Is it a bubble or isn’t it? That’s what everyone seems to be asking about the US stock market. I say it isn’t. A bubble to me is when price becomes disconnected from any rational, articulable value, the way people chased opaque schemes in the Roaring 1920s or the blind faith in new internet companies in the 1990s.

When investors feel like the stock market is toppy, as many do now, they often compare what they expect stocks and bonds to pay. The yield on stocks should offer a premium over bonds to compensate for higher risk, and it usually does.

It’s not often that investors encounter something truly new in markets. But they will soon when Space Exploration Technologies Corp., OpenAI and Anthropic PBC go public with trillion-dollar valuations, or close to it. No company listed in the US has ever come to market so extravagantly priced — by a long shot.

I’ve lost count of the praise heaped on US hedge funds for their “historic performance” in April on artificial intelligence-related bets and alleged foresight of a ceasefire in the Iran war.

Apollo Global Management Inc. announced last week that it will soon provide daily pricing for its private credit. It may not sound like a big move, but its decision to lift the veil on these assets could be the most impactful development in financial markets and investing in a long time.

Warren Buffett shared his usual wisdoms about patience, diligence, prudence and kindness in a CNBC interview the morning of Berkshire Hathaway Inc.’s annual meeting last Saturday, the first in many decades that the oracle did not lead. But the sign that hung above him spoke loudest.

Affordability is a major problem that is finally getting the attention it needs. As important is directing that attention at the root cause of America’s cost-of-living crisis: inadequate wages.

Many people seem surprised by the US stock market’s resilience during the Iran war. I’m not one of them, and I don’t see the war becoming a significant threat to the market, even if it drags on.

Those are a lot of disappointments in a relatively short time. That also left some investors wondering if Treasuries are still the bear-market hedge they are touted to be — which prompted me to ask if they ever were. After digging into the data, I discovered a surprising answer: no.

Most investors, from grandma to the mightiest sovereign wealth funds, own bonds to help steady their portfolio and provide a ready reserve for spending. So, it’s notable when prominent voices start questioning their safety.

There are calls in Europe to “sell America” and invest that money at home in response to political tensions over Greenland.

Every time there’s a raging bull market in stocks, as there is now, people start worrying about too much leverage in the market, and for good reason. When investors chase stocks with borrowed money, bad things can happen.

The article examines the high valuations of AI-focused tech giants like Alphabet and Nvidia, contrasting the risk of an "AI bubble" with their powerful profitability. While Berkshire Hathaway's new stake in Alphabet signals confidence, both companies require substantial future growth to justify their current multiples.

This lack of transparency around private assets has helped the industry grow and innovate; it has also created a rapidly expanding multi-trillion-dollar black box that could pose systemic risks.

Gold resembles stocks more than bonds in terms of risk, although stocks have been better performers. Since 1968, gold has been about 20% more volatile than the S&P 500 while trailing it by 2.3 percentage points a year.

A lot of people are watching this meteoric US stock market with amazement as it shakes off one worry after another – slowing labor market, sagging consumer sentiment, continuing trade uncertainty, geopolitical tensions and now a US government shutdown – on its way to new record highs.

Many people are puzzled about the disconnect between how well the US economy is doing and how badly Americans feel about it.

For as long as I can remember, institutional investors have been hailed the “smart money” and retail investors derided as rubes.

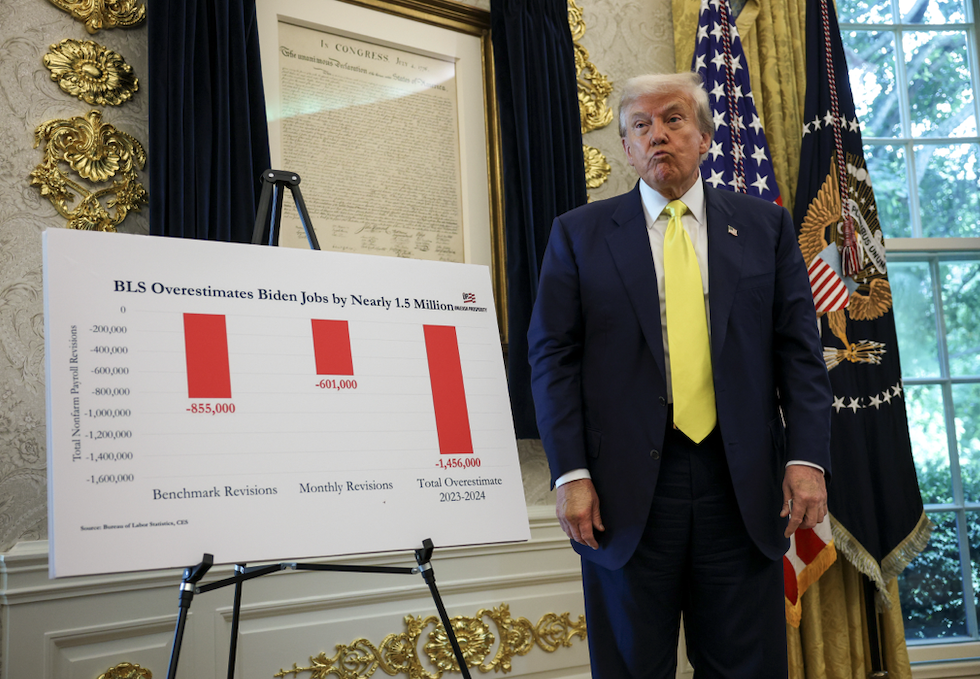

The Fed has long been criticized for reacting too slowly to economic developments, an inevitable consequence of relying on lagging government data. Now the Fed and BLS are likely to face even more pressure to catch up.

