Whenever faced with tradeoffs between risk and return, we recommend turning to expected utility. The method of maximizing expected utility is the most sensible technique for making these tradeoffs, taking into account both your personal preferences and the specifics of the situation.

Probably the most popular insight to make its way from finance theory into everyday usage is that "diversification is the only free lunch" in investing. The idea dates back to Harry Markowitz in 1952. He, and those building on his work, demonstrated that in an efficient market, investors shouldn't earn extra return for bearing company-specific risks that can be diversified away.

Vanguard’s Total World Stock ETF (ticker VT) is an elegant product: a single fund that gives you cap-weighted exposure to the entire global equity market. For investors who want simplicity, it’s hard to beat. But is simplicity costing you money?

Rather than worrying about the narrow impact of faster IPO inclusion on index fund performance, we think investors would be better served by focusing on the long-term expected returns offered by the markets in which they’re investing – in particular the U.S. and non-U.S. equity markets.

It’s tax season, and we’ve been reading a lot about taxes — and strategies for mitigating them. In this note, we’ll take a close look at one such strategy, known as leveraged long/short direct index tax-loss harvesting (LSDI), and explain how investors being pitched the strategy can assess whether it’s right for them.

Thanks to Section 351 of the US tax code, investors can contribute their appreciated assets directly into an ETF structure without realizing gains at the time of transfer. Here, we briefly explain the mechanics, limitations, and potential benefits and risks of a 351 exchange to seed a new ETF with appreciated assets.

While we don’t find much reason to underweight our allocation to U.S. stocks based on the current high degree of concentration, we do believe that the valuation of the overall U.S. stock market today is consistent with low expected returns relative to safer fixed income investments.

The concepts underlying our suggestions are straightforward, grounded in basic portfolio theory, and eminently practical. Most importantly, they align the committee’s focus with the endowment’s true objective: maximizing the sustainable resources available to beneficiaries over the long run.

Buybacks raise important questions. Foremost amongst them are whether, and how much, buybacks push up stock prices, and whether they create other distortions relevant to investors and public finances. This article explores these questions by drawing on economic theory and broadly held views of real-world investor behavior.

We steer our financial course through life, choosing how much to spend and how to invest what’s left, periodically updating our choices as circumstances evolve. This is the essence of financial planning: specifying in advance a desired spending and investment policy conditional on relevant aspects of our life, varying investment opportunities, and our preferences for the benefits derived from our wealth.

