Financial markets have been relatively unaffected by the costly and senseless war the US and Israel are waging against Iran. But what’s really surprising is the ongoing boom in investment banking.

Private credit managers are feeling sheepish. Some of their investors can’t get their money out as quickly as they’d like — and some may be quite angry about that.

Banks making loans to specialist fund managers instead of directly to companies is meant to act like a firebreak protecting traditional lenders against the risks of businesses going bust. But losses from financing private credit firms and other nonbank lenders are coming back to bite them — and it’s making their investors antsy.

The Federal Reserve is about to give America’s biggest lenders an extra $200 billion of capital to play with. Later this week, US regulators will launch fresh proposals to update and, in some ways, loosen US capital rules that will fuel stock buybacks, lending and trading.

Back in 2008, executives at Goldman Sachs Group Inc. were zealots for valuing their assets at exactly the prices where they could be sold. Critics said this fervor for fair value inflamed the financial crisis, while supporters argued it helped investors and lenders at least know where they stood.

Private credit firms are facing a major test, with mom-and-pop investors pulling their cash in fear of corporate defaults spiking and artificial intelligence destroying many of the software businesses that these funds have lent to.

Artificial intelligence fears have ripped through stock and bond markets, but investors in loans and private credit are still playing catch-up.

Artificial intelligence doesn’t only threaten to put herds of software businesses out to pasture. Anthropic PBC’s schooling of its Claude models in financial modelling has also sent a cold shiver down the spines of bankers and analysts.

Warren Buffett has a great line on how hard it is to pick winners when major industrial change is afoot. “What you really should have done in 1905 or so, when you saw what was going to happen with the auto, is you should have gone short horses,” the Oracle of Omaha once said.

Big banks’ share traders are raking it in right now. Sure, stock market indexes have been flying high, but it’s been far from certain in recent years that traditional Wall Street firms would reap the benefits with electronic market makers storming the zone.

While outright defaults in the private credit sector remain low, analysts are increasingly concerned about the deteriorating outlook for repayment problems. When factoring in "selective defaults"—like borrowers adding interest to the loan (PIK loans) or extending maturities—the true default rate climbs to a significantly higher 4.6%.

Despite these successes, many finance executives struggle to quantify the actual return on AI, as the required spending on development, data clean-up, and rigorous testing is immense and mostly paid upfront.

The rebirth of private equity dealmaking has been supposedly just around the corner for well over a year. But even as investment bankers cheer a rush of mergers & acquisitions and the reopening of the market for initial public offerings, many financial sponsors are still struggling to catch the same wave.

Jane Fraser’s elevation to chair as well as chief executive officer of Citigroup Inc. is a reward for progress and a bulwark against potential pretenders to her throne. Her restructuring of the lumbering and longtime dysfunctional beast that is the US’s third-largest bank by assets is taking time and is far from done.

Bank of America Corp. and Morgan Stanley exposed a stock market puzzle on Wednesday. Both reported record third-quarter earnings following roaring results from rivals the day before.

All’s fair in love and politics — and international bank capital rules. US financial watchdogs are making mischief with European standards that give lenders relief by treating the euro zone as a single domestic market.

JPMorgan Chase & Co.’s $20 billion debt commitment for the record-breaking buyout of Electronic Arts Inc. is classic leveraged financing, which might seem surprising in a world overrun with private credit.

Buy-now-pay-later firm Klarna Group Plc is among a string of companies bringing US public stock offerings in what looks like an extremely busy September for investment bankers.

Credit cards versus stablecoins is one of the less-discussed competitive battles ahead, but it’s one where traditional finance faces the most coherent threat.

“The size, scale and scope of JPMorgan Chase also offer huge advantages,” Jamie Dimon wrote in a letter to shareholders — his first as chief executive officer at the end of 2005.

Goldman reported record equity trading revenue in second-quarter earnings on Wednesday and trounced its peers with a rebound in investment banking revenue that was fueled by a 70% jump in deal-making fees versus the same period last year.

Chief executive officers in the US and beyond are becoming accustomed to the policy swings of President Donald Trump and are deciding they can pursue growth ambitions regardless.

Global central bankers have ducked a chance to push for tight borrowing constraints on the biggest hedge funds, whose importance to core government bond and other financial markets has grown enormously in the past decade.

The Federal Reserve is aiming to lessen the costly fluctuations in bank capital demands created by its annual stress tests. But big lenders are pushing for more relief while the central bank is politically weakened and some board members seem keen to please the White House.