With all the uncertainty around big policy questions that directly affect companies, notably tariffs and immigration, forecasting has become thorny for Wall Street analysts.

Ordinary investors have won the battle of fees. The challenge will be holding on to that victory as Wall Street mounts a counteroffensive.

If the Trump administration’s tariff policies result in higher overall inflation, a scenario that will play out in the coming weeks, the question is who will pay for it.

It may seem as if Treasuries are the better bet these days with the US stock market back near record highs and government securities offering respectable yields again. But stocks are still likely to pay more.

If I told someone with even a little investing experience that I own an asset that pays like stocks but is stable like bonds, they would probably think I was a huckster or a fool. Yet many of the most sophisticated investors claim to own such a thing.

A lot of people are worried about the level of US interest rates. “I think we should be afraid of the bond market,” billionaire investor Ray Dalio said last week.

Imagine an institutional investor that allocates a big chunk of its portfolio to illiquid private assets but then needs to sell some of those investments to raise cash. Or a fund company that makes a fortune on actively managed mutual funds for decades, but its investors move their money to low-cost index trackers.

Warren Buffett, the greatest investor of all time, will step down as chief executive officer of Berkshire Hathaway Inc. at the end of the year. The six-decade track record he leaves behind is so astonishing that mere numbers on a page don’t do it justice.

I confess that when the VIX, the Cboe Volatility Index, spikes, I brace for stock market declines. Judging by investors’ anxious reaction to the VIX’s surge following President Donald Trump’s big tariff announcement last month, I’m far from alone.

Now that Warren Buffett, the philosopher king of modern investing, has announced that he will step down as Berkshire Hathaway Inc.’s chief executive officer at the end of the year, it’s a good time to marvel again at his career.

Now that the stock market has momentarily stabilized from the shock of President Donald Trump’s “Liberation Day” tariffs, investors have an opportunity to reflect on how their portfolio held up during the past two turbulent weeks.

President Donald Trump’s bombshell Liberation Day tariff announcement was greeted with one of the worst two-day US stock market routs on record. Whatever you think of Trump’s tariff policies, they are a huge gamble, and no one knows how things will play out.

The US stock market is on edge. The S&P 500’s recent 10% correction has investors worried, though a highly uncertain policy environment and an unusually top-heavy market obscure just what is spooking stocks.

President Donald Trump is attempting the most sweeping transformation of government and policy in decades. The White House is moving furiously to slash spending, expand tariffs, repeal regulations and rewrite tax rules.

President Donald Trump may have found a way to force the Federal Reserve to lower interest rates after all.

If I were to ask investors to name the best businesses in America, I suspect many would point to the Magnificent Seven, and understandably so.

If you’re looking to a popular stock market tracker like the S&P 500 Index to gauge the effect of President Donald Trump’s proposed tariffs, don’t. It’s likely to be insulated from much of the fallout and therefore fail to reflect the true impact on US businesses.

DeepSeek, a Chinese artificial intelligence startup, has developed a model that can apparently answer questions as well as any chatbot in the US. It might even help answer a long-running question on Wall Street without being asked.

There’s a lot of chatter on Wall Street about artificial intelligence replacing analysts — the folks at banks and brokerages who tell investors which stocks to buy, hold or sell. The bots should be able to make those recommendations just as well as humans.

Stock investors have been watching the runup in US Treasury yields with considerable alarm of late.

Maybe you have a pile of cash to invest, but you’re terrified of putting it into a US stock market near record highs.

Meet the new stock pickers. They will remind you of the old stock pickers.

December is a big month for stock buybacks, and by month’s end, companies are expected to spend more money repurchasing shares this year than ever before.

Berkshire Hathaway Inc. reported its stock holdings last week — a widely anticipated quarterly update of Warren Buffett’s latest trades. There were some notable ones, including the addition of Domino’s Pizza Inc. to Berkshire’s portfolio and more trimming of its stake in Apple Inc.

The Federal Reserve is widely expected to lower its benchmark federal funds rate by a quarter of a percentage point on Thursday to a range of 4.5% to 4.75%. The big question is how much lower the Fed might go from there during this rate-cutting cycle. The bond market suggests it won’t be as low as some expect or as low as policymakers signaled less than two months back.

When Covid-19 brought the US economy to a standstill in the spring of 2020, America’s top executives called for a “national conversation” about the need for workers to return to work, warning of an “economic catastrophe” if they didn’t.

In China’s resurgent stock market, there’s a lesson for investors about the perils of market timing.

China’s recent stimulus announcements sparked a massive rally in its stocks, and a growing chorus of analysts see more gains ahead. Is this a reawakening of the country’s long slumbering stock market or just another false start? Bloomberg Opinion’s Nir Kaissar and Shuli Ren, based in the US and Hong Kong respectively, met online to discuss the risks and opportunities.

A lot of people are worried about the shrinking number of public companies in the US, but quality is an even bigger problem than quantity.

Financial services, like many institutions, are losing Americans’ trust. That’s a problem. Economies depend on a healthy financial system, as became painfully evident during the 2008 financial crisis, and that system operates largely on trust — confidence that people can access the money in their bank accounts, that their investment accounts are secure, and that their trades will be filled at quoted market prices, to name just a few everyday financial interactions.

Retail investors have won the battle of fees. Brokerage accounts are free. Trading commissions are history. Anyone can own the entire stock market through a single exchange-traded fund for basically nothing. It’s a huge win for investors and terrible for the investment industry.