When you measure home affordability today against the metric that actually governs the check you write each month, the picture flips. By that measure, buying a home may be easier now than it was for the Boomers and Gen Xers who get blamed for everything.

Decades of data across global markets reach the same verdict: the more frequently retail traders trade, the worse they perform. The infrastructure has never been more inviting. The losses have never been more documented. Here are some key statistics we will dive into further.

If you knew you were standing inside a stock market bubble, you wouldn’t be standing in it for long. You’d sell. So would I, and so would everyone reading this. And if spotting market bubbles was something everyone could do in real time, the bubble couldn’t form in the first place.

The AI capex risk profile has gotten sharper since then, and the argument needs tightening in a few places. The bull case and the tail risk are now the same buildout, but they are running in different directions.

Rising prices increase the value of collateral in every margin account, which automatically increases how much each investor can borrow under Reg T. Debt rises BECAUSE the market rose, not the reverse. That single fact is what breaks the ratios we’re about to examine, and it lies at the core of why margin debt risk is so often misjudged.

Wage growth peaked four years ago. Since 1985, it has led CPI by three to seventeen months in every single cycle. The May 4.2% inflation print is the noise. Watch the wages.

The money is REAL. The question was never whether it exists. It’s who’s spending it, and what they borrowed to do it. When the wall of cash and the bottom half finally commit to risk at the same moment the Fed turns hawkish, that’s not the start of something. That’s the part of the cycle where the careful investor gets paid to be careful.