Investment banks and private equity firms are fighting over the kids again.

Banks are contemplating a role for themselves in stablecoins if pending US legislation helps take cryptocurrencies and their gateway products mainstream.

When it’s finally completed seven years from now, Citadel LLC’s New York tower will be the second tallest building in the city, after the World Trade Center. It will also loom over the headquarters of JPMorgan Chase & Co. just a few hundred yards south along Park Avenue.

Electronic market makers like Citadel Securities LLC and Jane Street Group have been gobbling up market share from investment bank rivals, but to really get ahead they’ll need a helping hand. They might be about to get it from a surprising source: Some of those same banks.

Banks’ businesses don’t change radically year to year so nor should their capital requirements.

Banks needed the right version of Donald Trump to justify their high-flying stock prices. They got the wrong one. The US president’s chaotic and aggressive performance during his first few weeks in the White House has shocked companies, put investment plans and deals on hold and threatens to drag the economy into recession.

US investment banks have little room for error in their upcoming full-year results.

To understand the wave of bank partnerships with private-credit fund managers during the past year or so, think back to the boom in mortgage lending through securitization in the early 2000s. The same forces are at work: a huge demand for finance, limited and costly bank capital and investment bankers’ ingenuity and desire to generate business.

JPMorgan Chase & Co.’s net interest income was the hot topic of its third-quarter results, much to the irritation of Chief Executive Officer Jamie Dimon, who grew impatient with quibbling over details of the bank’s outlook on its earnings call on Friday.

Britain’s stock-investing culture has been withering for years, with the only real growth coming from consultants, policymakers and commentators generating ideas on how to revive it. So why is Robinhood Markets Inc. so keen to expand in the UK? The draw may be more the country’s enthusiasm for online betting than allocating savings to equities.

It might not be time to really get nervous about US money markets, but it’s definitely time to pay more attention. Signs of strain emerged as September turned into October this week — it wasn’t completely wild, but the tensions were the worst since early 2020.

Gary Gensler, chief US securities regulator, enlisted Scarlett Johansson and Joaquin Phoenix’s movie “Her” last week to help explain his worries about the risks of artificial intelligence in finance. Money managers and banks are rushing to adopt a handful of generative AI tools and the failure of one of them could cause mayhem, just like the AI companion played by Johansson left Phoenix’s character and many others heartbroken.

Banks and shadow banks are meant to exist in separate worlds, but the financial links between them are increasingly seen as a source of potential instability. That’s a problem for banks because the business of forging those ties has lately been among the hottest activities on Wall Street.

Jane Street Group LLC and Citadel Securities are on a tear. First-half revenue at the two predominantly electronic market makers grew about 80% compared with the first six months of 2023, according to Bloomberg News. That’s enough to make traditional Wall Street executives green with envy — but these upstarts aren’t going to completely devour the old guards’ lunch.

Call me Ishmael. The biggest question about an investment banking client like Elon Musk is whether he turns out to be a Moby Dick.