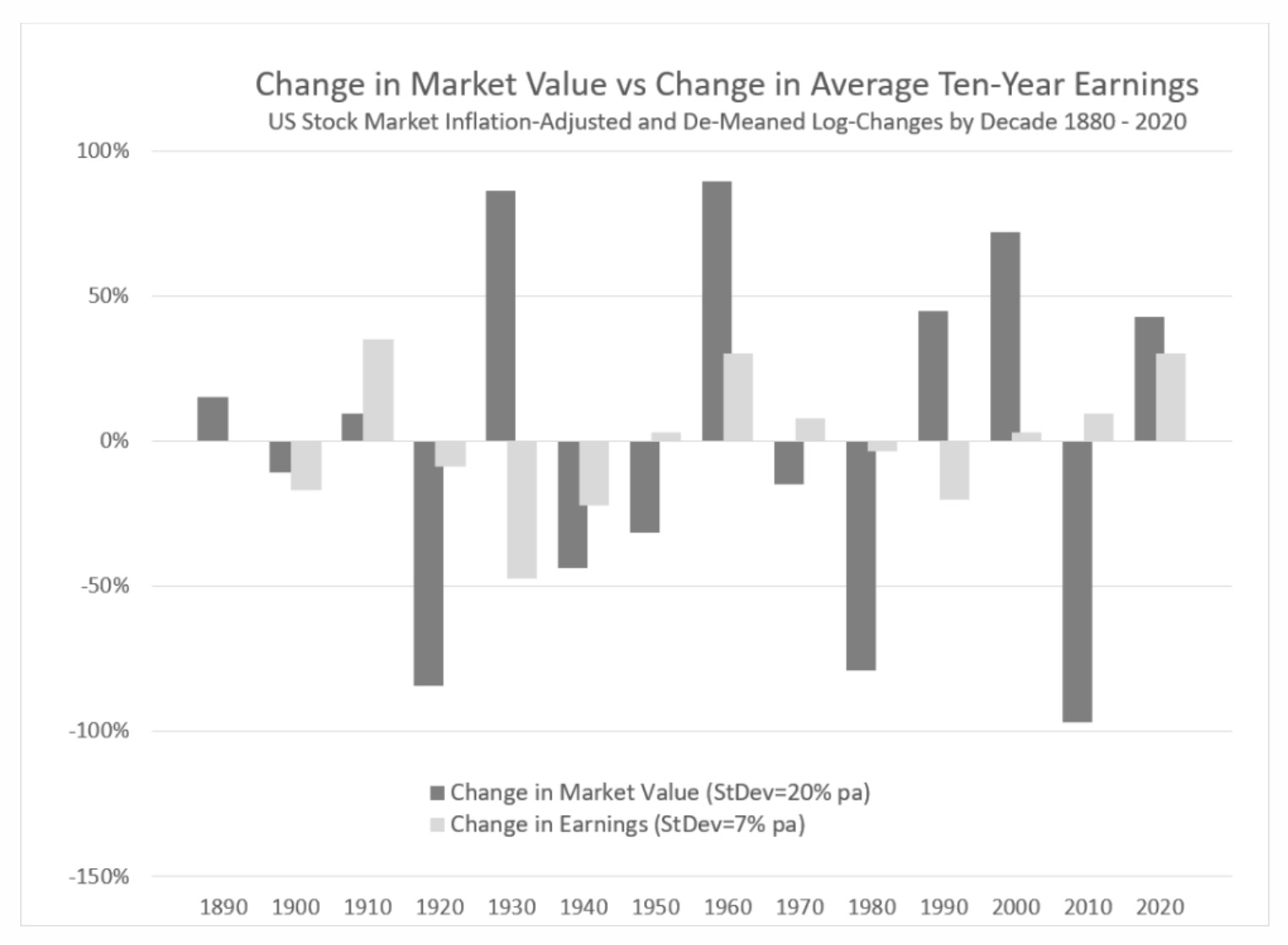

While the US has indeed enjoyed a tremendously exceptional economic environment over the past 125 years, this has not translated into earnings growth that US companies could freely tap into.

We hope you find this alternative perspective based on forward-looking excess expected return helpful (and stress reducing) as you consider putting money to work in stock markets today and in the future.

We suspect that for many of our clients, converting to a Roth will make sense, either today or in the near future. We hope this note and our calculator will encourage many of you to give the conversion decision another look.

While the bond market is in general pretty efficient in its pricing, there may be times when it can be significantly out of line with investor expectations. At such moments, investors should be well-rewarded for making the effort to decode what the bond market is saying.

Over the past ten years, we’ve discussed this question with about 50 of our friends and clients, resulting in many animated and productive conversations.

As with all decisions involving uncertainty, we want to find the answer which maximizes your expected risk-adjusted return, not your base-case or expected return. This means that we have to go beyond the industry standard and explicitly account for risk in our analysis.

As market prices change over time, so will the fraction of your portfolio which is in stocks or bonds. How often should you rebalance your portfolio back to your desired asset allocation? And how much is that rebalancing worth?

Modern direct indexing tools, using sophisticated technology, can identify tax loss opportunities on a daily or even minute-by-minute basis. As time progresses, I believe more advisors will see the potential of direct indexing.

The central question we want to address in this note is how to quantify how “price sensitive” insurance buyers should be, and in the context of insurance, what is the “price” they should be sensitive to?

In this note, we'd like to share our analysis of one potential solution we've been hearing about a lot lately. It involves leveraged direct index tax-loss harvesting.

Investors can now choose from about $100 billion in ETFs that provide leveraged long or short exposure to a broad range of popular stock indexes and individual companies.

A visit to the annual Bogleheads conference got Elm Wealth's Victor Haghani thinking about static vs. dynamic asset allocation.

In the 1989 blockbuster Back to the Future II, time travel enables Michael J. Fox’s nemesis, Biff, to become a gazillionaire by bringing an almanac with sports match outcomes back from the future. We thought it might be instructive, and certainly entertaining, to make a less fanciful version of this dream a reality – for a few lucky people.

In this article, we’re going to throw some cold water on the DI love-fest by explaining why most tax-sensitive investors would be better off with a simpler approach to tax loss harvesting.

