Although a lot has changed since our last quarterly, its central theme – dispersion – feels like it’s only become more pronounced. We wrote last time that ‘‘we believe we’re entering a new era of dispersion in the performance of financial assets.’’

The general field called “credit” has seen massive innovation over the course of my career. An Oaktree colleague asked me about the developments that brought the credit sector to where it is today. I came up with the following list.

When I was preparing to write my December memo about artificial intelligence, Is It a Bubble?, I gained a great deal from speaking with some interesting techies in their thirties and forties. It’s stimulating to explore fresh territory and an absolute requirement for staying current as an investor.

We believe we’re entering a new era of dispersion in the performance of financial assets. Behind buoyant index averages are sharply bifurcated cohorts of winners and losers.

In the current installment of The Roundup, Oaktree experts explore the need for renewed vigilance in the direct lending market, discuss the future of private credit in Europe, identify the evolution of the high yield bond market, and reflect on the backdrop for emerging markets equities.

I’ve lived through several bubbles and read about others, and they’ve all hewed to this description. One might think the losses experienced when past bubbles popped would discourage the next one from forming. But that hasn’t happened yet, and I’m sure it never will.

One of the most prominent characteristics of the financial markets that I’ve detected over the years is their tendency to obsess over a single topic at a given point in time. Today it’s the recent string of episodes in sub-investment grade credit.

Often framed as rivals, private and liquid credit should instead be viewed as powerful complements for both issuers and investors. We believe these two markets are settling into a symbiotic coexistence, as the distinctions blur between the likes of direct lending and broadly syndicated loans.

Over the last 56 years, I’ve spent a lot of time making suggestions to clients regarding their investment processes and portfolios, and I’ve been on the client side as a member of various investment committees. But seldom have I been able to bridge the two, serving as an active participant in clients’ investment processes.

Investment assets – things such as stocks, bonds, companies, and buildings – have a value, which is sometimes referred to as their “intrinsic value”: what the asset is “worth” at a point in time. This value is subjective. It can’t definitively be found anywhere – not even by AI, as far as I know – and opinions will differ as to what it is.

The United States has been on a remarkable run: exceptional growth and innovation, multiple structural advantages, and the financial market dominance to match.

Private equity transaction volumes remain limited despite predictions for a boom in 2025. With interest rates remaining elevated and the economic backdrop increasingly uncertain, executing acquisitions and IPOs is proving a challenge, leading financial sponsors to hold portfolio companies for longer.

In the current installment of The Roundup, Oaktree experts explore various investment risks and opportunities, including the heightened demand for mezzanine financing, potential entry points for special situations investors, the limited competition for unrated asset-backed finance investments, and the growing need for specialized life sciences lenders.

Ever since interest rates got up off the floor in 2022, there’s been increased interest in credit, and that’s why I’m devoting this memo to it. It’ll come a little closer than usual to “talking my book,” but I think the subject justifies that.

Many people these days are on heightened alert for bubbles, and I’m often asked whether there’s a bubble surrounding the Standard & Poor’s 500 and the handful of stocks that have been leading it.

Oftentimes, we’re best able to understand something we’re interested in through analogies that clarify the matter by establishing connections between it and other parts of life.

In December 2022, I published Sea Change, a memo that primarily discussed the 13-year period from the end of 2008, when the U.S. Federal Reserve cut the fed funds rate to zero to counter the effects of the Global Financial Crisis, to the end of 2021, when the Fed abandoned the idea that inflation was transitory and readied what turned out to be a rapid-fire succession of interest rate increases.

In his latest memo, Howard Marks provides a follow-up to Sea Change (December 2022). He argues that the trends highlighted in the original memo collectively represent a sweeping alteration of the investment environment that calls for significant capital reallocation.

In his latest memo, Howard Marks discusses the essential choice in both investing and sports. Should you go for more winners or try to eliminate losers? That is, should you emphasize aggressiveness or defensiveness? This is a key decision that every investor has to make thoughtfully, and the answer can be different for each person.

