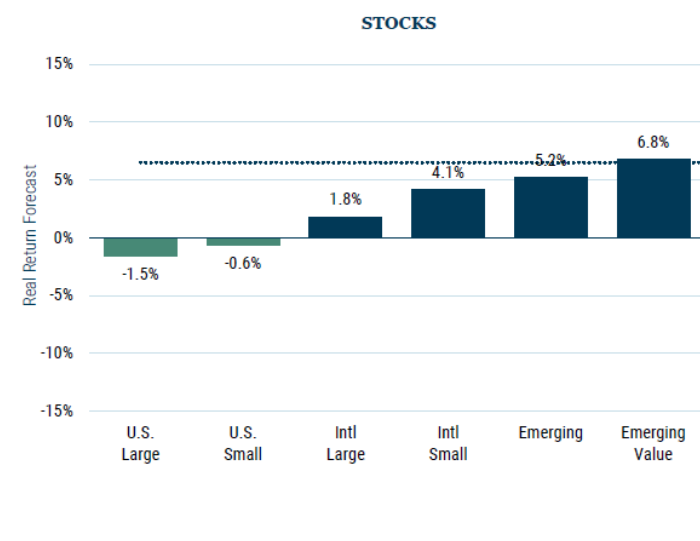

GMO has published a new seven-year asset class forecast.

A perennial challenge faced by all big or small, developed or developing economies is achieving sustainable economic growth that boosts standards of living and financial stability. Globalization has been the road that brought economies to that destination.

For more than a year now, there’s been ample discussion about whether or not the U.S. economy is in or approaching a recession. The surprisingly strong May jobs report out last Friday appears to have allayed some of those concerns.

With several EM countries facing elections in the next 12 months, Eric Spencer, Senior Research Analyst on Loomis Sayles' Global Emerging Markets Equity team, weighs in on potential risks and opportunities.

Wall Street is a strange place. In 2017, the top Wall Street banks published over 40,000 pieces of research… every week. Yet investors read less than 1% of that, according to Quinlan & Associates.

As a result, many are looking to capitalize on this trend by investing in ETFs that focus on AI companies. In this article, we will cover the top 5 ETFs to consider when investing in this sector based on their YTD performance.

We like both John Deere and Caterpillar. Both are A-rated companies with solid balance sheets, similar market caps, and similar long-term debt-to-capital ratios.

In many respects, COVID-19 was not a temporary disruption.

The Eurozone just entered a recession as the region posted two consecutive quarters of negative economic growth. The manner in which it entered a recession is a bit quirky.

Franklin Equity Group Portfolio Managers Blair Schmicker and Daniel Scher reflect on the ever-evolving landscape of the commercial real estate, and the answer to that question might surprise you.

While the retirement of several high-profile CIOs has generated ample news, and headlines, there’s been very little press coverage about OCIO as a potential solution. We find this perplexing.

While it has been months since the latest regional bank failure, many advisors remain concerned. They fear that the issues that caused runs on Signature Bank and Silicon Valley Bank have not receded.

In several recent blog posts and weekly Bull Bear Reports, we discussed our concern over the narrow breadth of the rally in 2023.

In economics we often talk about cycles. “Business cycle theory” is an entire academic sub-field whose basic idea is that economic history really does repeat itself. Not in every detail, of course, but as a recurring sequence of expansions and recessions.

Despite high volatility in the bond market during the first half of the year, what's surprising is how much didn't change.

Copper is currently trading around $8,300 a ton, down approximately 26% from its all-time high of nearly $11,300, set in October 2021. According to Citigroup, the metal could top out at $15,000 a ton by 2025, a jump that would “make oil’s 2008 bull run look like child’s play.”

Emerging markets (EMs) are a big, heterogeneous universe of economies and markets that can be subject to big volatility. They also are a large and fertile hunting ground for investment opportunities. Stock picker Emily Fletcher offers a grand tour of the “wild” EM equity landscape.

In a difficult year such as 2023, rebalancing between asset classes that are declining may seem a futile exercise. But rebalancing, even in down markets, remains vital to keeping a portfolio within the right risk/reward ratio and is a key element of the value that an advisor can provide to their clients.

While the Fed wants to retain optionality on further hikes and affirm rate cuts are not on the horizon for this year, we anticipate that slowing economic momentum and easing inflation pressures will lead to the beginning of an easing cycle in 2024.

When it comes to their equity portfolios, US investors have historically exhibited a high degree of home-country bias. But in today’s fast-changing global market landscape, they may find that there are good reasons to rethink regional allocations to stocks.

Anne Walsh, Chief Investment Officer for Guggenheim Partners Investment Management, joins Bloomberg TV to discuss fixed-income market opportunities, managing climate change risk, and the Fed’s path forward.

As markets continue to respond to an uncertain macroeconomic environment, the current fundamentals in the municipal bond market are creating an investment opportunity to capture strong after-tax total returns according to Stephen Dover, Head of Franklin Templeton Institute.

The Fed’s refusal to pause rates through the first five months of 2023 raises the odds of a hard landing. The magnitude of the yield-curve inversion has increased the risk inherent in the US banking and financial systems. The impending recession is unnecessary and self-inflicted.

This article will examine four real estate ETFs that investors and advisors can consider for their portfolios in 2023. Whether investors are seeking exposure to a specific sector or a diversified portfolio, there is a real estate ETF available to meet their needs.

If price stability is the legal mandate of the Bank of Japan (BOJ), and the central bank’s official target for price stability is 2%, as measured by the Consumer Price Index (CPI),* then why are fluctuations in prices the norm for Japan?

The debt ceiling crisis has been averted—but this short-term relief might come at the cost of greater future peril. Franklin Templeton Fixed Income CIO Sonal Desai analyzes the debt-ceiling resolution and delves into the potential longer-term risks that rising public debt poses to financial markets.

Value equities have faced years of tough sledding, outside a run of outperformance following “vaccine day” and the lift-off from zero rates. Broadly, this has left value stocks extraordinarily cheap relative to growth. However, looking closer, the cheapest 20% of stocks – what we call “deep value” – trades unusually cheap today despite offering surprisingly attractive fundamentals.