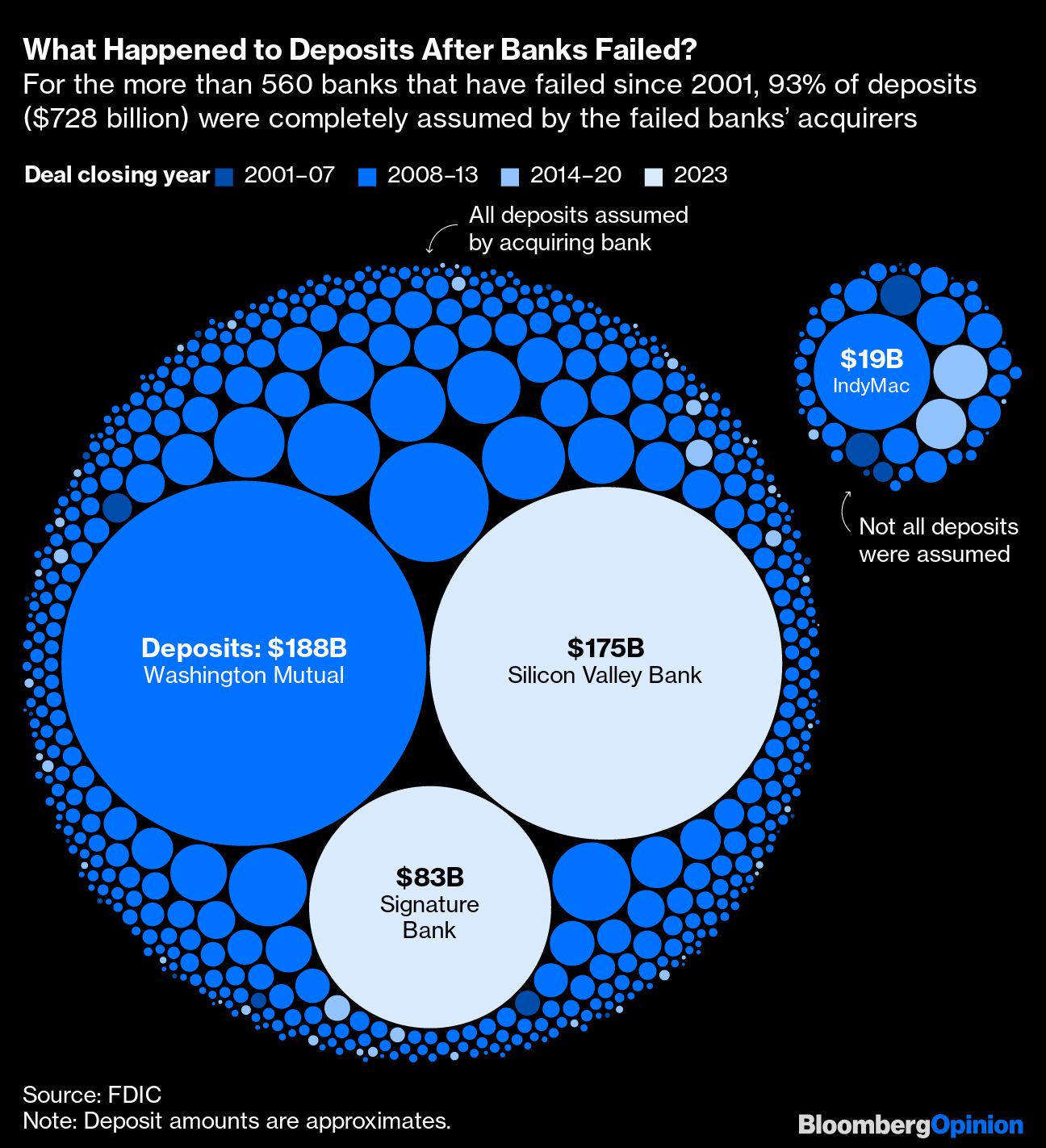

Since Silicon Valley Bank became the second-biggest failure in US history a year ago, other lenders have been trying to take its place in banking the fast-moving, entrepreneurial world of startups and tech companies.

When the Federal Reserve flooded the economy with cash during the Covid-19 pandemic it exacerbated a problem for America’s largest banks: What to do with all the extra deposits.

Big banks are scrambling to work out what to do with generative artificial intelligence: how to use it to make some of their people smarter or free up others to do only higher-value tasks, and how to ingest and process data more rapidly, speed up decision making and cut costs. Every bank fears their competitors getting good at AI before they do.

Two knockout stock-market debuts by tech companies last week will boost confidence among others waiting for their chance to go public – and lift the hopes of investors in venture capital funds who’ve endured meager returns in the past couple of years.

The failures of Silicon Valley Bank, Credit Suisse Group AG and others have gotten financial authorities thinking again about bank runs and liquidity regulations — and whether some rules ought to be tweaked to make the system safer.

Silicon Valley Bank suffered probably the quickest bank run in history and the fastest bailout of depositors, too. The lender to the venture capital industry had operated under lighter rules and fewer restrictions than larger banks after a successful lobbying effort back in 2018.

Stubborn inflation means more interest-rate increases are coming from the Federal Reserve and that sounds like great news for banks.

The health of borrowers is the key concern for all of finance in the coming year.

The $24 trillion US Treasury market has gotten too big for even the “Masters of the Universe.” As the Federal Reserve reverses its bond purchase program and more government securities flood back into the hands of dealers, banks, investors and traders, the chances of extreme, unhealthy volatility are rising.

If everyone feels so miserable, why do they seem to be out having a good time?

Everyone is stressing about consumer debt. Investors have been dropping the shares of big banks, credit-card specialists and younger fintechs because of fears about the pain that rising living costs and interest rates will inflict on borrowers.