In his latest memo, Howard Marks discusses five market calls he’s made during his career. He argues that investors seeking to know the market’s likely direction should focus on taking its psychological temperature and understanding the nature of cycles. Just as importantly, they should learn to control their own emotions and have the humility to know when not to make a call.

Howard Marks (Co-Chairman) and David Rosenberg (Co-Portfolio Manager, U.S. High Yield, Global High Yield, Global Credit) discuss topics from the June 2023 edition of The Roundup. They consider the evolution of the high yield bond market, investor optimism, and why this time might actually be different in financial markets.

In his latest memo, Howard Marks discusses the significance of the Silicon Valley Bank collapse. He argues that it likely doesn’t portend a wave of banking failures but may amplify preexisting wariness among investors and lenders, leading to further credit tightening and additional pain across a range of industries and sectors.

In his latest memo, Howard Marks writes that the investment world may be experiencing the third major sea change of the last 50 years. Events in recent years – especially the spike in inflation and the Federal Reserve’s response – appear to have caused a reversal of the market conditions that prevailed after the Global Financial Crisis and for much of the last four decades. Howard discusses what this potentially new era could mean for lenders, especially bargain hunters.

In his latest memo, Howard Marks weaves together some of the themes he’s explored in 2022 to explain what he believes really matters in investing and what doesn’t. He discusses the disadvantages of short-term thinking, the difference between volatility and risk, and the one word he believes defines the essence of investment excellence.

Over the years, I’ve explained at length why I’m not interested in forecasts, but I’ve never devoted a memo to explaining why making helpful macro forecasts is so difficult. So here it is.

I recently was asked by Patrick Schotanus of Edinburgh Business School to participate in their inaugural symposium on the subject of cognitive economics. The symposium took place at Panmure House, the final residence of the great economist Adam Smith, and the theme was the Market Mind Hypothesis (MMH), which Patrick developed.

Howard Marks’s latest memo argues that investors seeking superior performance must have the courage to depart from the pack, even though doing so means accepting the risk of being wrong. Thinking differently and better than others is key to outperformance, he explains, because in investing, it’s not enough to be right.

Howard Marks’s latest memo explores recurring investment themes to contextualize the current market correction and the bull market that preceded it. He discusses the role played by financial innovations like SPACs and cryptocurrencies and why he believes psychology, not fundamentals, primarily drives investment cycles – and likely always will.