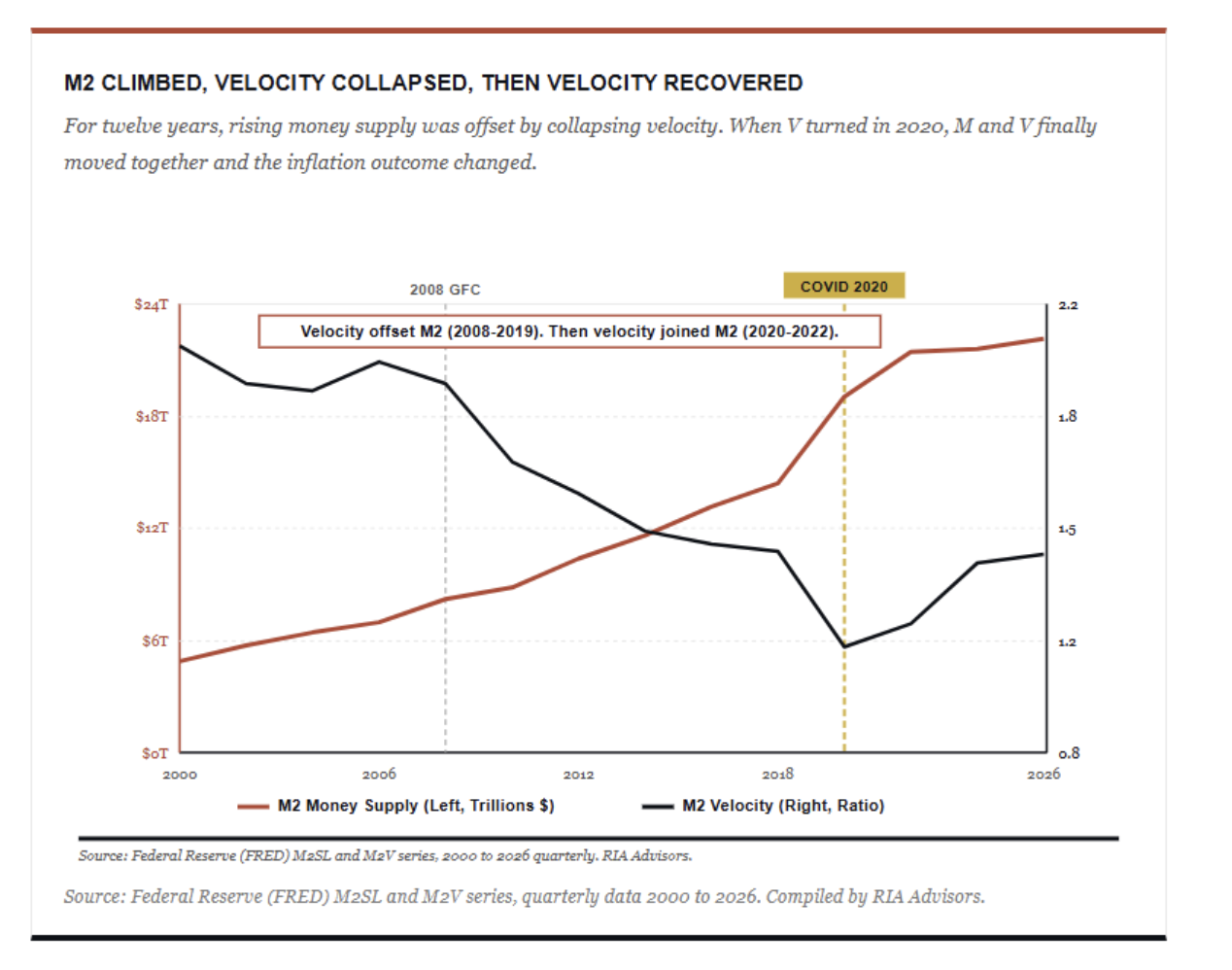

Friedman was reasoning from the equation of exchange, MV = PQ. Money times velocity equals prices times real output. It’s an identity, not a theory. Where it gets interesting is when you ask which variable does the work.

Here’s the setup most investors are underrating right now. Over the next two weeks, the tape will trade on plumbing rather than fundamentals. We just cleared the largest options expiration in history. Quarter-end pension selling comes next, and then July 1 reopens the passive-money firehose into a market that already routes forty cents of every S&P 500 dollar into ten stocks.

Start with the disconnect itself. If you only looked at the Michigan headline, you’d assume the country was in a depression. However, when you look at what people are actually doing, the picture changes completely.

The catalyst that turns a healthy pullback into something deeper won’t be a single oil-soaked CPI print. It’ll be the moment forward earnings expectations start to roll over while valuations sit at the high end of history. We aren’t there yet.

The K-shaped economy has become shorthand for a tidy story. The rich pull away while everyone else falls behind. It fits the mood, and it makes for a sharp headline. The problem is that it’s mostly wrong.

This past week, the market hit an all-time high. At the same time, Alphabet (GOOG) told investors it would raise $80 billion by selling stock to fund its AI buildout, and the shares fell about 4% on the news.

In Part 1, we explored why Dollar Dominance Remains Alive and Well. Today, we will explore the stronger-dollar trade, the one macro trade that nobody is sized for.

Reducing equity exposure during periods of elevated risk is not the same as market timing. The financial industry has spend decades blurring that distinction.

The dollar is supposed to be dying. We’ve heard that argument for the better part of a decade, and it’s getting louder, not quieter. Dollar dominance isn’t fading. In fact, the events of late April 2026 just delivered the loudest counter-signal in years.

After three decades of watching market cycles play out from both sides of the trade, I’ve come to a simple conclusion: Wall Street’s love of simple rules is one of the most dangerous aspects of investing.

Last Friday closed with the 10-year Treasury yield at 4.60%, a one-year high, and the doom commentary about rising interest rates was waiting before the bell even rang. Hyperinflation. Bond market breakdown. Paradigm shift. A 1981 fair-value retest.

That Buffett cash hoard has also created a lot of speculation, innuendo, and assumptions, which is what I want to walk through in today’s discussion. Primarily, what that cash hoard actually represents, the popular theories explaining it, and what it really costs shareholders to hold.

The stagflation narrative dominating financial social media isn’t completely wrong. That’s what makes it so dangerous. After more than 30 years of managing client portfolios through actual inflationary cycles, not watching them on YouTube, I’ve learned that the most damaging investment advice isn’t built on outright lies.

A real fundamental story doesn’t require a parabolic chart to validate it. In fact, fundamentals tend to drag prices up the trend line, not push them through the ceiling. When a “shortage” narrative arrives at the same moment that the worst-quality names in the sector are leading the index higher, that’s not fundamentals at work.

That skepticism isn’t contrarianism for its own sake, but rather the recognition that when a thesis achieves consensus, the crowd has usually already priced the easy part of the move, and the hard part is what comes next.

The S&P 500 hit a fresh record high last week. The median stock in the index is sitting 13% below its 52-week peak. That divergence is not a footnote or a curiosity.

Robots are coming to the economy. It is inevitable, really, and there is nothing that will stop it. At some point in the not-so-distant future, robots will infiltrate every aspect of our lives, from office work and manufacturing to service work and trade skills, and even your home. Here are some numbers for you.

Here’s where I want to start, because this is the point that almost every government debt analysis, including the article we’re responding to, completely ignores. Government debt doesn’t disappear into a void. By definition, if the Government borrows capital from someone, that capital must flow somewhere.

As of this writing, the Strait of Hormuz remains effectively closed since February 28. Roughly 20% of the world’s seaborne oil stopped moving through the chokepoint. T

The stock market selloff between February 28 and April 14 produced one of the more instructive market lessons in recent memory. It isn’t because of what the market did, but because of what investors did in response.