There’s been a lot of excitement and reporting about a new ETF: the Alpha Architect 1-3 Month Box ETF (ticker BOXX), designed to give investors the return of short-term US Treasury Bills with the tax character of long-term capital gains.

The average risk-adjusted excess return across all active portfolios will be less than the risk-adjusted excess return of the market portfolio, before taking account of fees and trading costs.

We've all heard the mantra "Cut your losses early; let your profits run." Does it make sense? We take a deeper dive in this short research note.

Today, not one Vanderbilt descendant can trace his or her wealth to the vast fortune Cornelius bequeathed.

The ongoing public drama surrounding Sam Bankman-Fried (SBF) and FTX is still unfolding, and there's been excellent coverage of many aspects of the story. Here's a short note on one piece of the puzzle we think is quite important, but so far has remained somewhat under the radar.

The S&P 500 is down 15% over the past year, so you’d think this would have been a great time to own some protection on your portfolio. Unfortunately, that’s not how things have turned out.

How risky is the stock market for investors who are focused on the long-term real spending their wealth can support, rather than the present value of their wealth?

It’s easy to overlook the fact that, in thinking about investment risk, we are implicitly making a choice about the benchmark against which risk is measured.

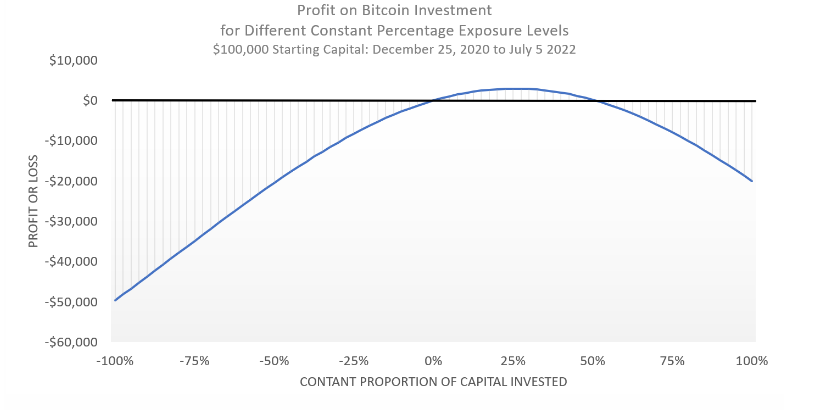

If you put $100,000 of your savings into Bitcoin at the end of 2020 and are still holding those coins today, you’d be down 20% on your investment. But, if you'd used that $100,000 to short Bitcoin, you’d have suffered a loss too. How is this possible?

If finance could be distilled into one idea, it likely would be that there should be a tradeoff between risk and reward: an investment with low risk should have a low expected return, while one that could make you rich should also be one that could lose you a lot of money. The Overnight Effect flies in the face of this core tenet.

The year 2022 sure has felt like a pretty bad one so far: interest rates and consumer prices have spiked up, and stock prices are sharply down. But, in terms of what really matters, many investors are better off than they were at the end of 2021–almost 5% better off for an investor in a diversified balanced portfolio.

What are we to make of the near-total wipeout of the stablecoin Terra and its companion coin Luna, in which around $50B in value vaporized in less than a week?

Yale Professor Robert Shiller’s Cyclically Adjusted Price-to-Earnings ratio (CAPE) is a respectable predictor of the future real return of the stock market, but it underwhelms when used on its own to set stock exposure. We examine a better way of using CAPE, with much better results.

In general, the more optimistic we are on the prospects of an investment, the more of it we’ll want to own. However, at extreme levels of bullishness, the normal relationship can be turned on its head and it can make sense to own less of an asset the more we like it.

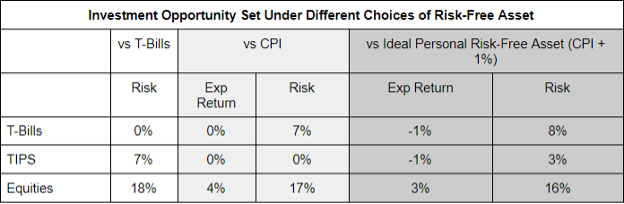

We provide a practical definition of the ideal personalized risk-free asset, and then we’ll discuss how to construct an efficient portfolio when that ideal asset doesn’t exist in investable form.

The top ten stocks in the S&P500 add up to 27% of the index. Is that a problem?

Is it better to jump in all at once, to average-in over time or to wait for a market correction?