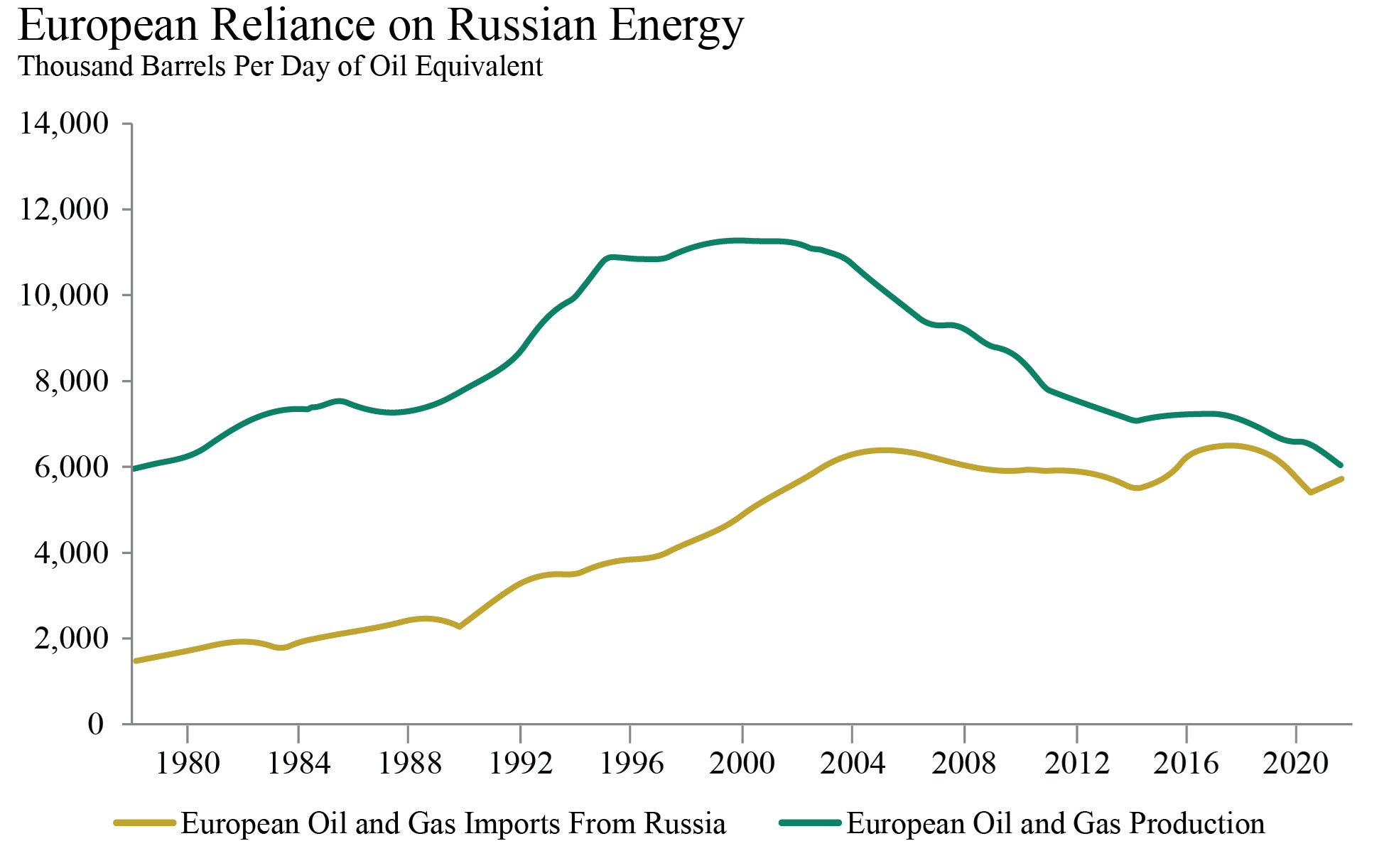

Howard Marks’s latest memo connects two seemingly unrelated trends – Europe’s energy dependence and U.S. offshoring – to explain why the pendulum of companies’ and countries’ behavior may be swinging away from globalization and toward onshoring. This shift will likely create risk for investors but also opportunities.

Howard Marks’s latest memo considers one of investing’s most fundamental questions: when to sell. Howard explains that it’s foolish to sell because prices are up and because they’re down – and why, most of the time, staying invested is ultimately “the most important thing.”

The last 20 months have taught us to question everything. What is the future of work? Can American democracy survive? Will Baby Boomers keep consuming more than their fair share? And what comes after “trillion”? Howard Marks’s latest memo examines paradigm shifts that could reshape the economy, markets and the world for many years to come.

Howard Marks doesn’t make bets on economic predictions. That’s especially true now when the biggest wildcard is inflation – a phenomenon no one fully understands. But just because something is unknowable doesn’t mean it’s unimportant. That’s why Howard has devoted his latest memo to a topic he largely disavows: macro forecasting.

Last year featured a jaw-dropping list of extremes, from a once-in-a-century pandemic to record-breaking market moves. Howard Marks writes in his latest memo about approaching the investment environment left in 2020’s wake – one generating many questions and no easy answers.

The dichotomy of “value” and “growth” investing has become a sharp stylistic divide. But is it helpful? Howard Marks writes in his latest memo how he views the art and science of value investing, especially in the increasingly efficient and complex world we face today.