The BLS jobs report has become so distorted that it often tells us almost nothing reliable about the actual state of employment. I realize that is a serious claim, but let me back it up with the data. I want to show you what I believe is a simpler, more honest alternative.

Over the last few weeks, we have published real-time market commentary as the correction proceeded. The goal was to help investors navigate the more dire outcomes promoted on social media. A largely unexpected outcome was that the S&P 500 outlook changed dramatically in a matter of days.

That article digs into the plumbing behind oil shocks and recession, and exposes why, over the years, I’ve learned to distrust the loudest voices in the room.

Last week, the stock market rally was one of the best performances in nearly a year. The S&P 500 surged 3.4%, the Nasdaq climbed 4.4%, and the bulls declared the correction over. As I have stated before, having watched markets for more than 35 years, I have come to recognize the difference between a relief rally and the end of a corrective cycle.

After more than three decades of watching oil markets upend economies, one pattern keeps repeating: investors learn the wrong lessons from the last shock. The 1973 OPEC embargo taught us that geopolitical disruptions are temporary.

The fiat currency collapse narrative is one of the most emotionally satisfying arguments in all of financial punditry. It feels intellectually rigorous, draws on genuine history, and speaks to deep and legitimate anxieties about government overreach, monetary recklessness, and the long-term consequences of unlimited debt creation.

What’s unusual today is the degree of divergence between individual stocks and the cap-weighted index. When a handful of stocks carry enough weight to paper over widespread internal damage, investors holding diversified portfolios feel the pain long before the headlines acknowledge it.

Every few months, a headline appears declaring that the U.S. dollar’s reign as the world’s reserve currency is over. China is dumping Treasuries. Central banks are hoarding gold.

Last week, on March 19th, the S&P 500 closed below its 200-DMA for the first time since May 2025. The first instinct is to panic as media headlines talk about bear markets and financial crisis events. However, as we will explore today, the data says it depends entirely on the type of break: sustained or brief.

This past weekend, Adam Taggart and I discussed what happens to Treasury bond yields when the United States enters a military conflict. The conventional wisdom is reflexive and tidy.

The private equity (PE) business is huge. When I say huge, I mean $4.4 trillion huge. However, as we warned then, the risks have come home to roost. The private equity and private credit industry is heading into a gut-wrenching period of consolidation.

The “fiat is dying” argument has become a catchphrase narrative among digital asset bulls, gold bugs, and cryptocurrency advocates. That narrative’s core is that central banks have printed vast amounts of money.

The S&P 500 closed at 6,740 on Friday, its lowest level since mid-December, as technical deterioration, collapsing payrolls, and $100 oil converged on the charts. Every major moving average has broken. Here’s what comes next.

If the SaaSpocalypse narrative proves to be more panic than prophecy, the critical task becomes identifying which companies will emerge stronger.

Economic growth metrics for the United States have recently shown surprising resilience; however, consumers’ economic sentiment has not. According to the Bureau of Economic Analysis’s advance estimate, real Gross Domestic Product expanded at an annualized rate of just 1.4%.

Money – everybody wants it, but few actually have it. As shown in recent financial statistics, the “wealth gap” in America continues to grow between the “haves” and the “have-nots.”

“China is dumping US Treasuries to get out of the dollar.” This claim has been circulating the mainstream feeds lately, with the narrative that the “end of the dollar is near,” or “the US will lose its funding base,” and “bond yields will surge.” But are those claims valid? Such is what we will explore in more detail.

The article from the Wall Street Journal titled “Why My Generation Is Turning to Financial Nihilism” by Kyla Scanlon argues that Gen Z is embracing high-risk financial behavior out of despair and detachment, but the data shows something very different.

Since the beginning of the year, we have discussed the “reflation trade” and its impact on specific market sectors. This past weekend’s newsletter also showed some of these more extreme returns in various market sectors since the beginning of the yea

The market got off to a strong start in 2026, with investors chasing industrials, materials, and commodity-related stocks as the reflation narrative gained traction. The “reflation narrative” is the belief that a range of policies will boost the rate of economic growth in the U.S. without triggering inflation.

For nearly two years, markets were driven by the same speculative narrative that “this time is different.” Speculative narratives are not only seductive but also contribute to investment behaviors that obscure reality. Speculation disguised as investing is a losing proposition.

Market cycles are once again at the center of the investment narrative as we head into 2026. The optimism is familiar as earnings held up in 2025, the economy avoided recession, and big tech lifted the indexes. However, those victories are already reflected in the price.

Mainstream expectations, those from Wall Street, economists, and corporate strategists, have congealed around a bullish economic outlook for 2026. Most forecasts project stronger economic growth, with contained inflation, and continued investment in technology and capital expenditure.