In his latest memo, Howard Marks walks readers through the unusual characteristics of this year’s economy; the impact of Covid-related monetary and fiscal policy actions, including low interest rates, on today’s markets; and the possible ramifications of the Fed/Treasury’s rescue efforts. What does it all mean for investors who face an environment marked by some of the lowest prospective returns in history?

Several months into the Covid-19 era, Howard Marks takes a step back to consider the global health crisis, the economic fallout and the U.S.’s response to date. He also shines light on how one might – or might not – view the current circumstances in the framework of a market cycle.

U.S. stocks have managed a remarkable advance in the past several weeks as optimism outweighed concerns about the economic recovery and worsening Covid-19 cases. Has this been appropriate or irrational? Howard Marks shares his thoughts on the recent rally in asset prices in his latest memo.

It is imperative that all Americans see recent events around racial inequality as a call for action and work to ensure equality for people of color. In his latest memo, Howard Marks shares his thoughts and pledges to heed this call.

True expertise is scarce and limited in scope. Howard Marks’s Uncertainty II — a postscript to his recent memo Uncertainty — explains why we should be careful about the “experts” we listen to and the weight we assign to their pronouncements.

In investing, uncertainty is a given – how we deal with it will be critical. Read Howard Marks’s latest memo, in which he discusses the value of understanding the limitations of our foresight and “investing scared.”

Read Howard Marks's latest memo, in which he discusses the notion of making informed guesses regarding the future and shares his questions about re-opening the U.S. economy and the latest Federal Reserve moves to help the economy combat the coronavirus.

The most important thing for an investor is to set the right balance between offense and defense. Today Howard Marks no longer feels defense should be favored. Find out why in his latest memo, Calibrating, in which he describes the importance of positioning portfolios in response to the environment.

How should investors think about the economy and asset values when faced with unprecedented uncertainty surrounding the effects of the coronavirus and a complete absence of guidance from analogies to the past? Read Howard Marks’s latest memo, in which he lays out the views of both the optimist and the worrier.

After giving our clients a few days to digest it, we’d like to share this memo from Thursday with all of our readers. We hope you’ll find it helpful.

Many questions – and few answers – surround the coronavirus epidemic and its implications for financial markets. Read Howard Marks’s latest memo, in which he shares his own questions, guesses, observations and inferences to help make sense of the potential impact of the virus on global economies and markets.

What really is a bet? How does one make decisions under uncertainty and with imperfect information? In his latest memo, Howard Marks weaves his own life story to discuss the process of thinking in bets, parses the world of gambling, and draws parallels between investing and games of chance.

Negative interest rates are nothing short of a mystery; they’re likely to throw off whatever we knew about the financial world and how things worked in the past. With more than $17 trillion of global debt trading at nominal yields below zero — and about double when considering inflation — this phenomenon has prompted differing perspectives about its purpose and consequences. Howard Marks offers his in this memo, in which he discusses why negative rates have become prevalent, what implications they might have, whether they will reach the U.S., and what investors can do as they navigate these uncharted waters.

Expectation that the Federal Reserve will cut interest rates has been a primary factor driving investor sentiment and actions in recent months. It should be noted, though, that the considerations and actions of the Fed are part of a complex ecosystem that has financial, political and behavioral components that come with considerable uncertainty.

In good times, we often see the notion "this time it's different" work its way into the marketplace as investors seek to rationalize higher asset prices and continued upward movement. Today this sentiment is expressed in contexts ranging from questioning the prospect of a recession altogether to supporting the high valuations of tech companies despite their current profitless state. In his latest memo, Howard Marks discusses the outlook for nine such theories. It would truly have to be different this time around for them to hold.

A few weeks ago, we were pleased to announce a partnership with Brookfield Asset Management that created an alternative investment manager with one of the broadest slates of strategies and greatest asset totals. And what question did I get? “Will there still be memos?” Well, here’s your answer.